Kalkine has a fully transformed New Avatar.

Company Overview: Downer EDI Limited provides services to customers in markets, including transport services, technology and communications services, utility services, rail, mining, and engineering, construction and maintenance. The Company's segments include Transport Services, which includes its road, rail infrastructure, bridge, airport and port businesses, and provides a range of transport infrastructure services, such as maintenance and earth works; Technology and Communications Services, including services, such as civil construction, network construction, commissioning and testing; Utility Services, including water lifecycle solutions for municipal and industrial water users and sugar cane waste fired cogeneration plants; Rail, including rail asset solutions, such as passenger and freight build; Engineering, Construction and Maintenance, which includes services, such as engineering design and civil works for projects, and Mining, including blasting services and exploration drilling services.

.png)

DOW Details

Decent Performance in 1H FY19: Downer EDI Limited (ASX: DOW) happens to be a leading provider of the integrated services in Australia and New Zealand. As on June 17, 2019, the market capitalisation of Downer stood at ~$4.16 billion. The company reported its results for the half-year ended December 2018 in which it witnessed increases in the total revenue, earnings before interest, tax and amortisation of acquired intangibles assets (or EBITA) and NPAT. The company’s total revenue witnessed a rise of $522.5 million or 8.6% and stood at $6.6 billion. Downer’s transport revenue witnessed a rise of 0.8% or $16.2 million and stood at $2.1 billion despite revenue lost after the divestment of the freight rail business in the prior corresponding period. The company’s utilities revenue rose 27.5% and stood at $1.2 billion because of continuing strong contributions from nbnTM contracts in Australia and new renewable energy projects.

.png)

Downer’s Financial Results (Source: Company Reports)

The company’s EC&M revenue witnessed a rise of 34.1% and stood at $945.1 million because of increased activities on the Ichthys project in Northern Territory and six-month contribution from MHPS following the acquisition. Downer’s mining revenue rose 3.6% and stood at $714.2 million, primarily because of increased activities at Blackwater and Carrapateena as well as a contribution from the new contracts, although this got partially offset by the completion of the Boggabri contract in 1H FY 2018.

The company’s strategy focuses on zero harm, driving improvement in the existing businesses as well as operations, deploying towards targeted growth opportunities, and creating new positions in the appropriate markets. The company is focused towards the projects and customers which would be helping in driving the long-term service revenue and this might act as a tailwind moving forward. Downer had stated that the exposure towards the high-risk market is being actively limited by the risk management processes focusing towards quantum, type of project as well as contract form.

Top 10 Shareholders: The following chart provides a broader picture of the shareholding pattern of Downer EDI Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

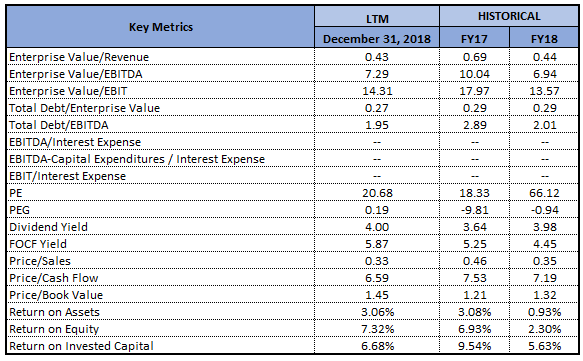

Decent Footing from Margins’ Standpoint: Downer EDI Limited is having decent standing with respect to its key margins position in 1H FY19. The company’s net margin stood at 2.2%, which implies a rise of 2.5% on the YoY basis, showing its improved capability to convert the top line into the bottom line. Its gross margin stood at 47% in 1H FY 2019 that reflects a rise of 1.6% on the YoY basis.

.png)

Key Metrics (Source: Thomson Reuters)

The company’s Debt/Equity ratio stood at 0.53x, which reflects a fall of 0.9% on the YoY basis and, thus, it looks like that the company has been deleveraging its balance sheet. A lesser debt on the company’s balance sheet is generally considered to be positive largely because it indicates that the company has a lesser obligation to meet moving forward.

