Kalkine has a fully transformed New Avatar.

Company Overview: Elders Limited is engaged in the provision of livestock, real estate and wool agency services; services and farm inputs; financial services; real estate franchise; live export operations; feedlotting of cattle; grain trading, and red meat supply chains. The Company's segments include Network, which includes the provision of agricultural retail products; Feed and Processing, which includes the Australian cattle feedlot near Tamworth in New South Wales (Killara Feedlot), the Indonesian cattle feedlot near Lampung (PT Elders Indonesia), and Elders Fine Foods, which is involved in the importation and distribution of Australian and New Zealand food products throughout China; Live Export, which facilitates the trades of dairy, beef feeder, beef slaughter and breeding cattle, and sheep from Australia and New Zealand to international markets by sea or air freight, and Other, which includes the general investment activities and the administrative corporate office activities.

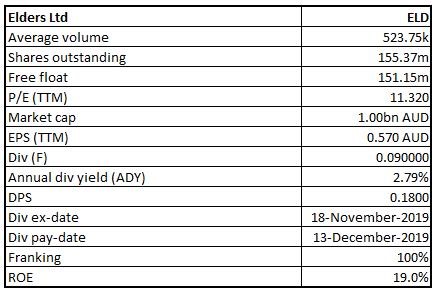

ELD Details

Elders Limited Reported Decent FY19 Results: Elders Limited (ASX: ELD) is primarily involved in the provisioning of retail products and associated services to the rural sector and livestock and wool agency services. As on December 2, 2019, the market capitalisation of Elders Limited stood at A$1 billion. The company reported a decent set of numbers for FY19, in-line with the guidance. The company has continued to deploy towards growth initiatives, which are likely to help in overall growth, moving forward. The company’s statutory net profit after tax stood at $68.9 million and underlying net profit after tax came in at $63.6 million, in-line with pcp. The impact of reduced summer cropping and lower wool volumes were offset by earnings from the recent acquisitions. The company’s underlying EBIT posted a marginal downtick of 1% to $73.7 million as compared to the prior year’s result of $74.5 million. ELD’s return on capital stood at 18.2%, below the company’s target of 20%, but almost twice its weighted average cost of capital. Elders Limited declared a fully franked final dividend of 9 cents per share, and the full-year payout comes out to 18 cents per share fully franked, in-line with the previous year.

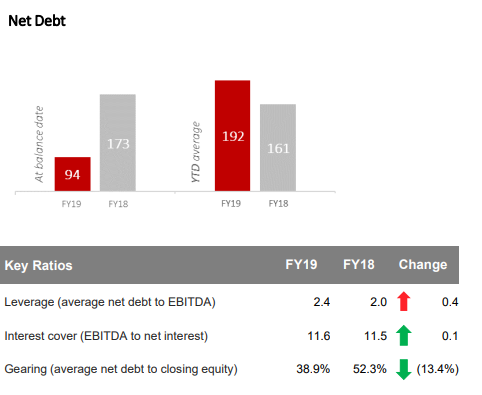

Net Debt (Source: Company Reports)

The net debt at balance date stood at $79 million, which is lower than prior year. This was primarily because of the proceeds which were received from the equity raised, net of the transaction as well as capital raise costs, for Australian Independent Rural Retailers (or AIRR) acquisition amounting to $130 million. The company’s FY19 results reflected the advantages of pursuing acquisitions that meet the company’s stringent investment criteria. Both TitanAg and Livestock in Transit products are delivering increased earnings, that are helping to offset the lower margins in retail business from reduced summer cropping and the impact of lower wool volumes on agency business. The company added that a new Rural Bank distribution agreement would be generating a stable income stream exceeding $10 million per annum during the term, apart from enhancing the ability to provide customers with the high-quality banking services.

The company stated that although summer crop outlook happens to be difficult, the average winter crop seasonal conditions would be providing a robust platform for business. Moreover, in FY 2020, business development along with improvement initiatives, are expected to act as tailwinds for achieving robust growth.

