Company Overview: Empired Limited is an information technology (IT) services provider. The Company is engaged in design, development and integration of business knowledge, information technology and creativity. The Company operates through two segments: Australia and New Zealand. The Company's business solutions include Cloud Services, Identity and Access Management, Systems Integration, Data Insights and Business Intelligence, Internet of Things, Spatial Services, Mobile Solutions, Digital and Experience Design, Enterprise Content Management (ECM), Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Digital and Experience Design, Infrastructure Transformation Services, Managed Infrastructure Services, Project Management Office (PMO) and Unified Communications. The Company operates in various industries, including retail and manufacturing, public sector, financial services and insurance, health, mining, oil and gas, utilities, transport and education.

.png)

EPD Details

Empired Ltd (ASX: EPD), an IT services provider specialising in consulting, applications and infrastructure services with a focus on providing business solutions, has a good reliance on its multi-year managed services contracts and higher margin project services for revenue generation. Empired’s exposure to a range of sectors adds diversity and minimizes sector driven risk to some extent.

Positive bottom line:Empired delivered a top line growth of 5% year on year (yoy) to $167 million for FY17. The key highlight of the group’s result entailed a turnaround of the profit after tax which reached $3.2 million during the year against the loss after tax of $1.7 million in prior corresponding period. The EBITDA surged 106% yoy to $15.4 million during the year. EPD’s Australian segment rose 3% yoy to $104 million during the year while the segment’s EBITDA reached $10.6 million. The New Zealand segment revenue enhanced 4% to $65 million while EBITDA reached 4.7 million. The New Zealand segment performance was weak due to adverse trading conditions on US based contracts hurting revenue and EBITDA by about $1 million. The group’s major growth markets, New South Wales and Auckland showed an outstanding performance in terms of sales, which rose by 32% and 67%, respectively. On the other hand, Empired faced contraction in hardware sales and the overall performance of US operations was subdued. But the hardware sales contributed only a small portion to profit and the group expects better results from the region in 2018.

.png)

FY17 Top Line Performance (Source: Company reports)

Controlled debt:As of June 2017, the group’s operating cash flow dropped to $9.8 million against $13.3 million in the prior corresponding period. This is because the earlier year had a cash lease incentive of $3.8 million and excluding this, the operating cash flow rose 4% on a year on year basis. The group also controlled their net debt to $13.8 million as compared to $25.6 million in the prior corresponding period while gearing fell to 16% from 33%. This better performance has been on the back of the equity raising of $15.1 million (net of costs) when 36.4 million shares were issued at 44 cents per share.

Growing managed services business:The group made huge investments in intellectual property in managed services, mobile and cloud applications. The Cohesion platform in New Zealand enhanced to over 7,000 contracted users as compared to 4,500 across the year. EPD is also launching Cohesion into Australia, and the expected ‘go-live’ date is said to be in the second half of 2018. Cohesion 365 is a cloud-based enterprise content management (ECM) service for Australian and New Zealand (ANZ) businesses and government agencies. This is built on the Microsoft-based enterprise document and records management service and was initially created by Intergen, for New Zealand government clients. Cohesion 365 has been a proven service in government agencies like the Ministry for Primary Industries (MPI) in New Zealand, with whom the group signed a six-year Cohesion government contract for NZD$12 million in 2015. The group is in early stage adoption of another Empired software tool which offers a low cost, rapidly deployable collaboration portal. From expansion standpoint, EPD has set up a delivery center in Bengaluru, India for the managed services business. Further, investment in a collaboration portal called SNAP and a mobile field services solution is also showing early stage commercial success. With these solutions shifting to production, the group forecasts a falling capital investment profile related with solution development combined with growing recurring revenue.

.png)

Business solutions (Source: Company reports)

Huge market opportunity: The SMAC trends (S standing for Social technology services and their rising adoption in enterprise; M standing for Mobile applications and rising usability via high speed mobile communications and low cost; A standing for Analytics driven by data explosion from firms and the advent of the Internet of Things (IOT); and C standing for rising rapid transition to the Cloud) are shifting the business landscape. The group has identified these trends at an early stage and invested accordingly in developing the capabilities to leverage the major structural shifts in SMAC market. Further, the mergers and acquisitions in the Australian sector by international strategic buyers drove the opportunity as several of the key competitors got acquired, and Management now believes that they are well positioned to capture the market share in circa more than $30 billion market. EPD is thus said to benefit from its services that are aligned with high growth segments of the market including Managed Services, Cloud, Mobility, Data & Analytics.

.png)

Strong recurring revenues (Source: Company reports)

Outlook:The group has built a strong recurring revenue stream wherein 66% of the FY17 revenue was derived from multi-year contracts. The group built long-term clients wherein 80% of revenue has been derived from 20% of clients as of FY17. EPD’s FY18 workbook is strong and can drive the top line growth going forward. Moreover, EPD continues to focus on delivering services that generate recurring style revenue. On the other side, the ongoing shift in technology is leading to a rapid consolidation of the group’s target sector in the local market, disrupting the competitive environment but opening several new opportunities. The group expects to see the benefits of the investments across a broad range of areas. Empired has also built a presence in diverse sectors instead of depending on a single major sector. The group derived 24% of revenue from the Government sector in FY17 while 21% was derived from the Energy and Natural resources sector. Finance and Insurance, Manufacturing & Transport and ICT contributed to 10%, 9% and 7% of revenues respectively in FY17. The group expects Energy & Natural Recourses sector to show ongoing growth on a year on year basis. The Public sector spend is also forecasted to expand with East Coast growth. The group is also focusing on major growth opportunities in Finance & Insurance and ICT. As per the first quarter of 2018 highlights, WA region is showing solid growth especially in the mining / resources sector. The East Coast region performance is also on-track, but NZ performance is softer than expected due to the prolonged NZ government election. Overall, the group has signaled for a full year revenue, earnings as well as cash conversion growth in FY18, and reduction in net debt by year end.

