Company Overview - Drillsearch Energy Limited (Drillsearch) is engaged in exploration, development and production of oil and gas interests. Drillsearch operates in three segments: Oil; Wet Gas, and Unconventional. Drillsearch Energy Limited (DLS), one of the largest acreage holders in the Cooper basin region of central Australia, recently announced for successful completion of compulsory acquisition of the outstanding shares in Ambassador Oil & Gas Limited (Ambassador). Ambassador would thus become a wholly-owned subsidiary of Drillsearch. As per the Company, this step has consolidated DLS’ position in the Northern Cooper and will provide further diversification of DLS’ Unconventional Business outside of the Nappamerri Trough and into the Patchawarra Trough adjacent to its existing PEL 101 acreage.

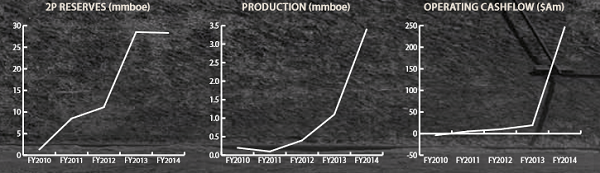

Analysis - The Company confirmed that its oil business steered the increase in production and cash flow in FY2014. Total oil and gas production was of 3.4 million barrels of oil equivalent (mmboe). This exceeded the guidance of 3.0 to 3.3 mmboe. Further, $387 million in revenue generated $71.5 million in net profit after tax. As at 30 June 2014, cash on balance sheet was about $152 million.

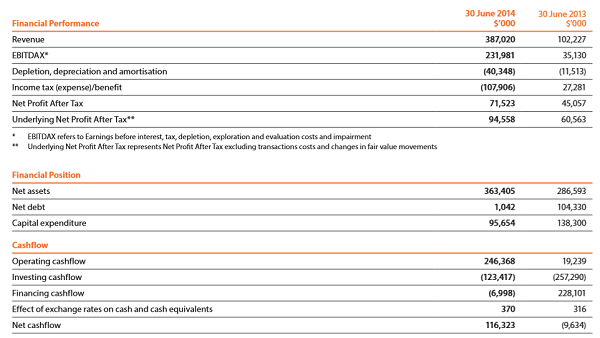

Financial Summary (Source – Company Reports)

In addition, the Company could proceed with successful replacement of 2P oil reserves after record production. The Company also entered into a joint venture with Santos in PELs 513 and 632 in view of fast-tracking plans for wet gas commercialization. It further announced for drilling two of its deepest wells at around 4,000 metres under unconventional project in joint venture with QGC. The deep-well drilling will be achieved using high resolution 3D seismic and the most fit-for-purpose rig in Australia. Further, this project is the biggest one undertaken by Drillsearch as an operator.

2P Reserves, Production and Operating Cashflow (Source – Company Reports)

The Company’s long term debt was $153.43 million and total liabilities were $319.43 million, as of June 2014. The Company witnessed higher operating costs, royalties and depletion, depreciation and amortization (DDA) than in the previous year, due to increased production. DLS did not pay any dividends during the last 12 months. The Company has invested immensely in the exploration and development activities across its acreage position. Further, DLS announced for a three-year $50 million working capital facility in 2013, which is undrawn as at 30 June 2014. This provides DLS to have a strong total liquidity position of $202.4 million at financial year-end.

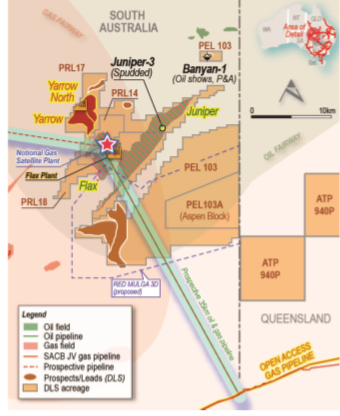

The latest September 2014 Drilling Report by DLS gives more clarity on DLS’ operational aspects. Specifically, the Company highlighted that Western Flank and Northern Cooper campaigns; and Padme-1 drilling are continuing. The schedule with regards to the hydraulic stimulation in ATP 940P is appearing to be on track with Charal-1. Juniper-3 well is underway in Northern Cooper Gas and Liquids Project Area.

