Company Overview - Drillsearch Energy Limited (Drillsearch) is an Australia-based oil and gas explorer and producer focused on the Cooper-Eromanga Basin. The Company operates business through three segments: Oil Projects, Wet Gas Projects and Unconventional Projects. Drillsearch is exploring and developing oil projects in the Cooper Basin, targeting numerous, high-return oil exploration projects to drive short-term growth. Wet gas is natural gas that contains significant amounts of liquid hydrocarbons - condensate (a light oil) and LPG. The Company is focusing its exploration activities on two key project areas; the Central Cooper Basin - Nappamerri Trough Shale Gas Fairway, and in the Southern and Western Cooper Basin Unconventional Gas Fairway. The Company holds 18 permits and six tenements with a net permit interest of 15,000 square kilometers. Drillsearch holds at least a 50% interest in 17 of these 24 areas and operates 14 permits.

Analysis - Drillsearch Energy Limited (DLS) recently announced the discovery of a new wet gas on the Western Cooper Wet Gas Fairway of the Cooper Basin, which is the fourth discovery, out of the five wells drilled by the company through its joint venture with Santos (STO).

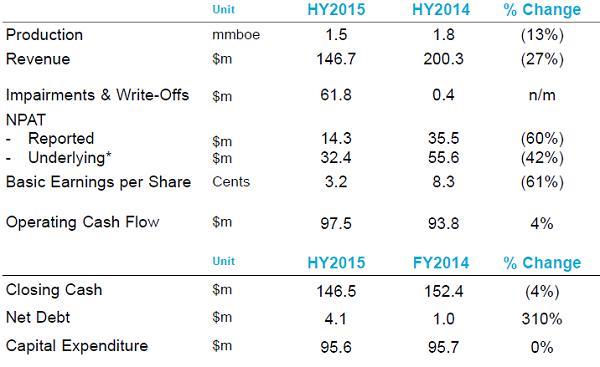

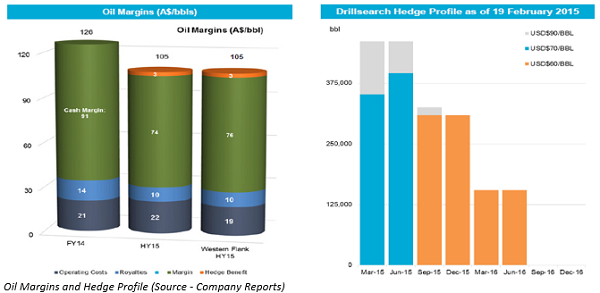

The company’s financial results for 1HFY15 were impacted by the plunging oil and gas prices, and DLS thus reported a year-on-year revenue decline of 27% to $146.7 million. For the same period, the average realized oil price (including hedge gains) decreased to $105.40/bbl, as compared to $126.30/bbl for the corresponding period last year. Although new production started in the company’s Western Flank Oil Fairway, total production in 1HFY15 fell 13% to 1.54mmboe. The company’s outlook of lower oil prices led to over $61.8 million of non-cash exploration write-offs and asset impairment, especially for the company’s interests in producing Eastern Margin/Tintaburra assets. Hence, the net profit after tax witnessed a year-on-year decline of over 60% for 1HFY15 to $14.3 million.

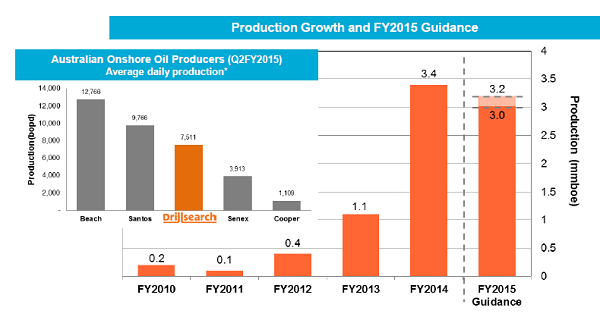

Production Growth and FY15 Guidance (Source - Company Reports)

As at 31 December 2014, the company’s net assets rose to $417.4 million, as compared to $363.4 million in June 2014, mainly due to the acquisition of Ambassador Oil & Gas Limited. The company acquired a 47.5% stake in PEL570, through this transaction. Capital expenditure for the same period stood at $95.6 million. As at 31 December 2014, the company holds strong liquidity position of $196.5 million, which includes undrawn $50 million working capital facility. Operating Cash Flow increased by 4% to $97.5million during 1HFY15, as compared to the same period of FY14.

DLS has solid projects like western flank of the copper basin and a strong track record of exploration success. The company’s relatively small gas business has also demonstrated succesull discoveries with a high content of natural gas liquids like propane, condensate and butane. There are enough funds to increase the gas business, while the oil business is mainly dependent on the drilling success.