Robust Operating Cash Flow: Downer’s statutory EBITA witnessed a rise of 20.6% in 1H FY 2019 and stood at $268.0 million as compared to the underlying EBITA amounting to $222.3 million in pcp. The increase was primarily due to mining, utilities, transport and facilities, and was partially offset by the lower contribution from Engineering, Construction and Maintenance (EC&M). The company’s NPATA witnessed a rise of 23.8% and stood at $163.4 million. The funding, liquidity as well as capital are managed at group level and the divisions are focused towards working capital and operating cash flow management. In 1H FY 2019, the company’s operating cash flow was robust and stood at $355.3 million, which reflects a rise of 15.7% on pcp basis.

Dividend Rate on ROADS Preference Shares: Downer EDI Limited and Works Finance (NZ) Limited have advised that in accordance with terms of the ROADS preference shares, the dividend rate on ROADS preference shares for period 15 June 2019 to next reset date of 15 June 2020, happens to be 5.49% per annum, which is payable quarterly in arrears. The figure equates to One Year Swap Rate on 17 June 2019 of 1.44% per annum plus the Step-up Margin of 4.05% per annum.

Key Takeaways From Downer Group Site Tour: Downer EDI Limited recently released its Downer Group site tour presentation in which it threw light on road services business. Downer’s road services business gives strong, vertically integrated supply chain to the customers. Its customers include state and local governments, waste businesses, miners, airports as well as toll and other road owners. However, infrastructure investment, population growth, environmental sustainability focus and smart city technology are expected to act as tailwinds moving forward.

The following picture provides more details with respect to the vertically integrated multi-brand strategy:

.png)

Vertically Integrated Multi-brand Strategy (Source: Company Reports)

Contract for Stage One of The Murra Warra Wind Farm: In the month of December 2017, Downer and its partner Senvion GmbH, which is a leading global manufacturer of wind turbines based in Germany, had entered into a contract for Stage One of the Murra Warra Wind Farm near Horsham in Western Victoria. The stage One of the Murra Warra Wind Farm involves electrical, procurement and construction work, which includes installation of 61 wind turbines.

Under the contract, Senvion is responsible for manufacture, transport, erection as well as commissioning of turbines. However, Downer is responsible for the balance of plant works. It was stated that Stage One had been valued at around $380 million, and the share of Downer is around $100 million. The construction as well as delivery of stage one of the Murra Warra Wind Farm happens to be at an advanced stage and around 95% of Downer’s balance of plant work had been wrapped as per schedule as well as on the budget and 26 out of the 61 wind turbine generators are erected. However, all the remaining towers as well as blades are either at manufacturer’s premises, port or at Murra Warra site and 3 of 61 nacelles are in process of being manufactured, while a further three had been completed and are at manufacturer’s facility and remainder are either in Australia or in the transit to Australia (as per the release dated May 28, 2019).

Appointment of New Non-Executive Director: Downer EDI Limited had made an announcement about the appointment of Mr. Peter Watson as the Non-Executive Director, effective 22 May 2019. Mr. Watson joins Downer EDI Limited as Independent Director. The Chairman of Downer, named Mike Harding, stated that Mr. Watson happens to be an experienced CEO and Non-executive Director, including in industrial, transport, defence, health, justice, and utilities sectors.

Awarding of Chorus Field Services Agreement: Downer had made an announcement that they have been selected by Chorus Limited for 2019 Field Services Agreement. The new two-year-and-nine-month agreement would be providing field services for most of the country from Waikato to the Lower South Island and would be generating revenue amounting to around $220 million to Downer. The contract includes reactive maintenance and provisioning services, network maintenance routines, cable locates as well as build services and would commence on July 1, 2019.

The CEO of Downer, named Grant Fenn, had stated that the agreement would be expanding Downer’s delivery of extensive network maintenance and build services in New Zealand. Mr. Fenn also added that the contract doubles the geographic spread and they would be working with Chorus on construction as well as maintenance of their network.

