Company Overview: Emeco Holdings Limited (Emeco) provides heavy earthmoving equipment rental solutions to mining companies and contractors. The Company's segments include Australia, Canada and Chile. The Australia segment provides a range of earthmoving equipment and maintenance services to customers in Australia. The Canada segment provides a range of earthmoving equipment and maintenance services to customers primarily in Canada. The Chile segment provides a range of earthmoving equipment and maintenance services to customers in Chile. Its rental fleet includes Caterpillar and Komatsu rear dump trucks of 50 to 240 tons; Komatsu, Hitachi, Liebherr and Caterpillar excavators of 40 to 400 tons; Caterpillar articulated trucks of 30 to 40 tons; Caterpillar dozers of D8 to D11; Caterpillar and Komatsu loaders of 966 to 994H; Caterpillar graders of 14H to 24M, and ancillary equipment, including water carts, service trucks, compactors, integrated tool carriers and tire handlers.

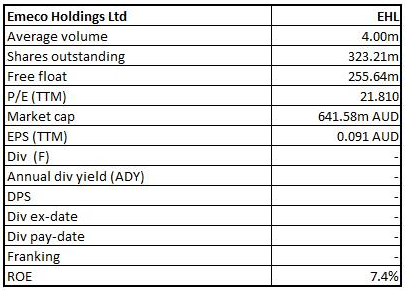

EHL Details

1H FY 2019 Results Primarily Aided By Recent Acquisitions: Emeco Holdings Limited (ASX: EHL) is an ASX listed company which is engaged in the provision of safe, reliable and maintained earthmoving equipment solutions to the customers which are in the earthmoving industry as well as the maintenance and remanufacturing of major components of heavy earthmoving equipment. As on June 18, 2019, the market capitalisation of Emeco Holdings Limited stood at ~A$641.58 million. The company had earlier released its results for the half-year ended December 31, 2018 in which it reported operating net profit after tax amounting to $31.7 million which reflects a rise of $19.5 million from 1H FY 2018. The company’s operating revenue for 1H FY 2019 amounted to $224.3 million, which implies a rise from $171.1 million in 1H FY 2018. In 1H FY 2019, the company’s rental revenue amounted to $182.4 million which is up 17.7% from $155.0 million in 1H FY 2018 because of the full contribution from acquisition of Force Equipment (which got wrapped up on November 30, 2017) and Matilda Equipment (which got wrapped up on July 2, 2018), improvement with respect to operating utilisation as well as continued strength in Eastern Region, particularly the coal mining customers. The company’s maintenance services revenue amounted to $41.4 million, which implies a rise of 170.6% from $15.3 million in 1H FY 2018 because of the full contribution of earnings and increased workshop activity in 1H FY 2019 in comparison to one-month contribution from Force workshop in 1H FY 2018. The company stated that its operating EBITDA and operating EBIT margins stood at 45.8% and 26.7%, respectively and the increases were because of high margin earnings from Matilda Equipment, implementation of the innovative win / win customer contracts, cost management in the disciplined way as well as extensive use of Force workshops in order to minimise the cost of preparing equipment for the projects.

Moving forward, tailored rental agreements, focus towards deleveraging the balance sheet, quality workmanship as well as focus towards optimising the capital structure to reduce the WACC are expected to act as tailwinds.

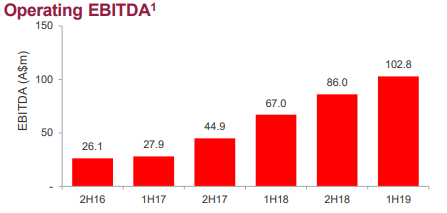

Operating EBITDA (Source: Company Reports)

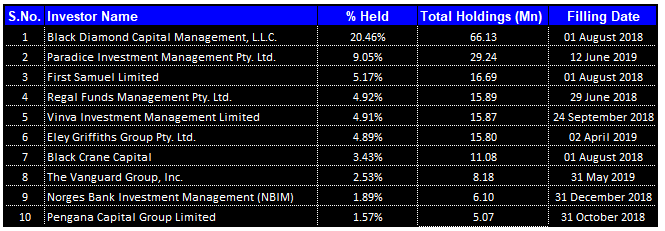

Top 10 Shareholders: The following table gives the broader picture of the top 10 shareholders of Emeco Holdings Limited:

Top 10 Shareholders (Source: Thomson Reuters)