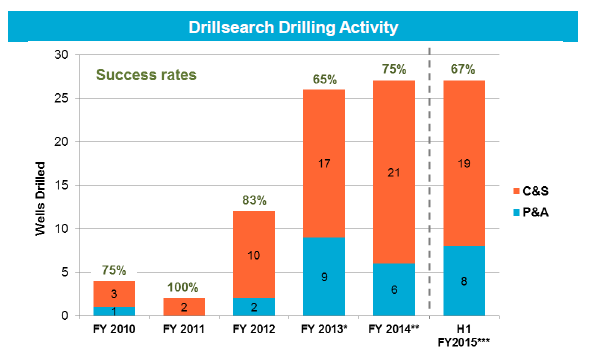

For 1HFY15, Western Flank oil production contributed 11,294 bopd, as compared to the 12,748 bopd for the same period in the previous fiscal year. In the same period, the company reported 16 successfully cased and suspended Oil and Gas wells, with two new Western Flank oil discoveries and three new Wet Gas discoveries.

During 1HFY15, the drilling program reported the 14th and 15th oil discoveries, on Western Flank Oil Fairway (formerly PEL 91) at Balgowan-1 (PRL 171) and Burners-1 (PRL 172). Moreover, six Bauer development wells, with the Hanson-2 appraisal well (PPL 255) were also cased and suspended as future oil producers. The pad drilling techniques were used for the development wells of Bauer-16 to -19, which were drilled as deviated wells from a single pad location in the central part of the Bauer oil field. In February 2015, Stanleys-1 exploration well at PEL 91 (PRL 171) area, was cased and suspended as 16th oil discovery.

Performance Summary (Source - Company Reports)

The Stanleys-1 exploration well successfully recovered oil from a seven metre gross oil bearing interval in the Birkhead Formation. Based on March updates, DLS also reported drilling of Bauer-20 to -23 development wells from a single pad location. This did not require any rig demobilization and the four wells were drilled, cased and suspended within 36 days. These ought to be connected as future Namur/McKinlay production wells. The Bauer 23 development well was found to be intersecting the Namur Sandstone reservoir 3m high to prognosis, which is a good sign for enhancing reserves.

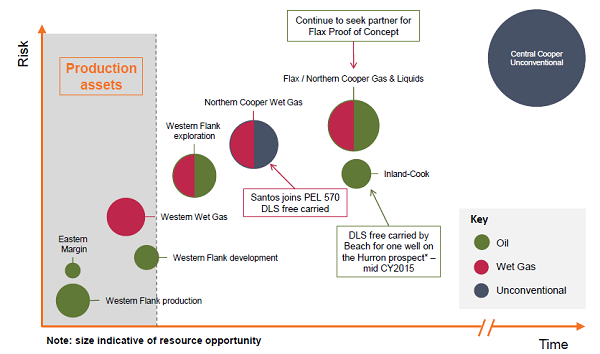

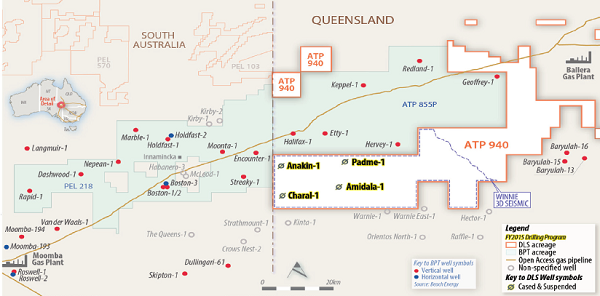

Quality Growth Assets across the Portfolio (Source - Company Reports)

As indicated above, the Western Cooper Wet Gas joint venture with Santos (DLS 40%, STO 60% and Operator) reported a new wet gas discovery at Kyanite-1 in March 2015, on the Western Cooper Wet Gas Fairway of the Cooper Basin. The Kyanite-1 exploration well in PEL 513 was drilled for a total depth of 3,354 metres, which demonstrated good gas shows through the Patchawarra and Tirrawarra Sandstone/Merrimelia Formations, as well as identified stacked reservoirs. After the completion of Kyanite-1, the sixth well, Spinel- 1 was drilled to a total depth of 3,282 metres in April, and is cased and suspended as a future gas producer. Nulla North-1 well in the PRL 133 area was cased and suspended as a new discovery during February 2015. For the Beach Energy joint venture, four wells were drilled in the PEL 106 area. PPL 257, the Maupertuis-1 wet gas well, showed good hydrocarbons in Tirrawarra Formation, and is elected for future evaluation.

