Company Overview - Downer EDI Limited provides engineering, construction and asset management services to customers in the Minerals & Metals, Oil & Gas, Power, Transport, Telecommunications, Water and Property sectors. It operates through three divisions: Downer Infrastructure, Downer Mining and Downer Rail. Downer Infrastructure Australia provides a suite of engineering, construction and project management services in the public and private infrastructure industries. The industries in which Downer Infrastructure Australia is involved include construction, road and rail infrastructure, power systems including transmission lines and renewable energy, asphalt, mining and materials handling, minerals processing, communication networks and water treatment and management. Downer Infrastructure New Zealand provides essential services for the construction, development, management and maintenance of road and rail assets in the public and private sectors. Downer Mining provides contract mining services.

Analysis – In the past decade despite a highly supportive macroeconomic environment, Downer EdI’s financial results have been mixed with strong profitability in one division often offset by losses in another division. Lack of earnings stability and legacy issues surrounding a major passenger train contract have continued to plague the company. In the past Downer has also underperformed from an operational perspective but now appears to have learned the hard lessons and is building solid positive momentum.

Group Revenue (Source - Company Reports)

Group Revenue (Source - Company Reports)

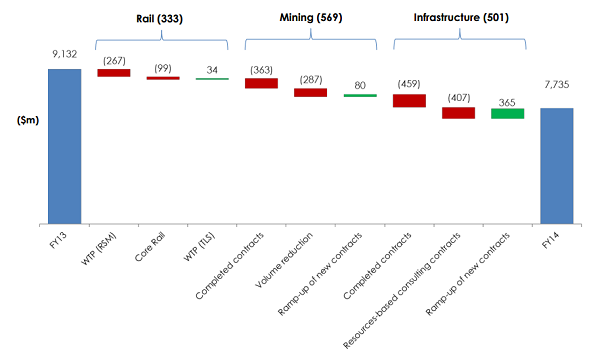

A largely unsurprising fiscal 2014 result from Downer EDI, with operating revenue down 12% to AUD 7.4 billion, earnings before interest and tax or EBIT down 5% to AUD 341 million and net profit after tax or NPAT flat at AUD 216 million. Although Downer’s revenue decline was slightly stronger than expected earnings were in line with our forecasts. All three operating divisions (infrastructure, mining and rail) reported lower revenue as the mining downturn continued to bite. A sustained decline in resources sector capital expenditure and operating cost containment among miners have combined to create tough environment to achieve growth.

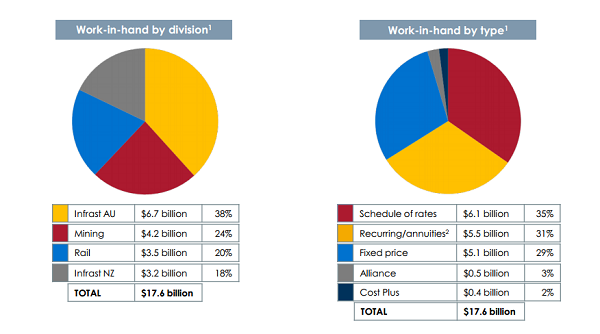

Work In Hand (Source - Company Reports)

Work In Hand (Source - Company Reports)

Fortunately during the past year Downer moved rapidly to adopt a cost out strategy which resulted in the company’s EBIT margin increasing to 4.4% from 3.9% in the prior year. Downer’s operating cash flow remained robust up 30% to AUD 583 million. A final dividend of AUD 0.12 per share fully franked was declared up 9% on the prior year. Management guided to fiscal 2015 NPAT of AUD 205 million , down 5% from fiscal 2014 de3spwite lower operating and financing costs .