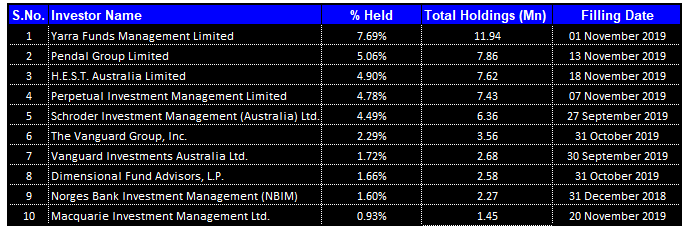

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Elders Limited:

Top 10 Shareholders (Source: Thomson Reuters)

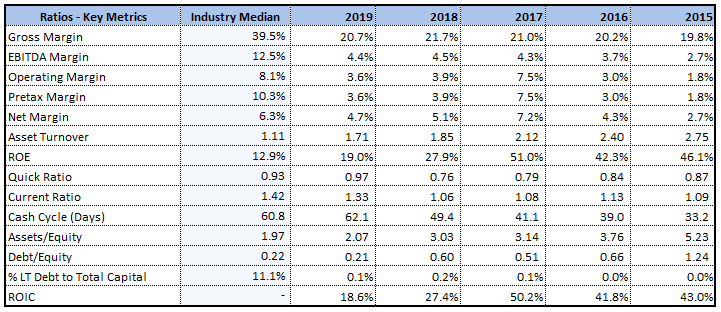

Improvement in Key Margins: The company’s return on equity stood at 19.0% in FY19, which is above the industry median of 12.9%. Its debt to equity ratio is 0.21x in FY19, which is slightly below the industry median of 0.22x. Thus, it can be said that ELD’s balance sheet is less leveraged as compared to the broader industry.

Key Metrics (Source: Thomson Reuters)

Over the last five years, the company has maintained its gross margin within the range of 19.8% in FY15 to 20.7% in FY19. Also, there has been a significant improvement in EBITDA margins and net margins during the same time period. Its EBITDA margins stood at 2.7% in FY15, which has improved to 4.4% in FY19 and its net margins have also improved from 2.7% in FY15 to 4.7% in FY19. An improvement in net margins reflects that ELD’s capabilities to convert top-line into bottom-line have been improved. Notably, the company’s current ratio stood at 1.33x in FY 2019 as compared to FY 2018 figure of 1.06x and, therefore, ELD has improved its capabilities to meet its short-term obligations. Also, respectable liquidity footing can help the company in making deployments towards growth initiatives.

Eight Point Plan: The company is confident about its Eight Point Plan and has reaffirmed that this strategic plan is on track to deliver 5-10% growth in earnings before interest and tax (or EBIT) through the agricultural cycle to 2020. The company reshaped cost and capital base of the business under the first Eight Point Plan to ensure that it could deliver good results in bad seasons for the shareholders. During the second Eight Point Plan, the company focussed towards management of the portfolio to ensure an optimum diversification through the product and service, business model and geography.

Strategic Priorities (Source: Company Reports)

Performance of Rural Products and Agency Services: The rural products margins improved by 3% (or $4.0 million) in FY19 as compared to the previous year, mainly due to the acquisition of TitanAg. The dry conditions in key areas has continued to subdue demand when it comes to crop protection as well as fertiliser, with northern New South Wales most affected. The agency margin declined by 3% (or $3.2 million) in FY19, mainly due to lower wool activity, with fewer bales sold across all geographies in line with the overall fall in the market.

Real Estate Margin Witnessed Improvement: The real estate margin improved by 2% (or $0.7 million) in FY19 on the YoY basis, with Southern and Western geographies driving the uplift. Despite the ease of cattle prices as well as drought conditions, that continue to affect Northern Australia, Broadacre turnover increased as compared to the last year. Also, property management and turnover for the water broking services contributed towards upside for the year.

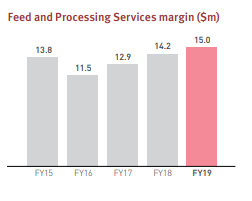

Financial Services and Feed and Processing Services: Financial Services margin were down by 13% (i.e. $4.9 million) in FY19 as compared to last year mainly due to the new relationship agreement with Rural Bank resulting in margin decline (or $6 million), which was offset by cost savings amounting to $6 million post enactment. Killara gross margin rose by $1.4 million (or 10%) as compared to prior year, which was mainly as a result of higher utilisation and throughput. The strategy with respect to Feed and Processing Services revolves around delivering continuous improvement in the EBIT as well as ROC for all businesses with active portfolio composition management.