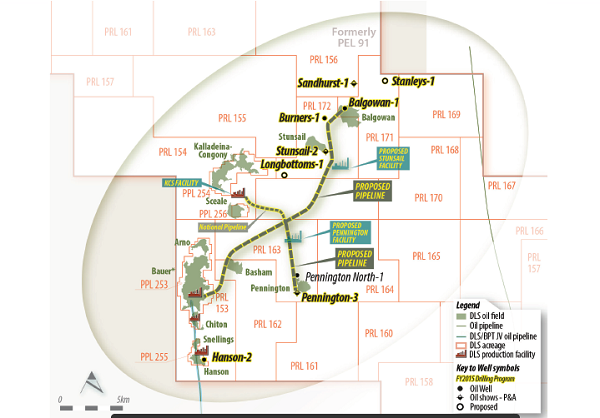

Western Flank Oil Ongoing Connections Program (Source - Company Reports)

With regards to the Northern CooperOil Fairway, PEL 103, the Banyan-1 vertical exploration well was drilled during 1HFY15, with petro-physical evaluation showing the well to be non-commercial, due to which it was plugged and abandoned. The drill in the Juniper-3 vertical went well in PRL 17, showed pay intervals in the lower Patchawarra Formation, and was cased and suspended for future testing and hydraulic stimulation. The Flax production facility in PRL 14 completed the recertification during the period, and reported an initial production rate of over 190 bopd. The Flax-3 production was 1,109 bbls for 1HFY15. PEL 182 finished the production testing of the Vanessa-1 exploration well, wherein the gas flowed to the surface at an average rate of 5.0 million standard cubic feet per day (mmscf/d) from the Epsilon and Toolachee Formations on a 65% choke (42/64”). Moreover, condensate was reported to be produced at a rate of 15 barrels per mmscf/d.

Northern Cooper Wet Gas Vanessa and PEL 101 (Source - Company Reports)

For the unconventional business, the second and third of the deep wells from the ATP 940 (DLS 40%, QGC, 60%) were completed during 1HFY14. The company also started the hydraulic simulation and testing of 2 wells in ATP 940, with Charal-1 tests recording peak flow rate of 0.95 mmscf/d, while Anakin-1 testing will be started soon.

Unconventional Joint Venture with QGC (Source - Company Reports)

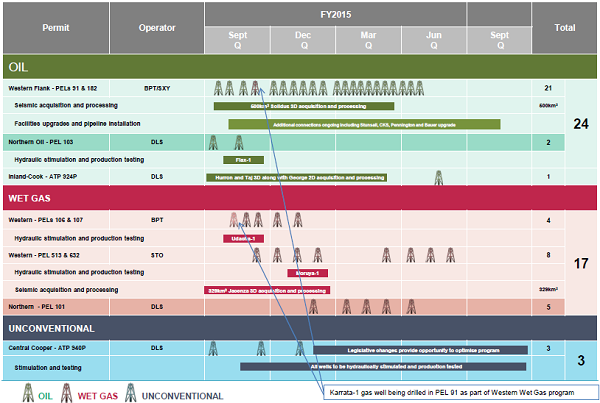

For the entire FY15, the company targets to drill five wells in the Northern Cooper Wet Gas project area (PEL 101). The management expects to drill a total of 24 for its oil business and 17 for the wet gas business, for the year.

FY2015 Activity (Source - Company Reports)

DLS reportedly increased its capital expenditure from $8.9 million in FY10 to $143.4 million in FY13, which is mainly used to fund the oil business. However, with the lowering oil prices, the company cut its capital expenditure spending to $95.7 million in FY14. But, DLS has now increased its capital expenditure for FY15, and spent $95.7 million for 1HFY15. The Company has slashed the capital spending guidance for the entire FY15 to $150-$165 million from over earlier guidance of over $170 million, and plans to use these $10-$15 million savings for corporate and operating costs.

Drilling Activity (Source - Company Reports)

DLS is almost debt free, in spite of having a convertible note of $153.4 million as at 30 June 2014 and has over $146.5 million in cash as at end of 1HFY15. Even though the oil prices are declining, the company manages to have profitable operations given the fact that it is paid in US dollars for crude oil production while cost is incurred in Australian dollars. Thus, the US dollar decline is being partly offset by the decrease in the Australian/US dollar exchange rate to as low as A$0.82 per US dollar, which witnessed greater than 10% decline during the period as compared to FY14. Although the cash margins decreased on the back of lowering oil prices during 1HFY15, DLS’ hedging activities have partially offset the decline. The company has hedged for over 927,000 barrels of production for floor prices in the range of $60-$90 a barrel, for the year 2015-16. Over $3.5 million pre-tax benefit was reported during 1HFY15. Moreover, DLS accumulated put options at $90/bbl for a volume of 80kbbl in February 2015.

Overall DLS’ efforts to maintain solid cash position, hedging activities to offset the impact of lowering oil prices and huge asset base makes it an attractive investment target at this juncture. Potential is also seen with regards to gas development opportunity in the Eastern Australian markets given the gas reserves. Of course, commercial production from the discovered wells is something to be eyed on.

DLS chart (Source - Thomson Reuters)

Accordingly, we give a BUY recommendation for the stock at the current price of $1.175.

Disclaimer The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...