Kalkine has a fully transformed New Avatar.

.PNG)

Australia is set to witness the new normal after COVID-19 restrictions are relaxed and the majority of the country reopens in July. Since the outbreak, the Australian government and other concerned authorities have been proactively involved in addressing the challenges occurring due to the COVID-19. With health being the topmost priority, the country was locked down like other countries in the world to mitigate the risk of contracting the deadly virus. Country-wide lockdown and social distancing measures meant a significant downturn for the economy as business activity came down massively. No single sector was left untouched by the adversities and has gone through a tough time due to interdependence.

As consumer spending decreased due to less movement of people, top-line of few businesses were severely impacted due to the significant fall in demand. Cost-cutting in the form of salary cuts, layoffs, deferred projects and capital expenditure came in as a part and parcel of the above as businesses aimed for survival through cash conservation. As a result, unemployment in the country also worsened as a large number of employees had to undergo job losses. However, the above challenges have been common to all the economies across the world, which have been hit by the novel coronavirus. What makes Australia stand out, is the approach it followed to deal with the virus, which makes it one amongst the few countries that have been successful in flattening the curve.

Three-Stage Plan to Lift Restrictions: Several states in Australia have started relaxing restrictions and have begun activities as per the Federal government’s three-stage plan for the same. The first stage in the government’s plan entails the opening of churches, libraries, cafes, restaurants, wherein gatherings of at most 10 people will be allowed at once. Households will be allowed to host 5 people, with allowance for local and regional travel. Stage two allows for gatherings of 20 people, with the added ease of reopening to gyms, cinemas, salon, community sport, etc. The final stage of the plan is expected to be implemented by July with workplaces opening and the number of people allowed per gathering rising to 100. Moreover, the government has also included inter-state travel as a relaxation in stage three..png)

Three-Stage Plan to Ease Restrictions (Source: Federal Government)

Several States Opening Up: Queensland has now allowed for the movement of people for shopping of non-essential items, visit parks, and traveling up to a certain distance for recreational purposes. The state is now operating as per the first stage of reopening defined by the government, where not more than 10 people can gather outside. Similarly, New South Wales has also relaxed movement as per stage one, with cafes, restaurants, libraries, etc., allowed to operate. Western Australia and Northern Territory have seen the most significant ease of restrictions, where most of the activities have already begun or are about to begin shortly. Other states that are reopening in strict compliance with the government’s directives, include South Australia, Australian Capital Territory, Tasmania, Victoria, etc.

With all the directives or restrictions in place, consumer behaviour across the country has been significantly affected by increased reluctance to physical purchases. Since the outbreak, online purchasing has taken a dominant position in comparison to store-based purchasing. Large retailers across the country witnessed a surge in online sales, which helped in balancing the adverse effects of a significant decline in stores’ sales. As stores remained closed, the sector saw increased spending on online infrastructure to keep up with the recent trend and avoid disruptions in serving customers.

Retail Sales Decline in April: As per the Australian Bureau of Statistics, retail sales for the month of April declined by 17.9% over the previous month as compared to a rise of 8.5% in March, driven by the food retailing industry, which fell 17.1% in April, following a 24.1% rise in March 2020. Moreover, 10% of the total retail turnover in April was generated from the online channel. Reportedly, it was largely the impact of regulations with respect to limited movement on account of social distancing measures. While the numbers collapsed in the month of April after consumers slowed down on panic purchasing, the three-stage plan comes to the rescue from the plight of a further slump in sales.

After the government announced the three-step plan for easing restrictions, the country has begun to adapt to the new normal with limited movement. Permission with respect to the opening of several businesses, movement of people, regional travel, etc., may not bring instant relief to the fractured economy but will surely mark the beginning of recovery in an organized manner. Australia’s success in flattening the curve as compared to other countries is attributable to the cohesive efforts of all the sections of the society. Retailers across the country strictly responded to the government regulations by closing all or majority of the stores across the network. Some of the players in the segment continued to function with well-established online infrastructure and witnessed robust sales growth across the online platform.