Two oil appraisal wells have been drilled in PEL 91 on the Western Flank Oil Fairway during the month. The Stunsail-2 well was although drilled, the same was plugged and abandoned due to uneconomic volumes and flow rates. The results for the Pennington-3 well which was spudded on 20 September are to be published in drilling report of the subsequent month. The rig will then be used to drill the Bauer-14 and -15 development wells in PEL 91. Peak production rates from PEL 91 overdid 13,500 barrels of oil per day.

Image (Source – Company Reports)

With regards to the Northern Cooper Gas and Liquids Project Area, the work-over of the Flax-1 well is continuing in PRL 14 for hydraulically stimulating a zone in the Mid-Patchawarra Formation alongside recompletion as a dual-zone producer. Recompletion of Tirrawarra Formation is also to be progressed. The Banyan-1 vertical exploration well was spudded on 27 August in PEL 103. This witnessed multiple oil shows from the Birkhead and Tinchoo Formations. However, the same was plugged and abandoned due to no potential pay intervals. Juniper-3 appraisal well was drilled post the completion of Banyan-1.

Under the Wet Gas Business, drilling was done for the Karrata-1 exploration well within the PEL 91 permit on the Western Wet Gas Fairway. This well witnessed great gas shows in coals and sands throughout the Patchawarra Formation. Nonetheless, potential gas pay intervals were found to be insufficient and thus the well was plugged and abandoned. Regardless of of the above, Wet Gas production from the Western Cooper project area was 0.47 mmboe, which is an increase of 62% increase over FY2013 production of 0.29 mmboe.

Image (Source – Company Reports)

Image (Source – Company Reports)

DLS’ total revenue was also supported by enhanced condensate production from the liquids-rich Canunda field.

The Padme-1 well was re-entered under the Central Unconventional Fairway ATP 940P. Further, production testing of Charal-1 will begin in early November.

In July 2014, DLS also announced for execution of an agreement with Beach Energy Limited for Beach to farm into its ATP 924P oil and gas exploration permit in the south west Queensland section of the Cooper Basin. Beach will fund 150km

2 of recently acquired 3D seismic and drill an exploration well on the Hurron Prospect.

DLS’ overall drilling success rate has gone up to 75% from 27 wells drilled. With more than 40 wells planned, FY2015 is set to bring new avenues. As per DLS, production guidance for FY2015 is given to be 3.0 to 3.4 mmboe with healthy production in PEL 91. Capex guidance is set to be as $130m to $170m.

5 Year Roadmap (Source – Company Reports)

5 Year Roadmap (Source – Company Reports)

DLS believes that its major developments were with regards to the Stunsail and the Balgowan-1. Further, the Eastern Margin joint venture with Santos is another producing asset, which may emerge as a long term driver of stable production. As per the Company, a big addition in 2P contingent resources will entail the work around the Flax field. This correlates to an exceptional use of horizontal wells in the Flax accumulation.

The Company is certain of the fact that it has shown a big improvement in profitability and cash position, and is exceptionally well-funded up to FY 2016. A recent announcement on the Annual General Meeting to be held on 19 November 2014 is being considered, as this would unearth more opportunistic areas for DLS.

Of course, we will have to be wary of the potential risks that may entail oil and gas price changes, fluctuations in exchange rates, operational risks, environmental and regulatory risks, geological risks impacting reserves and productivity, and engineering/technical risk associated with well positioning.

Nonetheless, the possibility of oil pricing gradually springing back may provide some leeway for DLS.

DLS Daily Chart (Source - Thomson Reuters)

Overall, DLS’ efforts with regards to its oil business success, drilling activities which may pay off over the long term, strong balance sheet, FY15 work programme and strategic approaches to emerge as a leader do indicate a good play. Reserves upgrade, widespread drilling programme in Cooper Basin assets, Cooper-Eromanga basin play, and unconventional play with QGC speak for DLS future.

Accordingly, we put a

BUY recommendation for the stock at the current price of $1.175.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...