Kalkine has a fully transformed New Avatar.

Company Overview: Echo Resources Limited is an Australia-based company engaged in exploration for mineral resources. The Company is focused on Gold in the Yandal Belt region of Western Australia. The Yandal Gold Project is located in the northern part of the Eastern Goldfields, and hosts the Julius Gold Project, as well as a range of prospective targets. The Company holds approximately 915 square kilometers tenement package across the Yandal Gold Province. The Julius Gold Project is located approximately 450 kilometers north of Kalgoorlie and over 70 kilometers east of Wiluna. The Zaphod Prospect is located within the southern part of the tenement package and within approximately 10 kilometers of multi-million ounce Gold deposits. The Company has also identified a range of regional targets at the Yandal Project. The regional prospects include Tipperary, Wimbledon, Bill's Find, Orpheus and Shady Well.

.png)

EAR Details

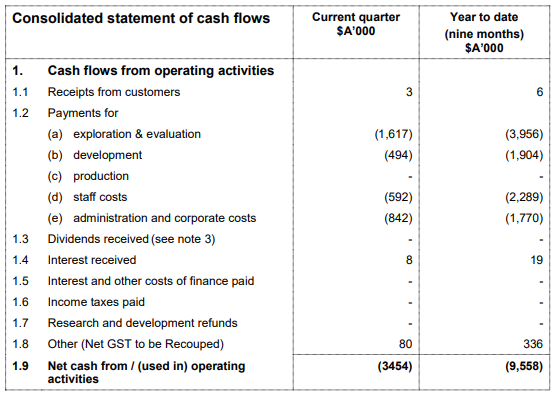

Yandal Gold Project Possesses Healthy Financial Metrics: Echo Resources Limited (ASX: EAR) is engaged in the gold exploration business with the large and highly prospective ground position in Eastern Goldfields of Western Australia. As on May 31, 2019, the market capitalisation of Echo Resources stood at ~$86.16 million. The company had recently released the results for the quarter ended March 2019 in which it stated that The Bankable Feasibility Study (or BFS) had confirmed the redevelopment of the Yandal Gold Project as technically robust with strong financial metrics. The key operating metrics of BFS consist production of 378,874oz over the initial 4-year life of mine and average annual gold production of 95,000 oz. However, it also consists of LOM all-in sustaining cost (AISC) amounting to A$1,095/oz. The company also stated that the Mining approvals have been received for both Julius and Orelia deposits at the Yandal Gold Project from the West Australian Department of Mine, Industry Regulation and Safety. In the March quarter, the net cash used in operating activities amounted to A$3.454 million, and the company had incurred $1.617 million payment towards exploration and evaluation. The financial highlights from BFS include the low pre-production capital amounting to $42 million and pre-tax project free cashflow which amounted to $225 million. These highlights also include pre-tax NPV amounting to $172 million as well as IRR of 198%. The company is considering all the strategic options in order to maximise the shareholder value ahead of progressing to production. With respect to exploration activity, the company mentioned about the outstanding drilling results at the Mount Joel Gold Project. Importantly, top-line of the company has grown significantly at a CAGR of 133.8% over the past four years (FY15-18), which reflects the strength in its revenue-generation capabilities.

Operating Cash Flow Statement (Source: Company Reports)

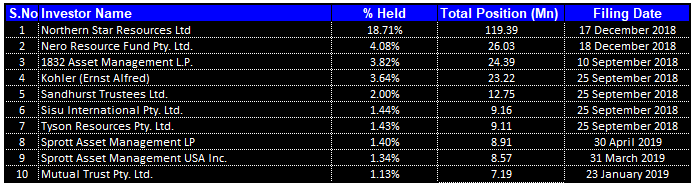

Top 10 Shareholders: The following table gives the broad picture of the top 10 shareholders of Echo Resources Limited:

Top 10 Shareholders (Source: Thomson Reuters)

Improvement in Key Ratios: In FY18, Echo Resources Limited had witnessed an improvement in its key financial ratios on the YoY basis. The company’s Assets/Equity ratio stood at 1.58x in 1H FY 2019 which is lower than the industry median of 1.70x and, therefore, it looks like the company’s assets are largely being financed via equities, and it has a lesser dependency on the debt. In most of the cases, lower debt on the balance sheet is considered favourable for the company at large, because it reflects a deleveraged balance sheet which might be considered positive for the long-term.