In recent weeks, several companies have started opening stores across their network and are set to be fully operational for physical purchases by or before the end of June. As conditions begin to stabilize and more people move out of their houses, we can expect optimistic results for the retail segment on the store front. What lies ahead in terms of financial gains, remain entirely a factor of consumer behavior. Considering the recent shift to online purchasing, one cannot predict where the next wave of consumer purchasing behavior will be directed to. Therefore, the companies with significant digital capabilities and sufficient financial flexibility to invest in online infrastructure are expected to be the beneficiaries of this change in the current environment. Moreover, there remains a chance of further boost in sales from in-store purchasing as the situation normalizes. In light of the above factors, let us have a look at few stocks that have demonstrated strength in the current challenging period and have provided a decent outlook for further growth.

1. Premier Investments Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 2.46 Billion, Annual Dividend Yield: 4.57%)

Surge in Online Sales: Premier Investments Limited (ASX: PMV) operates numerous specialty retail fashion chains in Australia, New Zealand, Asia, and Europe. The company recently updated that due to the temporary closure of all its stores in late March, Premier Retail’s global sales were adversely impacted, with total sales down 74% for the 6 weeks period to 6th May 2020. However, the company saw a surge of 99% in online sales after social distancing norms were introduced. The company’s largest Australian brand, Peter Alexander, witnessed a surge of 295% in online sales during this period. Premier has made major investments in online technology, people and marketing initiatives over the past 10 years, in order to deliver seamless customer experience.

Outlook: To secure the long-term future of its stakeholders, the company has acted prudently by making some tough decisions in the current operating environment. It has put all capital and operating expenditure on hold, stood down 9k employees, and has maximized all available government subsidies across various jurisdictions it operates in. As at May 2020, the company had a cash balance amounting to $256.2 million, with an access to $91.8 million of undrawn facilities. The company bases its confidence upon its long-standing successful strategies that provide a shield against all the challenges of the global health and economic crisis.

In a recent update on COVID-19, the company notified about the re-opening of its stores in New South Wales, Victoria, Western Australia, South Australia, Australian Capital Territory and Tasmania, from 15th May 2020. The company has in place the necessary safety checks to ensure proper adherence to the guidelines issued by the government. Stores in New Zealand have also reopened from 14th May 2020, with all health and safety measures in place..png)

Bankruptcy and DuPont Analysis:.png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs PMV (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained positive returns of 20.31% in the last one month and is currently trading slightly above the average of its 52-week trading range of $8.130 - $21.560. After a slump in the stock price due to COVID-19 led market volatility, the stock has demonstrated the strength of the business through a quick bounce. Price began to stabilize soon after the reaction to market volatility and stands resilient with the continued success of the business, despite external challenges. Premier Investments’ decent liquidity position provides it sufficient financial flexibility to begin the recovery as stores reopen across multiple locations. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Buy” recommendation on the stock at the current market price of $15.83, up 1.997% on 25th May 2020.

2. Myer Holdings Limited (Recommendation: Speculative Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 238.17 Million, Annual Dividend Yield: NA)

Recovery to Begin as Stores Reopen: Myer Holdings Limited (ASX: MYR) operates in the departmental stores segment and has a portfolio of 66 stores across Australia. During the 26 weeks period ended 25th January 2020, the company reported total sales amounting to $1,607.9 million, down 3.8% on pcp. Online sales stood at $168.2 million, up 25.2% on the prior corresponding period. The company continued to practice disciplined management of costs and cash, with a view to strengthening its balance sheet. During the period, it witnessed a reduction in costs, by further simplifying the business through improved processes.

Outlook: The company has been continuously engaged in managing the supply chain impact of Coronavirus and is focused on mitigating the delays to the planned delivery of merchandise. The company expects the current challenges to remain through the second half, with the impact on store traffic being uncertain. However, it has a clear plan to address the adversities and has numerous opportunities to improve productivity and further reduce costs.

