Company Overview: EML Payments Limited, formerly Emerchants Limited, is a payments solutions provider of prepaid financial card products and services. The Company's segments include Australia Reloadable, Australia Non-Reloadable, Europe and North America. By using its payments software and processing platform, the Company provides its clients with financial service payment solutions for reloadable and non-reloadable prepaid card programs, in Australia, the United Kingdom and Europe, the United States and Canada. It offers various solutions, such as consumer lending, EachWay cash load solution and commercial solutions. It provides prepaid solutions, such as treasury, and compliance and fraud management. EachWay cash load solution allows customers to convert cash to value in their gaming account, and to deposit cash at a retailer for instant value in the gaming account. It delivers general purpose reloadable and non-reloadable prepaid card based solutions for clients across various industries.

.png)

EML Details

Strong Customer Demand Supported EML’s GDV: EML Payments Limited (ASX: EML), formerly known as Emerchants Limited, is a small-cap company with the market capitalisation of ~$425.35 million as on March 5, 2019. The group has a portfolio which offers innovative financial technology that gives solutions for pay-outs, gifts, incentives and rewards, and supplier payments. It demonstrated robust performance in 1H FY 2019 (six months ended December 2018) which was well-supported by significant growth in GDV (or Gross Debit Volume). GDV is the debit volume which is processed by EML via its proprietary processing platforms. The company generated GDV amounting to $4.15 billion in 1H FY 2019 representing a rise of 16% on the prior corresponding period (or PCP). GDV happens to be a proxy indicator of the customer demand for the company’s payment services. The YoY growth in GDV was a result of $300 million in organic growth from programs in the market for over 12 months and $270 million from programs in the market for less than 12 months. This growth also consists of contributions from the acquisition of Nordic and Irish subsidiaries. The company’s GDV had witnessed a robust 121% CAGR from HY 2016 to HY 2019 depicting increased market presence and robust customer demand. The company’s Gift & Incentive (or G&I) segment had witnessed GDV growth of 42% and stood at $660 million on the back of stable trading conditions in North American malls and rapid growth witnessed in Europe from newly launched malls. Overall, the company rolled out programs in over 100 malls in 1H FY 2019. The company generated total revenues amounting to $47.2 million reflecting a 23% rise over the prior corresponding period and EBTDA was $13.74 million implying a 50% rise over pro-forma PCP.

We expect that the company is in a strong position to address market demand because of its increased penetration, diversified presence, and decent liquidity levels. Moving forward, the company is expected to be aided by increased customer demand and the adoption of digital tools.

.png)

Gross Debit Volume (Source: Company Reports)

Decent Standing from Margins’ Standpoint: In FY18, EML Payments ended FY18 with a decent position with respect to its key margins. The company’s net margins stood at 3.1% in FY 2018 reflecting a YoY rise of 3.1% demonstrating the company’s capability to convert its top line into the bottom line. Also, the company’s operating margin stood at 7.9% reflecting a YoY rise of 11.6% which depicts the company’s cost-effective strategies. The company’s return on equity or ROE stood at 1.8% which reflects the company’s focus on delivering returns to shareholders.

Growth in Segments Aided Revenue Growth: As mentioned, EML Payments Limited witnessed 23% growth over PCP to $47.2 million and it witnessed revenue growth in all segments as Gifts & Incentives rose 49%, GPR (or General Purpose Reloadable) rose 13% and VANS was up 100%. The growth in the company’s revenues demonstrates the inherent diversification in business and the lack of reliance on one customer, segment or geography for the short-term or long-term success. We expect that the company’s increased penetration and diversification into different geographies would continue to drive its top line moving forward. The company’s revenues in the North American business witnessed a rise of 5% as the mall volumes rose 5% and the impact of moving mall programs to higher interchange BIN ranges yielded results.

