Company Overview: Downer EDI Limited provides services to customers in markets, including transport services, technology and communications services, utility services, rail, mining, and engineering, construction and maintenance. The Company's segments include Transport Services, which includes its road, rail infrastructure, bridge, airport and port businesses, and provides a range of transport infrastructure services, such as maintenance and earth works; Technology and Communications Services, including services, such as civil construction, network construction, commissioning and testing; Utility Services, including water lifecycle solutions for municipal and industrial water users and sugar cane waste fired cogeneration plants; Rail, including rail asset solutions, such as passenger and freight build; Engineering, Construction and Maintenance, which includes services, such as engineering design and civil works for projects, and Mining, including blasting services and exploration drilling services.

.png)

DOW Details

Downer EDI Limited (ASX: DOW), that has the market capitalization of $4.37 billion, is into offering various services in Australia, New Zealand, the Asia-Pacific, South America, and Southern Africa. The company operates through three divisions, Transport & Infrastructure, Mining, Energy and Industrial. The company caters to market sectors that include Minerals & Metals, Oil & Gas, Power, Transport, Telecommunications, Water and Property. While the group has been witnessing a few broad-market challenges, the positioning at financial and operational front is healthy, which is reflected through enhanced earnings guidance for FY19, cash backed earnings profile, flexibility of balance sheet while different arms such as growing urban services’ market provide further support. The proliferation of technology with population growth and government intervention and outsourcing are other key factors that lay out the potential DOW can derive through Transport, Utilities and Facilities’ segment. These aspects also reconcile well in terms of winning additional contracts from the government, better performance through increased EBITA margin to 4% in 1H FY19, and 7.7% rise in dividends. The cash scenario is supported by better cash flow conversion while the company also continues to invest in strategic acquisitions for growth. Then, work in hand worth $43.5 bn is expected to support the outlook and help achieve guidance along with other developments.

Received Order for 17 More Waratah Series 2 Trains from the NSW Government of about $900 million: DOW, the integrated services’ provider, has received order for more 17 Waratah Series 2 Trains from the NSW Government of total value of approximately $900 million, which also includes the maintenance of the trains. This is under its Sydney Growth Trains Project. Earlier the company had received order of 24 Waratah Series 2 trains under the same project in which 12 are now in passenger service. Between July 2011 and June 2014, seventy eight Waratah Series 1 trains had already entered the passenger service on the Sydney network. The company is expecting more such orders from the NSW Government for the Sydney network as Waratahs trains are very reliable and popular. This is expected to set the base for the future performance.

Decent First Half FY 19 Performance: Downer for the first half of FY 19 has delivered decent growth of 8.6% in the total revenue to $6.6 billion. There has been 5.9% rise in the total expenses during the period compared to the prior corresponding period (pcp), including $139.3 million of Individually Significant Items (ISIs). Excluding these ISIs, the company has posted 8.5% increase in the total expenses, which is in line with the rise in total revenue. During the 1H FY 19, DOW has delivered 20.6% increase in the statutory EBITA to $268.0 million versus the underlying EBITA of $222.3 million in corresponding period last year. This increase is primarily on the back of the performance of the segments Mining, Utilities, Transport and Facilities, which was partially offset due to the subdued contribution from EC&M. The 1H FY 19 EBITA includes the fair value gain of $17.0 million due to the revaluation of existing interest in the Downer Mouchel joint venture. This profit gain is due to the revaluation of the proportion of the joint venture that is already owned by DOW. Overall, for the first half of FY 19, the company has delivered 23.8% growth in the NPATA to $163.4 million. During the period, there has been $8.9 million rise in the corporate costs to $42.2 million driven by the company’s continuous investment on various functions related with the business. The company has also posted the effective tax rate of 27.3% which is lower than previous year’s tax of 30.0% on the back of the impact of non-taxable distributions from its joint ventures and lower overseas tax rates. Meanwhile, during the first half of FY 19, the company has witnessed strong operating cash flow with 15.7% rise from prior corresponding period (pcp) to $355.3 million. This is driven on the back of strong contract performance, distributions from equity accounted investment and amount received from acquisitions. Further, it represents the cash conversion of 90.7% of adjusted earnings. However, during 1H FY 19, the company has witnessed $381.7 million lower total investing cash flow of $265.7 million than pcp. This is due to the fact that the prior period had included payment related with the additional interest acquired in Spotless of $391.8 million. Excluding this Spotless payment, the investing cash flow has risen by 4.0%. During the 1H 2019, the net capital expenditure was of $175.4 million and payment for lease assets of $16.3m.

