Company Overview - Downer EDI Limited is an Australia-based provider of engineering, construction and asset management services to the minerals and metals, oil and gas, power, transport, telecommunications, water and property sectors. The Company operates through three divisions. Downer Infrastructure operates predominantly in Australia and New Zealand and provides engineering services for critical infrastructure in both the countries. The division offers road infrastructure construction and maintenance; electrical and instrumentation services, and civil, structural and mechanical services, among others. Downer Mining delivers contract mining and civil earthmoving services. Downer Rail is engaged in the provision, maintenance and overhaul of passenger and freight rolling stock and the development of solutions for passenger cars, freight wagons, locomotives and light rail.

Analysis -

Downer EDI Limited (ASX: DOW)recently provided an update on their activities on Investor Day, 5 May, 2015. They have been actively rebuilding their brand for the past five yearsaddressing the target audience of investors, financiers, employees and customers.About 18 months ago they began a major push to develop a structure that is much more customer focused and consulted a range of customers to ascertain their perceptions and what the company had to do to outperform. Their customers responded by spelling out their expectations of safety, technical proficiency and high-quality delivery, responsiveness and value for money. They felt that the ingredients of outperformance were solutions and smart ideas, innovation being proactive and leveraging the entire gamut of capabilities. The company has also restructured itself into five operating divisions as follows:

.png)

Downer Divisions (Source - Company Reports)

The company sees its strengths in its market leadership, strong balance sheet and cash flow, refreshed brand and customer focus and programs to enhance efficiency and transformation. The company is establishing a platform from which it can take advantage of revival in the markets in which it operates. It has also confirmed its guidance of achieving NPAT of approximately $ 210 million in FY 2015.

Divisional activities

The company currently operates through three divisions Downer Infrastructure, Downer Mining and Downer Rail. Downer Infrastructure is one of the largest providers of critical infrastructure engineering services in Australia and New Zealand. It employs roughly 9500 people in Australia and 5500 people in New Zealand. It operates large-scale businesses in areas such as road infrastructure and E&I services. In the Australian telecommunications business, it owns and operates network and wireless infrastructure for customers and, in New Zealand, it is a major supplier to the telecommunications providers. It also operates three subsidiaries in the mining and resources sector. Downer Mining has been providing contract mining and earthmoving services for almost a century and, with 3500 employees on approximately 60 sites, it is a highly diversified mining contractor. Downer Rail is a leading Australian rail transport solutions operator with almost 1400 employees. It has strategic partnerships with the like of Bombardier and Hitachi.

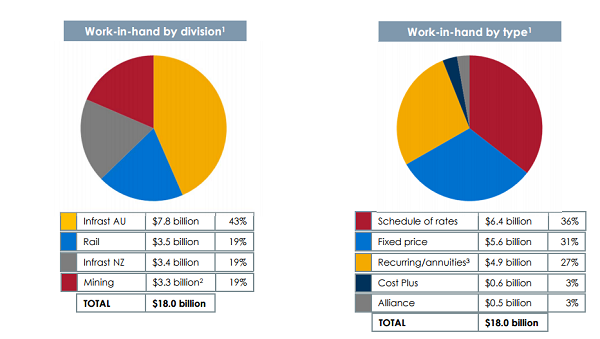

Work in hand (Source - Company Reports)

Results for the half-year ended 31 December 2014

Work in hand (Source - Company Reports)

Results for the half-year ended 31 December 2014

The group reported declines in total revenues and EBIT compared to the previous period because of the completion of several projects and the subdued markets in infrastructure and mining. Total revenues declined by 8.8% to $ 3.6 billion with lower revenues from the mining and rail activities offset by a 1.1% increase in infrastructure revenues to $ 2.3 billion. Mining revenues at $ 816.2 million were down by 20.4% and rail revenues at $ 424.4 million were down by more than 26%.

Employee benefit expenses declined by 5% to $ 1.3 billion and constituted 38.6% of the total cost basis. This is roughly in line with the total revenue reduction. Sub contracting costs also declined by 2.5% and at $ 757 million account for 23.4% of total costs. This is in line with the strategy of the group to use sub contracting to increase or decrease activity without incurring permanent fixed costs.

EBIT declined by 11% to $ 141.7 million largely because of the decline of Australian activity. The figure for infrastructure declined 16.7% to $ 72.8 million, the New Zealand business 34.9% to $ 20.3 million, the mining business 29.6% to $ 63.4 million and the rail business increased by 279.4% to $17.5 million as a result of restructuring. Corporate costs reduced by 13.9% to $25.9 million because of productivity increases and lower volumes while net finance costs fell by 41.9% to $ 13.6 million as a result of lower interest rates and repayment of higher cost borrowings.