In a recent update, the company notified that it has reopened 24 stores over the recent weeks on a stage and trial basis, along with a strong performance reported across the online platform. The company also updated that it will be reopening all its remaining stores from 27th May 2020, excluding Karrinyup (WA), which is expected to begin operations on 30th May 2020 after the completion of refurbishment works. The stores will operate with increased frequency of cleaning, protective items such as hand sanitiser stations, social distancing and contactless payments..png)

Bankruptcy and DuPont Analysis:.png)

Valuation Methodology: P/E Multiple Based Relative Valuation (Illustrative).png)

P/E Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs MYR (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gave negative returns of 22.67% in the last three months and is currently trading below the average of its 52-week trading range of $0.083 - $0.7. The stock of the company did react negatively due to the economic fallout but has shown decent recovery on April month onwards. Although there have been multiple challenges pressurizing the stock price lately, the company has maintained its position in the market through the digital channel. Moreover, as stores across the platform reopen and sales begin to gain momentum, the company will be in a better position to achieve long term growth. We have valued the stock using Price to Earnings multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.285, down 1.724% on 25th May 2020.

3. Accent Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 639.76 Million, Annual Dividend Yield: 7.63%)

Exponential Growth in Online Sales: Accent Group Limited (ASX: AX1) is engaged in the retail and distribution of branded performance and lifestyle footwear across Australia and New Zealand. During the half year ended 29th December 2019, the company reported EBITDA growth of 10.5% to $67.7 million. NPAT grew by 9.7% to $35.29 million. FY20 interim dividend amounted to 5.25 cents per share, up 16.7% on pcp. In the last 2 weeks of April, digital sales have grown from an average of approximately $250,000 per day to between $800,000 and $1.1 million per day, reflecting continued investment and further energised focus on digital.

Outlook: The company is committed to maintaining its position as the largest multi-channel retailer in the market. It enjoys a competitive advantage on the back of its superior digital capabilities and store performance. The company has received immense support from major suppliers and global brand partners to ensure that its inventory pipeline is right-sized and payment terms are aligned to reflect the current sales environment. In the future, the company expects online sales to represent a much larger portion of total sales due to a shift in consumer habits in Australia and New Zealand.

In a recent business update, the company notified about the reopening of stores on 11th May 2020, with new safety protocols. The above decision came on the back of increased demand for active footwear and apparel and the Sketchers range for health professionals. Moreover, with the recent spike in online sales, the company is re-evaluating the location, size and format of its store network to ensure the appropriate balance between digital and store sales..png)

Bankruptcy and DuPont Analysis:.png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative).png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs AX1 (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gave negative returns of 36.90% in the last three months and is currently trading below the average of its 52-week trading range of $0.555 - $2.2. With the massive surge in digital sales, the company has proved its capabilities to survive the unprecedented challenges, while maintaining a stable market position. After a decline in stock price caused by market shockwaves, the price slowly began to recover and reached a stable ground. Going forward, the company’s added sales from its store network and the benefits from large online demand will act as key catalysts for top-line growth as well as price movements. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.245, up 5.508% on 25th May 2020.

4. Adairs Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 292.5 Million, Annual Dividend Yield: 8.67%)

All Stores to Reopen by June End: Adairs Limited (ASX: ADH) is engaged in the retailing of homewares and home furnishings in Australia and New Zealand, via retail stores and online channels. Recently, the company released an update notifying that its online sales have exceeded expectations since stores closed, with sales rising by 221% during the period. The company’s online sales for the 9 months to March 2020 represented approximately 20% of the total sales. The company received strong support from its key product suppliers, with proper inventory management in place to align with an expected softer retail environment in the recovery phase. During the first half ended December 2019, the company reported sales amounting to $178.9 million, up 8.6% on the prior corresponding half, with store and online sales rising by 4.9% and 31.6%, respectively.