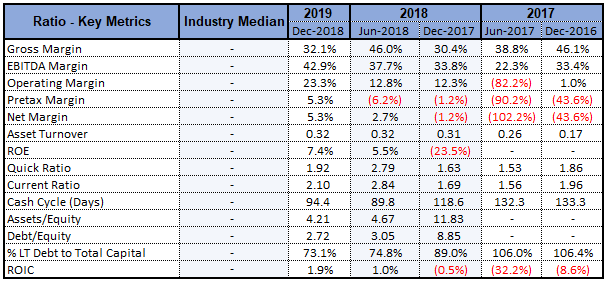

Improvement in Key Margins: Emeco Holdings Limited had witnessed a YoY improvement in its key margins which builds confidence in its key operational capabilities. The company’s net margin stood at 5.3% in 1H FY 2019, which reflects a rise of 6.5% on the YoY basis that implies an improvement in the capability to convert its top-line into the bottom line. Also, the company’s operating margin stood at 23.3% in 1H FY 2019, which reflects a YoY improvement of 11%.

Key Metrics (Source: Thomson Reuters)

Talking about the liquidity levels, its current ratio stood at 2.10x, which implies an improvement of 23.9% on the YoY basis, reflecting that the company is in a better position to meet the short-term obligations. Also, the sound liquidity levels provide sufficient headroom for deployments towards long-term growth catalysts. The company’s Debt/Equity ratio was 2.72x in 1H FY 2019, which reflects a significant fall of 69.2% and, thus, it can be assumed that the company’s balance has been deleveraged which can be considered as a positive sign. During 1H FY 2019, the company had continued on the path of earnings growth, margin improvement, increasing utilisation as well as reducing leverage.

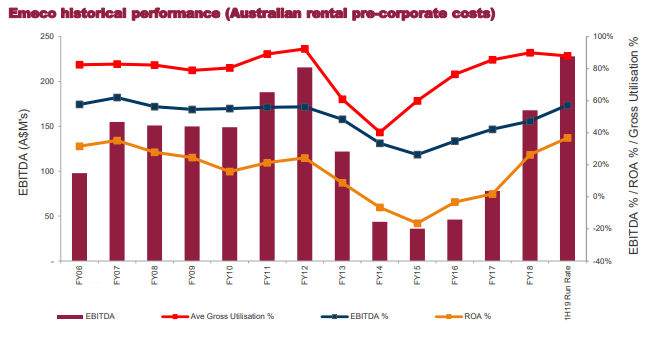

Key Takeaways from Investor Conference Presentation: In the investor conference presentation, Emeco Holdings Limited threw light on its long-term value creation model which revolves around generating returns, reinvestment in the business, offer compelling customer value propositions as well as optimising through expertise. With respect to generate returns, the company focuses on providing attractive shareholder returns, servicing debt, maintaining the robust balance sheet in order to support investment as well as optimising the capital structure to reduce the WACC (or Weighted Average Cost of Capital). The company had witnessed an improvement in its EBITDA, margins and return on assets and it is committed towards ensuring sustainability through capex and commodity cycles. The following chart provides a clear picture:

Emeco Historical Performance (Source: Company Reports)

The company is focused towards ensuring the healthy balance sheet through the cycle and it is committed towards an aggressive deleveraging path. The company stated that its objective is to refinance the notes on more attractive terms which could help in reducing the finance costs. However, dividends as well as share buy backs would be considered post-note refinance.

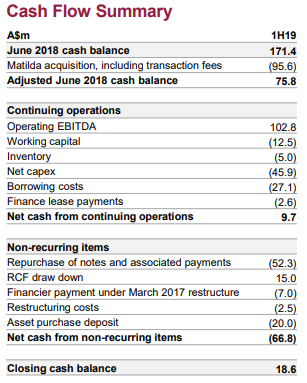

How Emeco’s Cash Flow Trended: Emeco Holdings Limited stated that, based on its confidence in market as well as the business’ ability to generate the strong operating cash, the company made significant deployments during 1H FY 2019. The company had used the surplus cash at the time for the reduction in its future coupon costs by approximately $5.0 million per annum. As per the company’s 2019 interim results presentation, finance lease payments are anticipated to stay flat moving forward notwithstanding new leases to be implemented to fund the asset purchase. The company is focused towards sustainably creating the shareholder value by being highest quality as well as lowest cost provider of the earthmoving equipment solutions.

Cash Flow Summary (Source: Company Reports)

Share Consolidation: As per the release dated November 27, 2018, Emeco had earlier advised that 10 to 1 share consolidation, which got approved by Emeco shareholders at 2018 annual general meeting on November 15, 2018, had been completed. It was also stated that the proposed share consolidation would be resulting in the company appealing to broader investor base, providing the additional liquidity and reduction in the share price volatility.