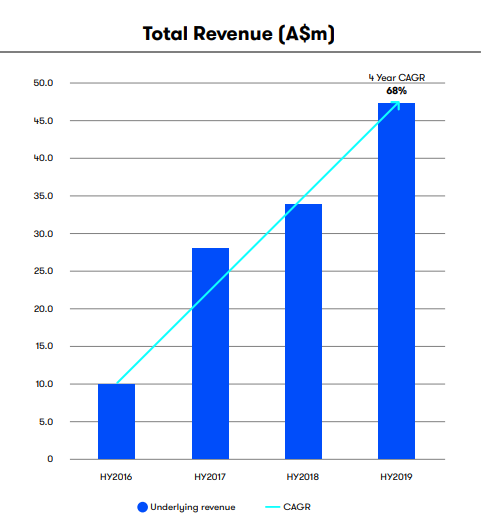

EML Payments generated 83% of the revenues in 1H FY 2019 from the recurring transactional revenue streams which were up 34% on a YoY basis. The company’s total revenues have grown at 68% CAGR from HY 2016 to HY 2019 which is the positive reflection of the company’s revenue generation capabilities. Over the long-term, we expect that the company’s robust revenue generation strategies coupled with the geographical diversification would continue to aid its long-term growth prospects. In 1H FY 2019, EML Payments witnessed a 50% rise in pro-forma PCP to $13.74 million in EBTDA which was backed by robust revenue growth because of organic and acquisitive business development.

Total Revenues Trend (Source: Company Reports)

Several Programs Supported EML’s G&I Business: EML Payments’ Gift & Incentive segment demonstrated robust performance as its GDV witnessed the growth of $197 million which was backed by growth in existing programs of 12%, newly launched programs of 47% and the newly acquired subsidiaries witnessed 41% growth. We expect that the company’s pipeline of new opportunities in all regions would drive the growth of the segment moving forward. With regards to G&I segment, the company had rolled out a mobile-based incentive solution and has signed 10 new US malls.

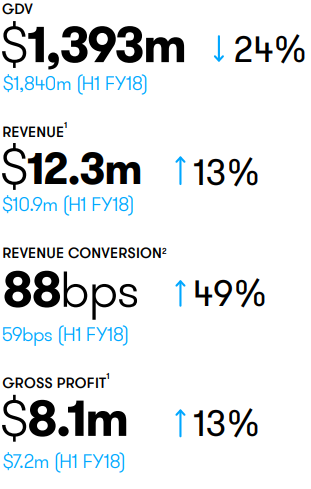

Understanding Performance of General Purpose Reloadable Segment: The company’s GPR segment witnessed a 13% rise in revenues to 12.3 million in 1H FY 2019 even though the GDV was down 24% on the prior period. The revenue was mainly driven by the decent organic growth in salary packaging & gaming business verticals during the same period. The Australian and European Sports Betting witnessed growth in GDV of 28% in 6 months as compared to the prior comparative period.

General Purpose Reloadable Segment Performance (Source: Company Reports)

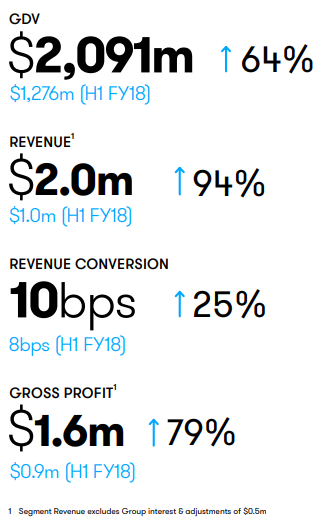

Strong Growth Witnessed in VANS’ GDV in 1H FY 2019: The Virtual Account Numbers (or VANS) segment witnessed the rise of 64% in its GDV to $2.09 billion in 1H FY 2019 as compared to the prior comparative period which converted to revenues of $2 million. The performance of this segment got aided by growth from both longstanding customers and the new customers which they acquired. EML also stated that the North America sales resources have been reallocated to focus towards the opportunities in North America Gaming vertical. The sales resources in VANS segment are focused towards large scale processing opportunities.