.png)

1H FY 19 Financial and Operating Performance (Source: Company Reports)

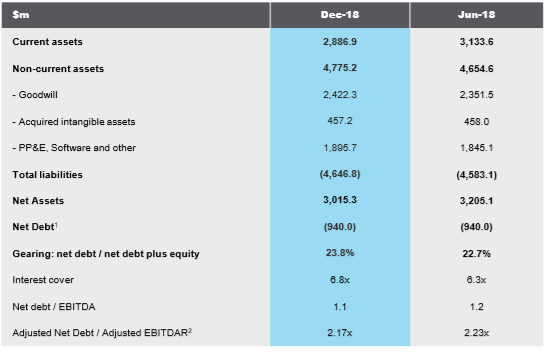

Financial Health During the First Half of FY 19: During the First Half of FY 19, there has been decline in the net assets of Downer by 5.9% to $3.0 billion, primarily due to the effect of the adoption of AASB 15 Revenue from Contracts with Customers. After adjusting this impact of AASB 15, the net assets have risen by $70.5 million. Overall, the cash and cash equivalents declined by 16.6%, to $505.3 million due to $106.3 million of external borrowing repayments that the company had paid during the 1H FY 19, $52.9 million consideration paid related with the business acquisitions and final working capital adjustment done for the divestment of Freight Rail in FY18. The company’s net debt of $940.0 million was consistent to level of 30 June. As at 31 December 2018, the gearing was higher at 23.8% from 22.7% as at 30 June 2018 but lower compared to 24.6% as at 1H18. There has been a 4.6% rise in the total trade and other payables driven by higher business activity and timing of payments. Trade and other payables form 51.9% of DOW’s total liabilities. The company has posted the deferred tax liability of $110.0 million for 1H 2019. During the first half of FY 19, there has been $189.8 million decline in the shareholder equity due to a $258.0 million cumulative opening retained earnings adjustment after the company’s adoption of AASB 15 and $87.4 million paid for dividend during the period.

Balance Sheet Scenario (Source: Company Reports)

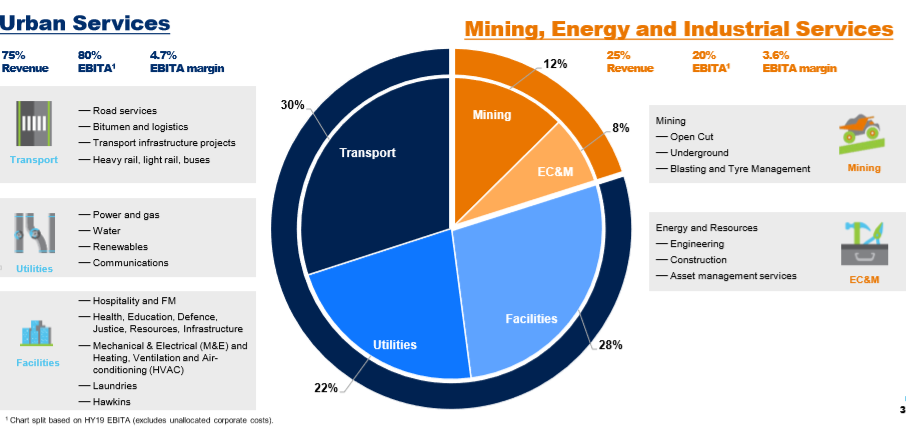

Almost All the Segments Grew for the first Half of FY 19: The company posted 0.8% growth in the Transport revenue to $2.1 billion. This rise is despite the revenue loss after the divestment of the freight rail business in the prior period. Further, the growth is driven due to the continuous strong performance in the Road Services business in both Australia and New Zealand, the continued investment in transport projects and also due to the strong performance in the Rail business, predominantly from the Sydney Growth Trains and High Capacity Metro Trains projects and also from the Waratah maintenance contract. There has been a 9.7% rise in the Transport EBITA to $87.9 million on the back of the continued strong performance in road maintenance in Australia and New Zealand and also due to higher contributions from the Waratah TLS contract. Utilities revenue grew by 27.5% to $1.2 billion for the 1H 2019, driven by the continued strong contributions from nbnTM contracts in Australia and new renewable energy projects. Utilities EBITA also grew by 19.6% to $64.7 million, due to the strong performance from Communications and higher contribution from the Water business. However, during 1H 2019, there has been 2.8% decline in the facilities revenue to $1.7 billion. The EBITA, still rose by 5.6% to $81.3 million mainly due to the growth in Hospitality & FM related contracts. EC&M revenue has risen by 34.1% to $945.1 million during 1H 2019 on the back of increased activities on the Ichthys project in the Northern Territory and also due to the six month contribution from MHPS. However, its EBITA declined by 4.7% to $22.4 million due to the completion of contracts. The company for the first half of FY 19 has posted 3.6% rise in the Mining revenue to $714.2 million, driven by the increased activities at Blackwater and Carrapateena and contribution from new contracts. Mining EBITA rose by 76.6% to $36.9 million on the back of robust performance on ongoing and new contracts.