Feed and Processing Services margin ($ million) (Source: Company Reports)

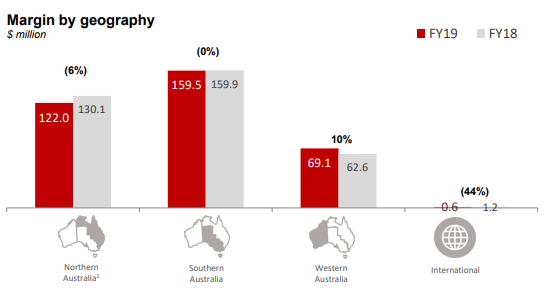

Performance by Geographies: In Northern Australia, the margins have declined by 6% on the YoY basis and it was mainly impacted by the dry conditions with reduced activity across mainly wool and rural products. In Southern Australia, the margins were flat on the YoY basis, and the impact of acquisitions was offset by lower wool volumes as well as higher costs. In Western Australia, the margins were improved by 10% in FY 2019 on the YoY basis and there was upside across most of the products, and acquisitions have boosted Rural Products result. Internationally, the margins fell by 44% in FY 2019 as compared to FY 2018, however, lower margins were offset by the cost savings.

Margin by geography ($ million) (Source: Company Reports)

Financial Position of the Company: The company’s working capital as at September 2019 stood at $287.1 million, 19% higher than previous year. This primarily relates to higher trade and other receivables due to higher livestock debtors with early timing of spring sales and additional StockCo advances (livestock funding investment) through the provision of short-term funding. The average working capital increased by $51.7 million to $288.6 million for the year. As mentioned, the company’s Debt/Equity ratio is lower than the industry median and, therefore, it can be said that ELD’s balance sheet is less leveraged as compared to the broader industry. Generally, a less leveraged balance sheet reflects stability and, as a result, the company could focus on its growth objectives as it can make deployments towards strategic growth objectives.

Outlook for FY20: The company expects that average winter crop seasonal conditions will provide a solid platform for the business, however, the summer crop outlook remains difficult. In July, the company made an announcement about the acquisition of Australian Independent Rural Retailers (or AIRR), which is an excellent strategic fit. It will provide Elders with additional growth channels through entry into the wholesale rural services market and the produce and hobby farmer services market. The acquisition has the capacity to add 20% to 25% growth to Elders at the EBIT level on full year basis. The company is targeting 5% to 10% per annum quality growth through the agricultural cycle, while maintaining a return on capital between 15-18%, which is in-line with the Eight Point Plan and the three-year goal to FY20. This improvement in EBIT is expected to be derived from organic and acquisition growth and constant focus on regulating base costs to offset inflationary increases.

With respect to Rural Products, the company stated that the completion of AIRR acquisition would be providing entry to the wholesale market as well as increase the product diversification. However, as far as Real Estate Services are concerned, the demand for the farmland property is expected to remain robust and gains are anticipated from the residential as well as property management..png)

Key Valuation Metrics (Source: Thomson Reuters)

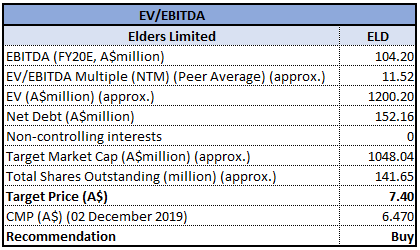

Valuation Methodologies: EV/EBITDA Multiple Approach

EV/EBITDA Multiple Approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters.

Stock Recommendation: In the span of previous six months, the stock of ELD has witnessed an increase of 5.84% while, in the past one month, the stock rose 8.40%. The company stated that costs are anticipated to increase which is in-line with the growth in footprint as well as continued Eight Point Plan investment. Also, there are expectations that increased deployment towards digital as well as technical areas and information technology might be continued. The company stated that the specialist independent consulting arm, Thomas Elder Consulting has been helping to broaden the services, applying its skills as well as expertise in the whole farm management throughout all areas of clients’ operations. Considering the aforesaid facts, we have valued the stock, using one relative valuation method, i.e., Enterprise Value to EBITDA multiple, and arrived at a target price of lower double-digit growth (in % term). Based on the foregoing, we give a “Buy” recommendation on the stock at the current market price of $6.470, up 0.31% as on 02 December 2019.

.png)

ELD Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...