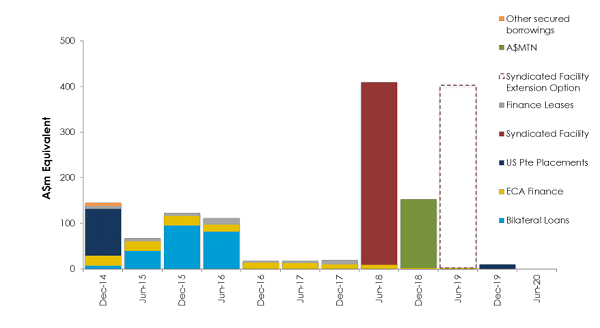

Debt Maturity Profile (Source - Company Reports)

Debt Maturity Profile (Source - Company Reports)

Downer has established a solid competitive position benefiting from scale and strong customer relationships. The business continues to build strong momentum towards delivery of substantially better operational performance but there is no escaping the mining downturn. In fiscal 2014 Downer’s infrastructure operations contributed 61% of operating revenue and 50% of EBIT. Nevertheless operating revenue was down 2% and EBIT fell by 17% mainly reflecting large decline in mining capital expenditure and limited new resource projects. Completion of committed and under construction mining projects during fiscal 2015 continues to look relatively assured, but expansion and new projects look increasingly improbable in a difficult and challenging environment. Positively Downer’s infrastructure operation starts fiscal 2015 with AUD 9.9 billion of work in hand up 5% on the prior year as a result of engineering contract wins on domestic LNG projects and road infrastructure contact wins in New Zealand.

Infrastructure Revenue + EBIT (Source - Company Reports)

Infrastructure Revenue + EBIT (Source - Company Reports)

Downer’s mining and rail businesses contributed 39% of group operating revenue and 50% of EBIT, in fiscal 2014. Mining operating revenue declined by a large 22% though EBIT fell by just 2%. Revenue was impacted by reductions in the scope of contracted work at BHP Billiton Mitsubishi’s Alliance Goonyella Coal mine and Fortescue Metal Group’s Christmas Creek Iron Ore mine. The strong EBIT margin expansion was the result of cost cutting, productivity improvements and equipment financing changes.

Mining Revenue + EBIT (Source - Company Reports)

Mining Revenue + EBIT (Source - Company Reports)

Downer is a major domestic engineering and maintenance business, which undertakes mining services and the manufacture of rail rolling stocks. The company’s major exposure is to the domestic mining, energy, rail, road and telecommunications sectors. Downer’s infrastructure business focuses on long term low margin schedule of rates contracts and contributes 55% to 60% of total operating revenue. Downer provides a diverse range of contracted services across numerous industries in Australasia. Non mining work undertaken varies from installation work for Foxtel’s satellite’s customers to open space (parks, nature strips and sporting fields) management for Auckland council.

Rail Revenue + EBIT (Source - Company Reports)

Rail Revenue + EBIT (Source - Company Reports)

Strong operating cash flow and payments associated with the completion of the Waratah rail project allowed Downer to reduce net debt tor AUD 33 million, including derivatives and deferred finance charges at the end of fiscal 2014. Gearing is low at 2% although including off balance sheet financing raises gearing to 9%. We believe by the end of first half fiscal 2015, Downer will be in net cash positive position and may consider acquisitions. We strongly endorse Downer’s decision to undertake share buyback as an excellent use of excess cash while only limited growth opportunities exist.

DOW Daily Chart (Source - Company Reports)

DOW Daily Chart (Source - Company Reports)

Despite significant efficiency and contract management ability improvements, Downer faces headwinds including mining project delays and increased customer bargaining power in the mining service contact negotiations. However management is taking necessary steps to ensure the company is well placed to weather the storm and build positive momentum.

Downer is in solid financial health due to an AUD 272 million equity raising in March 2011, AUD 147 million sale of the company’s CPG Asia consulting business and strong capital management. Downer ended fiscal 2014 with net debt of AUD 33 million. Operating cash flow remains buoyant. The company has forecast capital expenditure of less than AUD 300 million during fiscal 2015. During fiscal 2013, Downer commenced paying dividends to shareholders again, after stopping in fiscal 2010. We believe Downer will move to a net cash position during fiscal 2015.

Fiscal 2012 was the turning point for Downer, with the company emerging from a period of transformation. The restructurings, write-downs, project losses and contract disappointments are over and profitability is stable. Since being appointed in July 2010, CEO Grant Fenn has successfully restored confidence with recent infrastructure contract wins and introduction of the new project management framework providing further momentum in reestablishing the company’s reputation. Downer’s recurring revenue streams and stable cash flows from operations and maintenance contracts in the social infrastructure, transport, telecommunications and government sectors are helping to partially insulate the company from downturn in mining and energy work. We put a BUY on the stock at the current price of $4.77.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...