Outlook: During the first half, growth was delivered by strong execution of its digital strategy and an omni channel approach, particularly across expansion categories. With the outbreak of COVID-19, these established capabilities helped the company survive a tough period of fall in stores sales due to social distancing measures issued by the government.

In the recent business update, the company also informed that it has considered reopening its stores from 7th May 2020, with the initial focus being on larger format stores, primarily Homemaker stores. Stores across the platform will continue to open throughout May and June, with regard to relevant government directions.

.png)

Bankruptcy and DuPont Analysis:.png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs ADH (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gave positive returns of 51.75% in the last one month and is currently trading above the average of its 52-week trading range of $0.440 - $2.740. The company has a strong balance sheet and liquidity position and does not need any additional capital currently. The company’s online sales exceeded expectations while physical sales were remained NIL in Australia and New Zealand. Online performance will now be complemented by added sales, after the stores reopen. The stock price was impacted by a spike in market volatility during March and has been on a recovery since then. It has shown stable movements recently in response to a relative improvement in market volatility. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Hence, we give a “Hold” recommendation on the stock at the current market price of $1.775, up 2.601% on 25th May 2020.

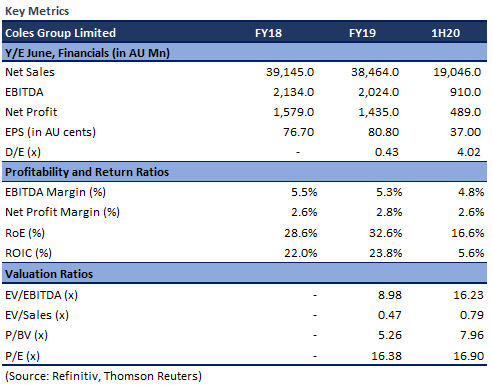

5. Coles Group Limited (Recommendation: Hold, Potential Upside: High Single-Digit)

(M-cap: A$ 20.08 Billion, Annual Dividend Yield: NA)

Sales Up in the March Quarter: Coles Group Limited (ASX: COL) distributes food, groceries, fuel, liquor, etc., through a network of stores and online channel. During the 12 weeks period from 6th January 2020 to 29th March 2020, the group reported sales revenue amounting to $9.2 billion, up 12.9% on pcp. The group witnessed strong performance across supermarkets in January and February, with comparable sales growth of 13.1% and the 50th consecutive quarter of comparable sales growth. The company continued to help the community during the unprecedented challenges put forward by COVID-19 and hired over 12,000 casual team members to serve more customers and expanded its distribution centres to increase capacity.

Outlook: During the fourth quarter, the company expects an elevated cost base due to additional investment in relation to COVID-19. These costs would include higher remuneration costs for new hires, investment in cleaning, security and queuing systems, team member discounts to reward their support during COVID-19, grocery donations, etc. Liquor sales are expected to increase till restaurants, pubs, clubs, etc, continue to operate as per government directives.

Although the retail sector suffered a loss in sales and demand due to coronavirus outbreak, Coles Group continued to deliver growth in sales with the diverse range of products it deals in. The group witnessed unprecedented demand and worked closely with suppliers and supply chain partners to ensure timely delivery of stock. In the March quarter, the company’s convenience store sales revenue increased by 5% on the prior corresponding period due to bulk purchase of non-food categories such as toilet paper and cleaning products. Liquor sales also increased by 6.1% on the prior corresponding period, with sales growth from exclusive Liquor Brands increased by 10%.

