Company Overview: Emeco Holdings Limited (Emeco) provides heavy earthmoving equipment rental solutions to mining companies and contractors. The Company's segments include Australia, Canada and Chile. The Australia segment provides a range of earthmoving equipment and maintenance services to customers in Australia. The Canada segment provides a range of earthmoving equipment and maintenance services to customers primarily in Canada. The Chile segment provides a range of earthmoving equipment and maintenance services to customers in Chile. Its rental fleet includes Caterpillar and Komatsu rear dump trucks of 50 to 240 tons; Komatsu, Hitachi, Liebherr and Caterpillar excavators of 40 to 400 tons; Caterpillar articulated trucks of 30 to 40 tons; Caterpillar dozers of D8 to D11; Caterpillar and Komatsu loaders of 966 to 994H; Caterpillar graders of 14H to 24M, and ancillary equipment, including water carts, service trucks, compactors, integrated tool carriers and tire handlers.

.png)

EHL Details

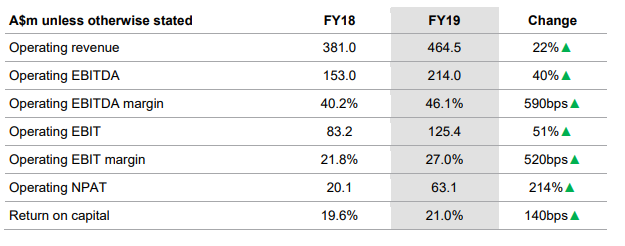

Decent Performance in FY19: Emeco Holdings Limited (ASX: EHL) is a small-cap company with the market capitalisation of circa $614.1 Mn as of September 03, 2019. It provides heavy earthmoving equipment rental solutions to mining companies and contractors across coal, gold, copper, bauxite and iron ore. Recently, the company released a decent set of numbers for FY19 with a significant rise in profitability. It reported operating NPAT amounting to $63.1 million, exhibiting uptick of 214% on a Y-o-Y basis. EHL’s operating EBITDA amounted to $214.0 million (which is up 40% on FY18) while operating EBIT stood at $125.4 million (reflecting a rise of 51% on FY18). The company stated that the robust growth in the earnings was because of the continued increase in the average operating utilisation to 64% (a rise from 58% in FY18), improvement in the rental rates, continued tight cost control, and full-year contribution from Force and Matilda Equipment.

EHL generated $90.1 million in the operating free cash flow (pre-growth capex) in FY19 that enabled the company to repay US$33.8 million of 9.25% senior notes and deploy towards strategic growth assets in order to drive future earnings. By the end of FY19, the company’s leverage down to 2.0x from 2.6x in FY18 and achieved a return on capital of 21.0%. The company’s Managing Director named Ian Testrow reflected favourable views with respect to the drop witnessed in its leverage and stated that, following recapitalisation and three-way merger transaction back in 2017, 2.0x leverage was a stated target for FY20 which has been achieved one year ahead of schedule. It was also mentioned that, in the capital-intensive business, they have a dedicated focus towards return on capital in order to ensure that they are efficiently utilising the capital.

The company stated that its objective in FY20 is to continue to deleverage by the growing earnings and using strong operating cash flow to reduce the debt levels. This will ensure that the company can refinance the notes on better terms at the optimal time to drive the shareholder returns. Additionally, there are expectations that the company’s decent capabilities to build cash levels and to generate revenues might act as tailwinds for long-term growth.

Operating Financial Results (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Emeco Holdings Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

YoY Improvement in Key Margins Reflect Improving Fundamentals: Emeco Holdings Limited has posted a net margin of 7.2% in FY19, which reflects a YoY rise of 5.8% and, thus, it looks like that the company’s capability to convert its top-line into the bottom-line has been improved. The company’s EBITDA margin stood at 42.8% in FY19, which implies a rise of 4.6% on a YoY basis.

.png)

Key Metrics (Source: Thomson Reuters)

The percentage of long-term debt to total capital of the company stood at 69.7% in FY19, which reflects a fall of 5.1% and, therefore, it looks like that EHL’s exposure towards the long-term debt component has been reduced. Importantly, it is to be noted that the deleveraged balance sheet is generally considered positive for the company as it reduces the long-term commitments. Therefore, a stabilised balance sheet helps the company in achieving long-term growth objectives.

Analysing Performance of EHL’s Rental Segment: The company’s revenue in rental segment witnessed a rise of 13.1% and stood at $401.7 million and its operating EBITDA margins increased from 47.3% in FY18 to 50.8% in FY19. It was stated that group operating utilisation witnessed a rise over FY19 averaging 64%, rising from 58% in FY18. However, gross utilisation averaged 90% in FY19. The rental growth was witnessed predominantly because of the robust demand from the customers in the metallurgical coal.