Key Valuation Metrics (Source: Thomson Reuters)

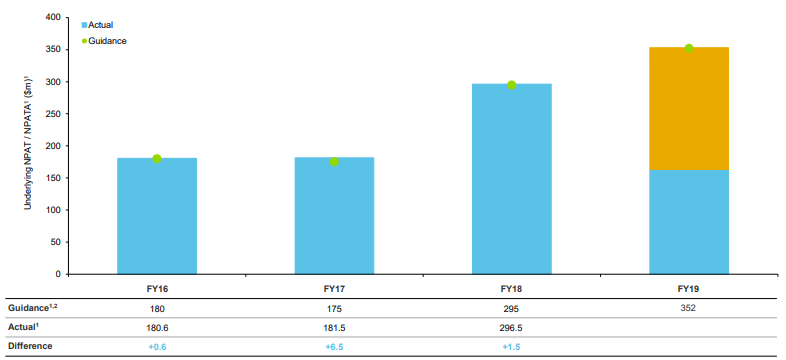

What To Expect From Downer: Downer’s Lost Time Injury Frequency Rate (or LTIFR) had witnessed a decline from 0.69 to 0.68 and Total Recordable Injury Frequency Rate (or TRIFR) got reduced from 3.38 to 3.09 per million hours worked. As per Macquarie Australia Conference, Downer had confirmed the previous FY 2019 NPATA guidance amounting to $352 million before the minority interests. For FY 2019, the company has a target of ensuring a safe environment for the employees with improving injury rates and well-being and it plans to deliver growth of 19% in FY19 in its EPS.

Downer has been targeting active capital management, and it plans to maintain the dividend pay-out ratio in the range of 50% – 60% of the NPATA. The company is focused on winning and delivering secure, long term service revenue as well as leveraging the expertise to drive the margin expansion over time. The company added that the services businesses give high quality and predictable earnings base.

Consecutive Financial Years Hitting (or exceeding) Guidance (Source: Company Reports)

At the end of December 2018, as per the Macquarie Australia Conference presentation, the company had work-in-hand amounting to $43.5 billion.

Valuation Methodologies:

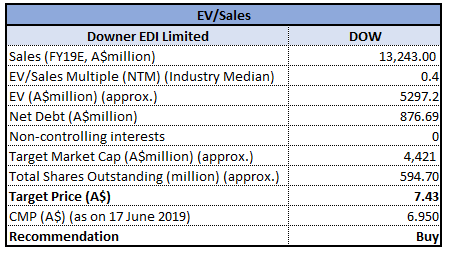

Method 1: EV/Sales Multiple Approach

EV/Sales Multiple Approach (Source: Thomson Reuters) *NTM-Next Twelve Months

Method 2: PE- based Valuation

PE- Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation: The stock of Downer EDI Limited has delivered the return of 7.53% in the span of previous 6 months while, on the YTD basis, it posted the return of 4.79%, which can be considered at respectable levels. The company’s performance bonding facilities amounted to $2,269.7 million at December 31, 2018 with $752.8 million undrawn. Downer added that there happens to be sufficient available capacity in order to support ongoing operations. The company’s net debt amounted to $940.0 million and has remained consistent to June 30, 2018, and the lower borrowing levels got offset by the reduced cash balances. Downer’s gearing at December 31, 2018 stood at 23.8%, which is higher than June 30, 2018 gearing of 22.7% but lower as compared to 1H FY 2018 gearing of 24.6%.

The company expects to maintain the conservative gearing position, which provides the balance sheet flexibility in order to help growth. Considering the strategic capital allocation, cost as well as capital efficiency and maintenance of the robust balance sheet and credit rating, we expect that the company might attract the attention of market players moving forward. Based on the foregoing, we have valued the stock using two relative valuation methods, P/E and EV/Sales multiple and arrived at the target price in the range of A$7.43-A$7.83 (single digit upside (%)). Hence, considering aforesaid facts and current trading level, we give a “Buy” recommendation on the stock at the current market price of A$6.950 per share (down 0.714% on 17 June 2019).

DOW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...