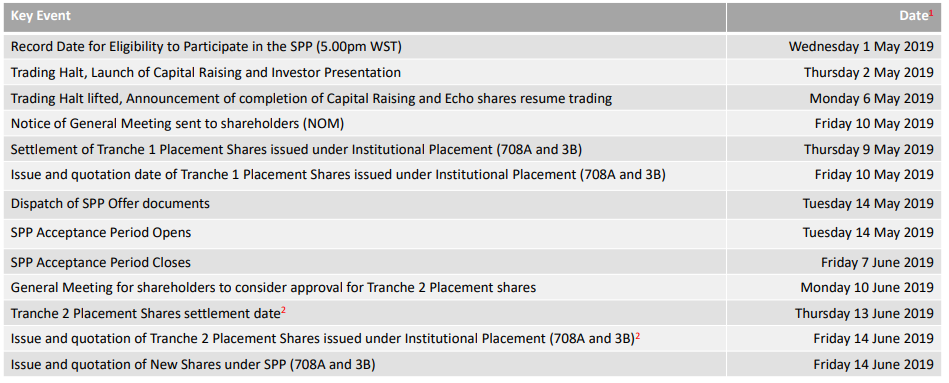

Key Insights into EAR’s May 2019 Investor Presentation: Echo Resources Limited recently published the May 2019 investor presentation in which the company gave the overview of the equity raising. The company detailed about the institutional placement in order to raise around A$15 million through two tranche placement which comprises A$11.3 million underwritten share placement of around 87.3 million new Echo shares (i.e., Tranche 1), and A$3.7 million conditional share placement of around 28.4 million New Shares (i.e., Tranche 2). The company also proposes to undertake Share Purchase Plan capped at A$3 million at same issue price as institutional placement.

The offer price has been determined at A$0.13 per new share which, as at last closing price on May 1, 2019 represents a discount of 7.1% to the last closing price of A$0.140 and discount of 12.8% to 5-day VWAP (volume weighted average price) of A$0.149. However, it also reflects a discount of 13.2% to 10-day VWAP of A$0.150. The proceeds are expected to be utilised towards Fund exploration strategy (i.e., around $12 million), and working capital and cost of Placement and SPP (i.e. around $3 million). However, up to $3 million of the proceeds received as a result of SPP would be utilised towards further exploration activities at the Yandal Gold Project.

Equity Raising Timeline (Source: Company Reports)

With respect to Bronzewing Processing Hub, the company stated that all the major infrastructure and plant which is required to support the restart of operations happen to be in place and the cost of replacement is approximately A$100 million.

.PNG)

EAR's Strategic Asset (Source: Company Reports)

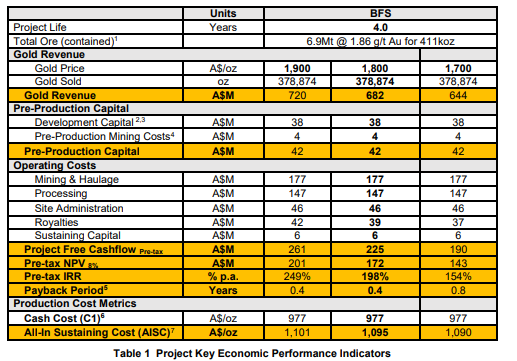

Broad Overview of Yandal Gold Project: The Bankable Feasibility Study reflects that under the conservative mining, processing and discount rate assumptions, it would be generating robust cash flows and returns on capital invested with the competitive operating costs and minimal pre-production capital. The Board is of the view that the pursuit of corporate opportunities and focussed resource conversion and regional exploration would be providing the company with significant return than immediately progressing to production. There are several identified, advanced projects and exploration targets within the company’s tenure and, thus, there is potential to increase the yearly production above 100,000oz per annum from the multiple mines, extend mine life and create a more profitable and sustainable business in years to come.

Project Key Economic Performance Indicators (Source: Company Reports)

Brief Overview of Recent Updates: With respect to the placement amounting to $15 million in order to fund the exploration strategy, Echo Resources Limited had stated that the placement is being supported by numerous high quality new and existing, domestic as well as international institutional investors. Also, Echo’s largest shareholder, Northern Star Resources Limited, has subscribed for around $3.4 million in Placement, on pro-rata basis according to the current shareholding in Tranche 1, and in Tranche 2 subject to the approval of shareholder.

As per the release dated May 14, 2019, the Share Purchase Plan allows for the participation of eligible shareholders for an amount of up to $15,000 per shareholder, involving a price of $0.13 per share. The SPP has not been underwritten and targets to garner up to $3 million. The company may accept additional applications subject to the demand of shareholder. If the offer gets oversubscribed, Echo Resources may in its absolute discretion, scale back the applications.

What To Expect From EAR Moving Forward: Echo Resources Limited is focused on enhancing its estimated returns of the Yandal Gold Project by making deployments in near term resource conversion, and focused exploration in order to further improve the production profile as well as extend mine life ahead of future production. The company is also focused on advancing the discussions with regards to regional asset and corporate consolidation. The exploration growth strategy has been designed in order to realise the additional value from 1,600km2 of contiguous and highly prospective tenements in the underexplored Yandal Greenstone Gold belt in Western Australia.

The company continued to progress the discussions related to the project funding during the quarter ended March 2019. Considering outcomes of the BFS and the final independent technical expert report, the non-binding indicative debt financing proposals are received from the range of resource lenders, which includes tier 1 Australian, and international institutions. The proposals range up to A$45 million and also have the potential to cover the entire pre-production capital. The company is assessing the proposals, and it also continues the discussions with the groups.