VANS Segment (Source: Company Reports)

Key Business Development Updates: In 1H FY19, EML Payments signed the first General Purpose Reloadable contract with Pointsbet, for recently legalised sports betting industry in New Jersey, USA. The announcement was made in November 2018 and the company rolled out in January 2019. Also, the company continues to increase the penetration of Salary Packaging vertical in Australia. When EML launched programs on July 1, 2017, it initially launched with 112,000 benefit accounts. EML’s market-leading solution has since won further share with the organic growth of 19,000 card accounts since inception, reflecting a growth of 13%, and, in January 2019, the company secured agreement for further 25,000 benefit accounts to launch in 2H FY 2019.

The company wrapped up its launch with ECE in Germany in October 2018. ECE happens to be the leading owner and operator of shopping malls in the country with 90 malls under management. Also, on July 4, 2018, the company made the acquisition of PerfectCard Group which is Ireland’s first authorized eMoney institution and FinTech company which gives incentive gift cards and corporate expense solutions. EML Payments rolled out its new mobile-based products using Pays technology in Australia (Apple Pay, Samsung Pay, and Google Pay) so that EML’s clients can reach their customers instantly. The company expects to roll out the offering in Europe and North America during the back half of calendar year (CY) 2019. Recently, EML announced that it has rolled out branded reloadable winnings card program with Betsson in Sweden. This programme provides cardholders with the ability to transfer their winnings from their gaming account onto the card instantly, anytime, anywhere giving them access to cash and usage anywhere Mastercard® is accepted. The aforesaid key business development might support the future growth prospects of the company.

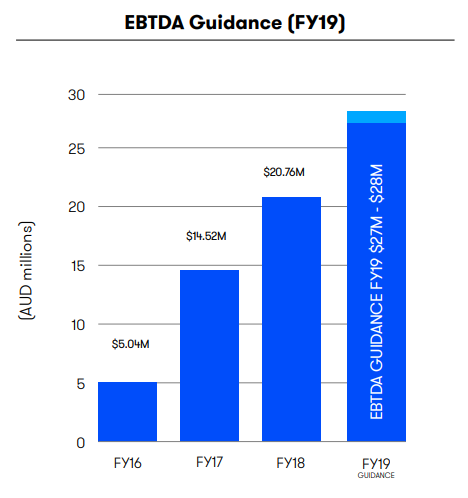

What to Expect From EML: EML Payments has tightened the EBTDA guidance towards the upper end of the range which was earlier given by the company which reflects a growth of 30%-35% on prior corresponding period. The assumptions for the same are that there would be no change to the present trading conditions, foreign exchange rates remain in line with rates as at December 2018 and with no significant Brexit impact as well as there would be no impact from the acquisitions. Also, the company has improved its FY 2019 guidance which might attract the investors’ attention. The revenues are expected between $88 million-$94 million in FY 2019 which has been changed from the earlier guidance of $82 million-$88 million. The company’s EBTDA might be in the range of $27 million-$28 million.

EBTDA Guidance (Source: Company Reports)

Stock Recommendation: In the last three months, the stock has risen by around 15.25% and is trading slightly towards 52-week higher level. A technical indicator, Exponential Moving Average or EMA has been used on the daily chart of EML, and default values were used for the purposes. After careful observation, it was noticed that the company’s stock price has crossed the EMA and moved upwards post the crossover which happens to be a bullish sign. Therefore, there are expectations that the company’s stock price might witness a rise moving forward. From the analysis standpoint, the company happens to be in decent position when it comes to liquidity levels as it has $50.1 million of cash on the balance sheet with no debt, thus, placing it in the strong position to cater to increased demand. From the valuation standpoint, the company is having the price-to-earnings (or P/E ratio) of 151.79x which is higher than the concerned industry median of 7.5x. Moreover, EML’s price-to-book ratio (or P/B ratio) stood at 3.0x as compared to the industry median of 2.0x which reflect that the company’s stock is trading at decent levels. Fundamentally, the company seems to be poised for robust growth in the forthcoming years supported by diversified business model, decent balance sheet position with improved financials in 1HFY19, solid sales pipeline, and continued contracts signings & program launches across all segments. EML is also making an effort to improve its ROE. Given the backdrop of aforesaid facts and current trading level, we give a “Speculative Buy” recommendation on the stock price at the current price of A$1.675 per share (down 1.471% on 05 March 2019).

EML Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...