.png)

Revenue by Industry (Source: Company reports)

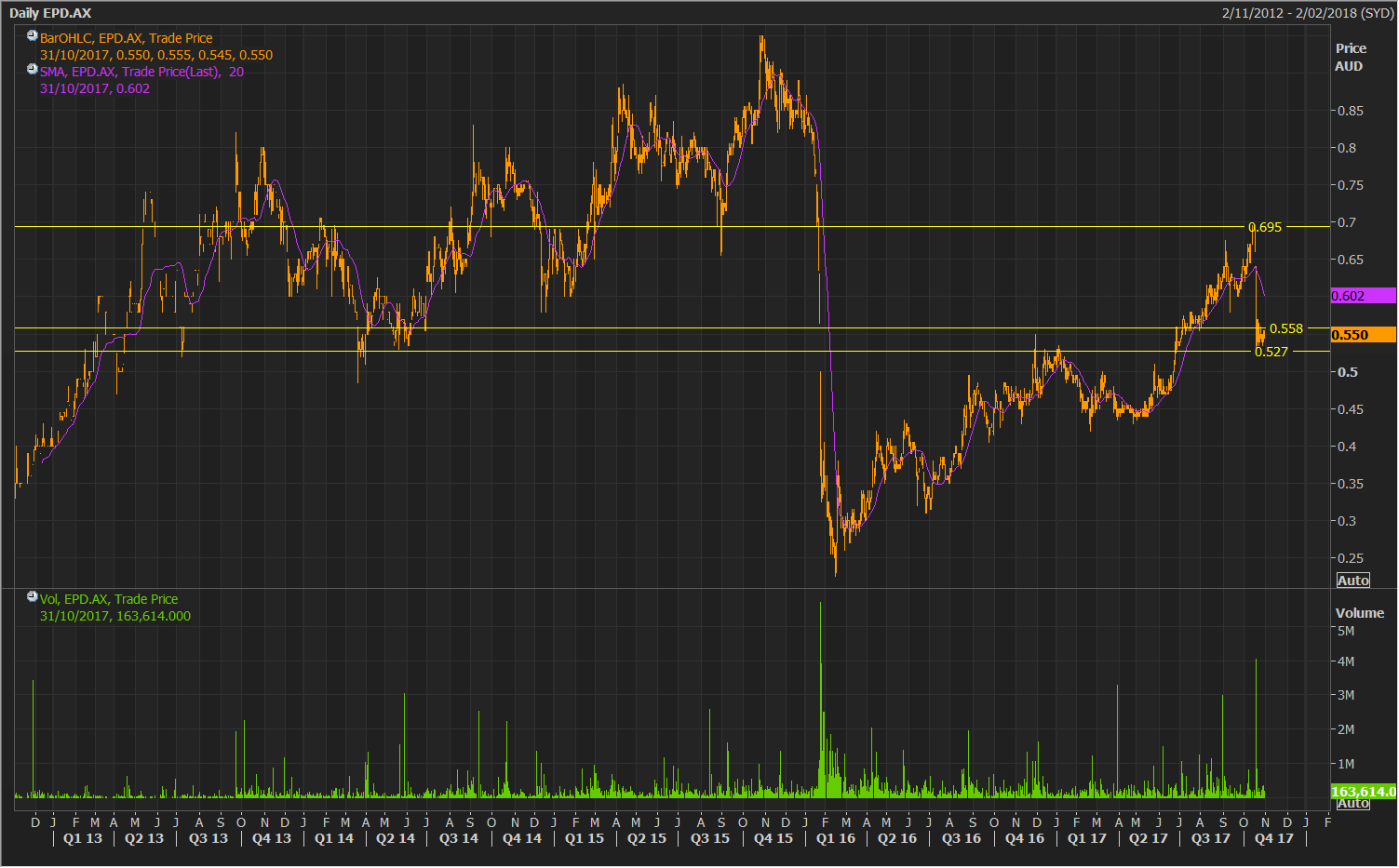

Stock performance: The shares of EPD fell 14% in the last four weeks (as of October 30, 2017) as the management gave a cautious outlook due to rising levels of volatility at the global level. On the other hand, the group has positioned itself well in the IT service market and has a competitive advantage in the SMAC market. The group controlled its debt, as well as invested heavily to compete and win against major players. EPD’s local management knowledge and resources are also said be differentiating it from the international players. The group lately responded to the ASX query by stating that they are in compliance with the Listing Rules and not aware of any other explanation for the recent trading in its securities. EPD stock otherwise delivered decent returns of over 22% in the last six months and seems to benefit from a healthy start to 1H18 with support from revenue growth translating into accelerated earnings growth and cash conversion, market consolidation and efforts on net debt reduction. In view of some anticipated impact from the softer than expected New Zealand performance in FY18 while the group has immense potential from its core regions and continuous business development activities, we give a “Speculative Buy” recommendation on the stock at the current price of $0.55

EPD Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...