Strength in Urban services’ space (Source: Company Reports)

Capital Management: As at 31 December 2018, the Group’s performance bonding facilities stood at $2,269.7 million and has undrawn amount of $752.8 million, which is enough to support the ongoing operations of the Group. As at 31 December 2018, the Group’s liquidity stood at $1.4 billion, that includes the cash balances of $505.3 million and the company has undrawn committed debt facilities of $855.0 million. The Group has the rating of BBB (Stable) by Fitch Ratings. Meanwhile, DOW has declared an interim dividend of 14.0 cents per share, which is 50% franked (13.0 cents per share 50% franked in the prior corresponding period), and will be payable on 21 March 2019 to shareholders on the record at 21 February 2019. The company will pay the unfranked portion of the dividend (50%) out of Conduit Foreign Income (CFI). Moreover, the company will pay a fully imputed dividend on the ROADS security and the next payment is due on 15 March 2019.

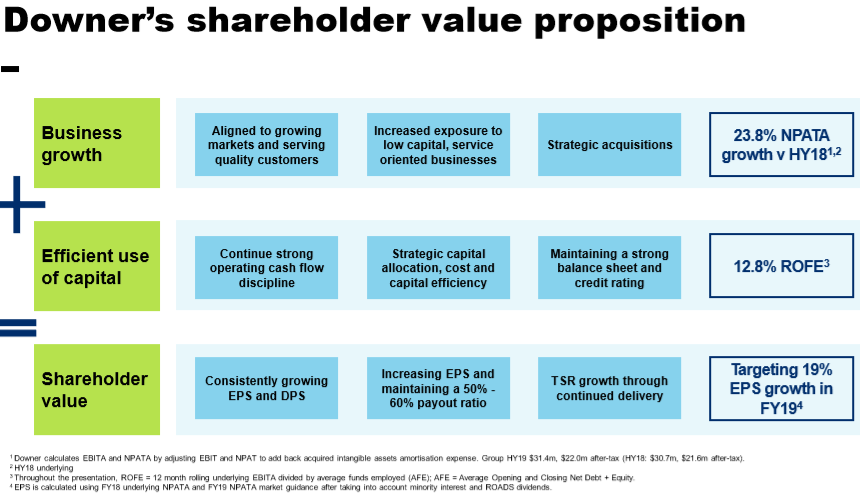

Value Proposition (Source: Company Reports)

Future Outlook: DOW has risen its guidance for FY19 of consolidated net profit after tax and before amortisation of acquired intangible assets (NPATA) before minority interests to $352 million. The company was earlier targeting the consolidated NPATA of $335 million before minority interests for the FY 19. This rise in projection is on the back of the fair value profit of $17 million that arose due to the acquisition of the remaining 50% of the Downer Mouchel JV in late 1H19.

Analysis depicts strong standing at margins’ front: It can be said that Downer EDI Limited is possessing robust standing when it comes to key margins’ position. The company’s net margin stood at 2.2%, at the end of December 2018, which implies the rise of 2.5% on the YoY basis primarily reflecting the strong capability of DOW to convert the top line into its bottom line. Also, the company’s operating margin has also witnessed a YoY improvement of 2.9% and this stood at 3.8% at the end of December 2018. We expect that the YoY improvement in the key margins might attract the market players’ attention and might help in creating the positive picture from the perspective of the company’s fundamentals. Moreover, the company’s return on equity or ROE has also witnessed a YoY improvement of 4.9% and stood at 4.5% at the end of December 2018. At the end of December 2018, the company’s current ratio stood at 1.00x and the debt-equity ratio happens to be 0.53x showing decent position.

On the monthly chart of Downer EDI, Exponential Moving Average or EMA has been used and default values were used for the purposes. After careful consideration, it was noted that the company’s stock price has crossed the EMA and had trended upwards and it might further witness a rise given the developments at hand.

Stock Recommendation: DOW stock has risen 9.21% in three months as on February 15, 2019 and is trading at a P/E of 20.43x. The company’s stock is trading at a price of $7.33, and has support at $6.03 and resistance at $7.94. The company has increased the guidance for FY19 of consolidated net profit after tax. It has posted decent growth in the first half of FY 19, with almost all its segments showing positive growth during the period. Therefore, we give a “Buy” recommendation on the stock at the current price of $ 7.33, given anticipated upside potential in the next 12-24 months.

DOW Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...