Liquidity and capital are managed at group level and divisions focus on the management of working capital and operating cash flow. Operating cash flow at $ 257.9 million continued to be robust though down 8% over the previous period and EBITDA conversion was 103.5%. Investment in capital equipment primarily for maintenance continued and the net capital investment at $78.7 million was down 49.7% over the previous period. Liquidity at the end of the half-year was approximately $ 1 billion comprising of cash of $ 376 million and undrawn facilities of roughly $ 612 million.

.png) Financial Highlights (Source: Company Reports)

Infrastructure

Financial Highlights (Source: Company Reports)

Infrastructure

The market continues to be highly challenging as a result of low commodity prices and reductions in capital investment. The environment for tendering remains very competitive with a reduction in the number of opportunities and pressure on margins. The consulting businesses such as Snowden, QCC and Mineral Technologies made losses during the half year while New Zealand was impacted by lower margins and a reduction in UFB volumes. On the positive side, the Tenix acquisition provides growth opportunities and other market sectors such as oil and gas, transport and telecommunications also offer attractive opportunities. The business is continuing to focus on managing costs and exploring new markets and services opportunities.

.png) Infrastructure Division Highlights (Source - Company Reports)

Mining

Infrastructure Division Highlights (Source - Company Reports)

Mining

The continued pressure on commodity prices remains a major challenge for customers and the lower revenues registered by the business were due to the premature termination of the Goonyella contract, the completion of the Daunia contract and the reduction in volumes. However, in December 2014, the company received two Letters of Award of a value of more than $ 2 billion from Adani Mining for mining services and infrastructure construction at the Carmichael Coal Mine in Queensland. In addition, there are opportunities to help customers reduce the cost of doing business.

.png)

Mining Division Highlights (Source - Company Reports)

Rail

The lower revenue was due to the completion of the contract for the Waratah Train Project Rolling Stock Manufacture. However, restructuring costs at $ 2.4 million for HY 2015 were considerably lower than $ 10.5 million for the previous year and the WTP Through Life Support contract is showing robust performance. A ten-year asset management contract worth $ 1 billion has been concluded with Pacific National. The Gold Coast Light Rail became operational in July 2014 and is showing good performance and Keolls Downer is pursuing other growth opportunities in public transport in Australia and New Zealand. Other opportunities include the NSW intercity train Project as well as the Dandenong train Project in Victoria.

.png) Rail Division Highlights (Source - Company Reports)

Acquisition of Downer Tenix

Rail Division Highlights (Source - Company Reports)

Acquisition of Downer Tenix

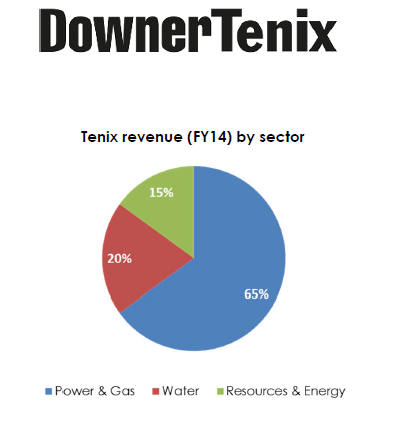

Tenix Holdings Australia was acquired on 31 October 2014 for $ 300 million on a cash and debt free basis and rebranded as Downer Tenix. It is a leading operator of long-term operations and maintenance services in Australia and New Zealand to businesses which own assets in electricity, gas, water and other resources. It represents an excellent strategic fit and is well placed to take advantage of opportunities arising from the outsourcing by state governments of maintenance and asset management. The integration is proceeding satisfactorily.

Tenix Revenue (Source - Company Reports)

Tenix Revenue (Source - Company Reports)

The company has announced that it has successfully completed the extension of the Group's A$400 Million Syndicated Debt Facility (Facility).The Facility, which closed in April 2013, had an initial maturity of four years and included options to be exercised in April 2014 and April 2015 to extend the term for an additional one year period. The first option was exercised in April 2014. The second option has now been exercised and the Facility matures in April 2019.At the same time, the pricing has been reduced to reflect both the general contraction in credit market spreads and the improvement in Downer's credit profile. The Group is rated BBB (Stable) by Fitch and the extension is a reflection of the support that the group continues to receive from its banks. The latest terms will reduce funding costs while extending the weighted average debt duration.

Downer Daily Chart (Source - Thomson Reuters)

Downer Daily Chart (Source - Thomson Reuters)

We put a BUY recommendation on the stock at the current price of $5.19.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...