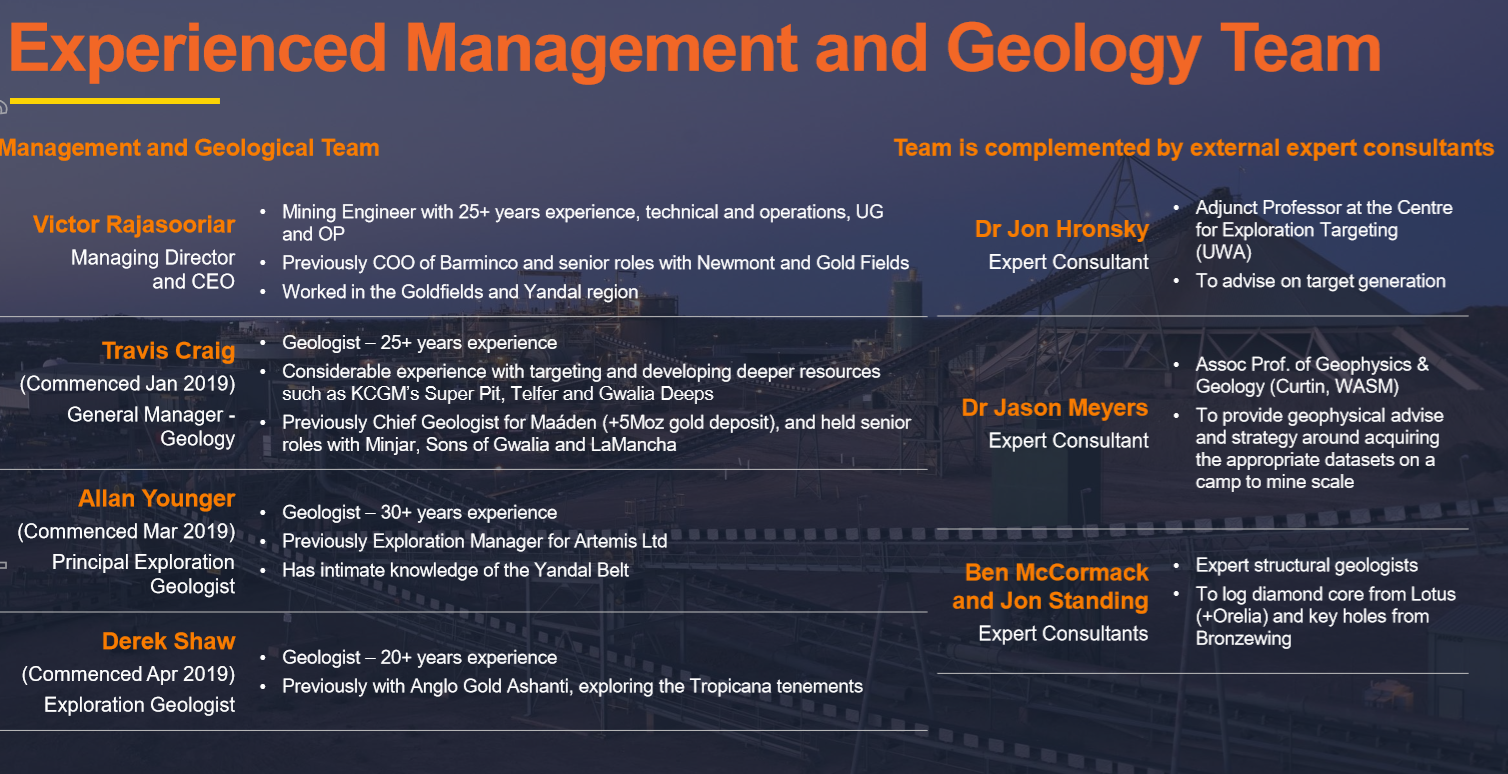

Strong Management and Team (Source: Company Reports)

Stock Recommendation: The management of Echo Resources Limited had stated that the decision to garner the additional capital reflects the company’s commitment to accelerate the exploration strategy at the Yandal Gold Project, which targets to unlock the further value from underexplored but very prospective tenement package. Assuming the entire take-up of placement, at the completion, Echo Resources would be having around 666.3 million shares on issue.

Also, the company’s key financial ratios have witnessed an improvement in FY 2018 on the YoY basis, which might attract the attention of market players. The company has lower Assets/Equity ratio in 1H FY 2019 as compared to the industry median, which implies lesser reliance on the debt when it comes to financing its assets. On the technical analysis front, recently the stock had fallen a lot from the upper levels of A$0.265 and now trading at A$0.135 as of 31st May 2019 (AEST 3:29 PM). After this selling pressure, the stock is consolidating in a range for quite a few days, which has halted the downtrend. This consolidation, after a downtrend indicates an accumulation zone, wherein investors might be interested and this may reverse the trend on the upside. Coming to the past performance, the stock has delivered the return of 23.47% in the span of the previous six months. However, in the time frame of previous three months and one month, it delivered the return of -34.15% and -6.90%, respectively and, thus, it can be said that the stock is quite volatile in nature. Given the backdrop of favourable Bankable Feasibility Study, growth strategy for its Yandal project, probable takeover scenario, and accelerated exploration program along with current trading level, we give a “Speculative Buy” rating on the stock at the current market price of A$0.140 per share (up 3.704% on 31 May 2019).

EAR Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...