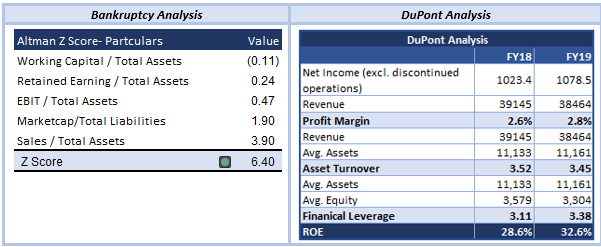

Bankruptcy and DuPont Analysis:

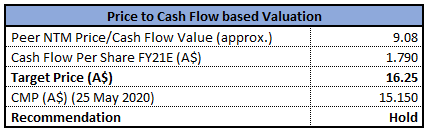

Valuation Methodology: P/CF Multiple Based Relative Valuation (Illustrative)

P/CF Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

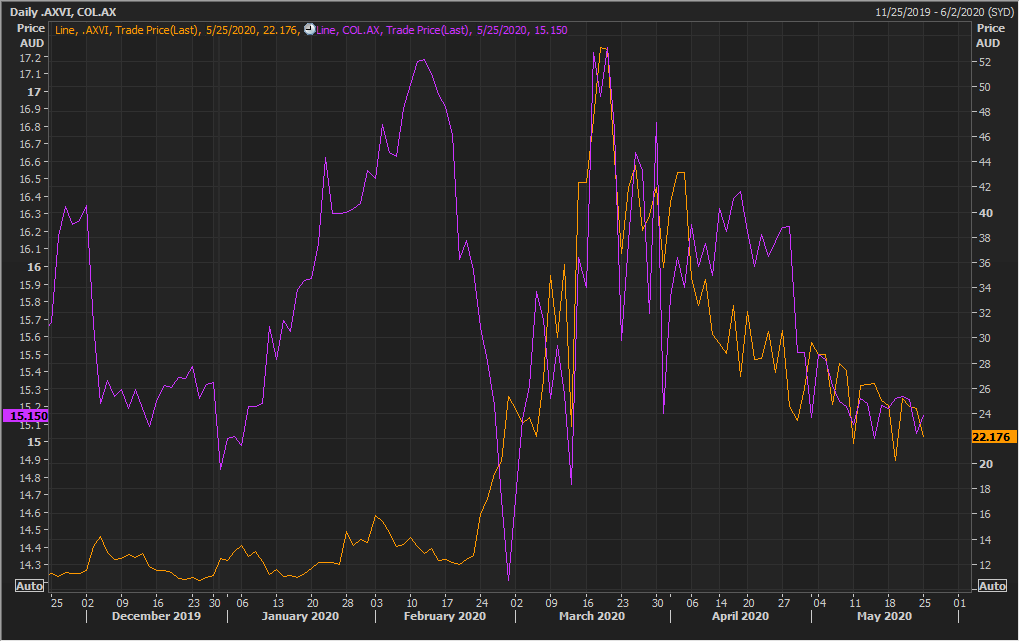

A-VIX vs COL (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained positive returns of 17.39% in the last one year and is currently trading close to the average of its 52-week trading range of $12.216 - $18.090. Unlike other retailers, Coles Group’s stock price reacted positively to a spike in market volatility during March, as demand for its products in the essential service category continued to rise. As consumers began to hoard daily necessities to avoid future shortages, the movement in the stock price was seen overlapping the market volatility, as depicted in the above chart. Till uncertainty looms over the anticipated impact of COVID-19 on the business, the group is continuously reviewing operational and strategic learnings and opportunities that will help in accelerating the delivery of its long-term plan. We have valued the stock using a P/CF multiple based illustrative relative valuation method and arrived at a target price with a high single-digit upside (in percentage terms). Hence, we give a “Hold” recommendation on the stock at the current market price of $15.15, up 0.664% on 25th May 2020.

.PNG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Note:

Altman’s Z-Score Model:

(1) When Z-Score<1.81 then it is in Distress Zone

(2) When Z-Score is between 1.81 and 2.99 then it is in Grey Zone

(3) When Z-Score > 2.99 then it is in Safe Zone

The above relative valuation implies a target price incorporating the key positive factors driving the business and indicate long term potential of the stock. Prices, however, remain subject to any short-term movements due to the impact of coronavirus on the business fundamentals.

All the recommendations and the calculations are based on the closing price of 25 May 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...