.png)

Rental Segment (Source: Company Reports)

Significant Increase in Workshops Throughput: With respect to workshops, it was stated that there was first full year contribution from the Force Workshops. During FY19, the workshops activity has increased significantly as a result of (1) capacity expansion with new locations throughout Australia, and (2) increased retail work and work on Emeco Rental fleet. Moreover, total workshops activity witnessed a significant rise from $41.8 million in FY18 to $114.7 million in FY19, displaying a growth of 174.4% on YoY basis. The operating EBIT contribution from retail earnings increased by 78% to $4.7 million. All the overheads, which includes additional overheads associated with the 3 new workshops, are allocated to retail earnings.

.png)

Workshops (Source: Company Reports)

Overview of EHL’s Cash Flow: On the back of the robust profitability in FY19, the company generated $90.1 million in operating free cash flow (pre-growth capex) which enabled it to repay US$33.8 million of its 9.25% senior notes and invest in strategic growth assets to drive future earnings. The company’s operating EBITDA witnessed a rise from $153.0 million in FY18 to $214.0 million in FY19. The prudent investment towards growth assets in FY19 resulted in the net operating cash flow decreased to $5.0 million as compared to FY18 figure of $77.7 million. However, excluding the investment in growth assets, operating free cash flow amounted to $90.1 million.

.png)

FY19 Operating Cash Flow (Source: Company Reports)

It was added that growth assets which were acquired in the year for the consideration amounting to $85.1 million (including prep costs) were fully financed via free cash flows and new finance lease facilities. The company also stated that no significant growth capex has been anticipated for FY20.

Total Outstanding Debt Witnesses A Fall: Emeco Holdings Limited stated that its total outstanding debt witnessed a reduction of $16.6 million because of repurchase of US$33.8 million of outstanding notes, offset by an increase in the finance lease liabilities as a part of growth asset acquisition and impacts of foreign currency translation until debt was fully hedged. The A$40 million revolving credit facility (or RCF), which consists of A$35.0 million cash advance facility and A$5.0 million bank guarantee facility maturing in the month of March 2020, was refinanced in the month of September 2018 and was replaced with A$65.0 million facility maturing in September 2021.

.png)

Leverage (Source: Company Reports)

The company’s cash balance witnessed a fall to $36.2 million as at June 30, 2019, mainly due to cash on hand at June 30, 2018 was used towards financing the acquisition of Matilda, in addition to deployment towards growth assets and repurchasing notes. Notably, the company’s leverage ratio witnessed improvement from 2.6x at June 30, 2018, to 2.0x at June 30, 2019. There are expectations that the leverage would continue to decrease in FY20 because of increased earnings and cash flows.

What to Expect from EHL Moving Forward: EHL is expecting to witness additional growth in the revenue and earnings in FY20, with the greater weighting to the earnings in 2H FY20. While the company expects continued demand in the metallurgical coal, particularly as the customers remain disciplined with the capital expenditure allocation. The company is also focused on diversifying Eastern Region exposure to gold and copper. It was also added that improving conditions in the Western Region have been observed in early FY20 with around 100 pieces of equipment committed into new gold and iron ore projects. However, full benefit of the earnings is not anticipated to be realised until 2H FY20. The company expects to allocate some growth assets and assets from thermal projects to Western Region to meet the fleet requirements.

.png)

Long-Term Value Creation Model (Source: Company Reports)

At a higher level, the company would be investigating opportunities to further build on the business model and widen its value proposition in order to achieve growth as well as sustainability through the cycle. The company happens to be committed towards being the lowest cost and highest quality provider of earthmoving equipment with the help of its asset management capabilities, enhanced use of technology and business improvement initiatives. It was stated that the company’s long-term value creation model revolves around generating returns, reinvest in the business, offering compelling customer value propositions and optimising through expertise.

.png)

Key Valuation Metrics (Source: Thomson Reuters)

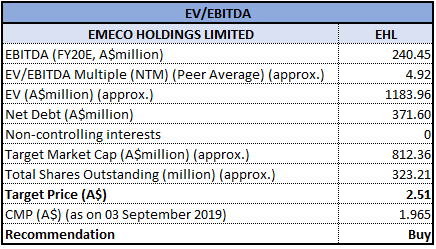

Valuation Methodology: EV/EBITDA Multiple Approach

EV/ EBITDA Multiple Approach (Source: Thomson Reuters) *NTM-Next Twelve Months

Stock Recommendation: The stock of Emeco Holdings Limited has delivered the return of 7.95% in the span of previous three months while, in the time frame of past one month, the stock has fallen 16.30%. Currently, the company’s stock is trading towards the 52-week lower levels of $1.630, proffering a decent opportunity for accumulation. The company has reduced the gross debt through the purchase of US$33.8 million in senior notes, decreasing the ongoing financing costs. Additionally, it is committed towards further deleveraging by reducing the gross debt and growing the earnings to ensure the note refinancing on better terms. Moreover, the company has decent revenue-generation capabilities as its top-line has witnessed a CAGR growth of 17.78% in the time span of between FY15- FY19 and, thus, it looks like that its capabilities to generate revenues might help it in achieving growth over the long-term. Based on the foregoing, we have valued the stock using a relative valuation method, EV/EBITDA multiple, and have arrived at the target price upside of double-digit growth (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$1.965 per share (up 3.421% on 3 September 2019).

(1)(1).png)

EHL Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...