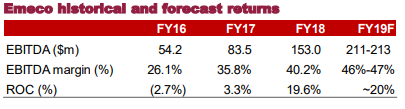

What To Expect From Emeco Holdings: Emeco Holdings Limited had forecasted operating EBITDA to witness a rise of around 40% on YoY basis in the range of $211 million and $213 million in FY 2019. The company stated that the market conditions are being positive and the outlook for FY 2020 happens to be strong. The company’s growth capex from the recent purchase of high-utilisation assets is anticipated to come in below the budgeted $90 million expenditure, and also there is a target to generate $25 million of EBITDA in FY 2020.

Emeco Historical and Forecast Returns (Source: Company Reports)

Emeco stated that deleveraging happens to be a strategic priority and it is forecasting leverage to be 2.1x by FY 2019 end. However, it is also targeting leverage to be 1.0x by FY 2021. The company added that the robust cash flow in FY 2020 assists with de-leveraging and would be allowing the company to refinance the $US notes in the future on more favourable terms. There are expectations that the ROC (or Return On Capital) would be around 20% in FY 2019, which happens to be the highest since IPO and is up from 13% in previous cycle peak (i.e., FY 2012) with the headroom for further upside through increased rental rates as well as utilisation.

In FY19 guidance, operating update and investor presentation and with respect to Western Rental Region, the company stated that the bidding activity has increased and there has been winning of the new contracts and the company is awaiting award on the number of additional major projects. The company has no operational or financial impact from the recent announcements with regards to certain gold projects in WA.

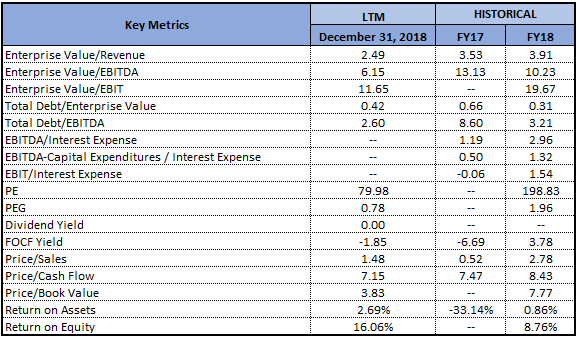

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

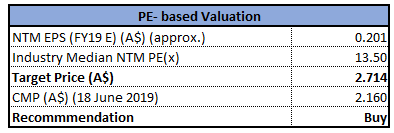

Method 1: PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

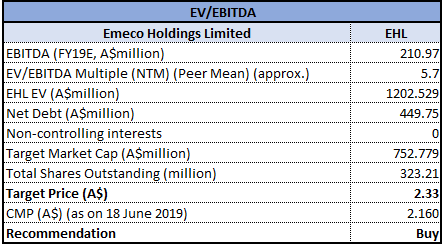

Method 2: EV/EBITDA Multiple Approach

EV/ EBITDA Multiple Approach (Source: Thomson Reuters) *NTM-Next Twelve Months

Stock Recommendation: The top line of Emeco Holdings Limited has witnessed a CAGR growth of 12.12% in the time from FY 2014- FY 2018, which could be considered at respectable levels and reflects its capabilities to generate revenues. The company stated that reducing the component costs as well as extending the component life provides it with the competitive advantage. Additionally, the company is committed towards the robust balance sheet which could act as a tailwind for the long-term growth and that might attract the attention of the market players. Emeco would be ensuring the strict capital management discipline in order to ensure robust returns through the cycle. The company is focusing on deleveraging through to FY 2021. The company stated that acquisition and the integration of Matilda Equipment is performing in line with the anticipation.

Also, there has been a significant YoY improvement in Emeco’s RoE which might also help it in gaining traction among the market players. In 1H FY 2019, its RoE stood at 7.4%, which implies a rise of 30.9% on the YoY basis, showing that the company has been efficient in delivering returns to its shareholders. Considering the company’s focus on providing attractive returns to the shareholders and maintaining healthy balance sheet position, we are affirmative on the company and presume that the company might continue to achieve respectable growth in the long run.

However, the stock has delivered a negative return of 10.59% in the span of previous three months, while in the time frame of past one month, its return stood at 6.72% and is trading below the average of 52 week high and low prices of around $2.84 with a beta of 0.80x (5-Years, Monthly), proffering a decent opportunity for accumulation. Based on the foregoing, we have valued the stock using two relative valuation methods, P/E and EV/EBITDA multiple and arrived at the target price in the range $2.3-$2.7 (lower double-digit upside (in %)). Hence, considering aforesaid facts and current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$2.160 per share (up 8.816% on 18 June 2019).

EHL Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...