Company Overview - Donaco International Limited is engaged in operating leisure and entertainment businesses across the Asia Pacific region. The Company's segments are Casino operations-Vietnam, Casino operations-Cambodia and Corporate operations. Its Casino operations-Vietnam segment consists of the Aristo International Hotel operating in Vietnam, hotel accommodation, and gaming and leisure facilities. Its Casino operations-Cambodia segment consists of the Star Vegas Resort and Club operating in Cambodia, hotel accommodation, and gaming and leisure facilities. Its Corporate operations segment consists of the development and implementation of corporate strategy, commercial negotiations, corporate finance, treasury, management accounting, corporate governance and investor relations functions. The Star Vegas Resort and Club has over 100 gaming tables, more than 1,400 slot machines, and 385 hotel rooms. The Aristo International Hotel has approximately 400 hotel rooms.

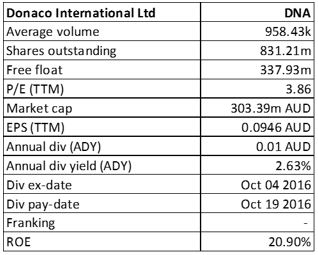

DNA Details

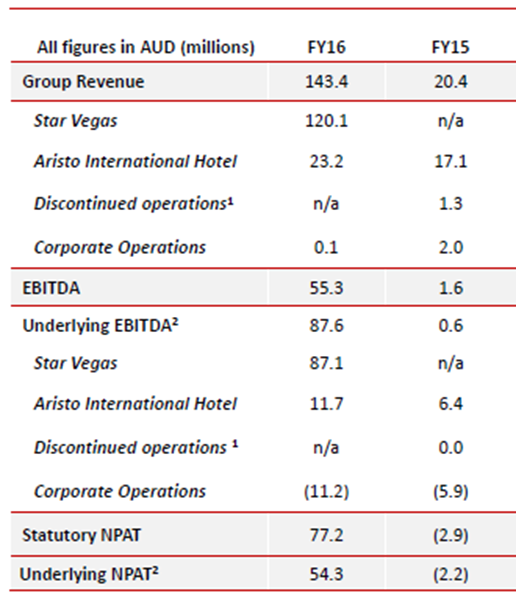

DNA Star Vegas acquisition led to a seven-fold rise in FY16 group revenues: Donaco International Ltd (ASX: DNA) had successfully integrated the newly acquired DNA Star Vegas in Poipet, at Thailand and Cambodian border during financial year (FY) of 2016. This acquisition has led to a seven-fold increase in the group revenues. Moreover, the group has been enhancing their performance at Aristo International Hotel, in Lao Cai in Vietnam during the period driven by strong growth in both gaming and non-gaming revenue. Meanwhile, DNA has reported the group revenue of A$143.4 million in FY16 up from A$20.4 million in the prior corresponding period. This performance includes revenue from Star Vegas of A$120.1 million and the Aristo’s revenue of A$23.2 million, which has grown 36% as compared to FY15. On the other hand, DNA has posted a statutory NPAT of A$77.2 million in FY16, against a loss of A$2.9 million in FY15. The NPAT includes the valuation uplift of A$55.2 million for Star Vegas, A$20.5 million management fee payable to the venue manager due to the strong performance of Star Vegas and A$11.8 million of non-recurring M&A costs for acquisition of Star Vegas. Moreover, DNA also posted strong operational results as the group EBITDA grew to A$87.6 million (before non-recurring items) in FY16 against A$0.6 million in FY15. Therefore, the adjusted group EBITDA is of A$97 million, exceeding the guidance of A$90-95 million in which Star Vegas has posted 21% increase in EBITDA in local currency terms to Thai Baht 2.2 billion. Aristo has posted a 62% rise in EBITDA in local currency terms to RMB 51 million. The Star Vegas EBITDA is USD 63.3 million during FY16 exceeding the target of USD 60 million.

Financial Performance in 2016 (Source: Company Reports)

Growth at DNA Star Vegas:Star Vegas acquisition has transformed the growth scale of DNA’s operations. Star Vegas is the most luxurious Poipet casino hotel having 385 guest rooms, Sports Bar with wagering license (sports and racing), multiple restaurants, shops, health spa, pool and growing non-gaming revenues. Further, there are substantial casino facilities having 139 gaming tables, predominantly baccarat, 1,566 Electronic Gaming Machines (EGMs), of which 288 are owned outright and 1,278 are under profit share deals. Moreover, DNA is positive about the growth of DNA Star Vegas through leveraging the Manchester United relationship, VIP promotions and the recent expansion into the neighboring Star Paradise property. Additionally, Star Vegas business also owns an online gaming license that is yet to be utilized and the company is currently exploring the alternatives for the utilization of this license and expects to make some progress during FY17.

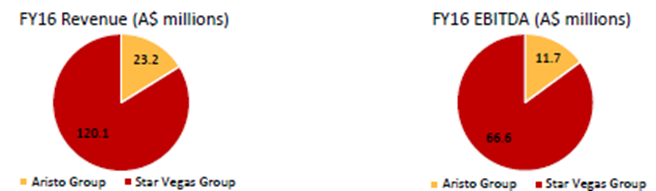

Star Vegas and Aristo Group Performance in FY16 (Source: Company Reports)

Star Vegas -Star Paradise deal: DNA has finished the deal to expand the Star Vegas gaming business into the adjoining Star Paradise property, and started managing the gaming floor for a monthly fee from the start of September. After the deal, there is a further capacity to allow for new Thai junkets and new players and in addition to the monthly fee, DNA would get the reimbursement of the operating costs incurred by Star Vegas for the venue. All costs and risks related with the venue development will be borne by DNA’s Thai partner and DNA requires no capital expenditure in this deal. Moreover, DNA is finalizing an exclusive option to acquire the entire Star Paradise business. The expansion of Star Vegas into Star Paradise is a major strategic move for DNA which would solidify the market-leading position in the Poipet region. Further, the additional earnings for managing Star Paradise is expected to complement DNA’s core earnings from Star Vegas.

Strength of the corporate governance practices: DNA recently gave an update on their corporate governance practices and reported that they are widely recognized by governments and the customers as the group operates with high standards of probity and governance. DNA believes that strong corporate governance principles would give them a solid competitive advantage while looking for further growth opportunities as they arise.

Reduction in Debt: DNA is reducing its debt and accordingly reported a net debt to equity of 15% in FY16. Moreover, DNA is focused on paying down the rest of the acquisition financing as a priority and is expected to pay all the debt in 12-18 months. DNA had renegotiated and refinanced the debt facility in July on more attractive terms that would further reduce the financing costs over the next two years. Particularly, DNA has refinanced USD 20 million working capital facility in July, which would control their financing costs over FY17 and FY18. Meanwhile, DNA bought over $1 million worth of shares on market for the newly established long-term incentive scheme. The grouphas also declared and paid a maiden dividend of 1 cent per share in FY16.

.png)

Aristo International Performance (Source: Company Reports)

Mixed performance for first four months of FY17: DNA experienced a mixed performance during the first four months to the end of October 2016. The Aristo delivered a very strong start on the back of high growth in visitation of 75% and a strong VIP win rate of 3.41%, but DNA Star Vegas results are lower than a very strong comparative period from last year. In the first four months of FY17, DNA Star Vegas has recorded a VIP win rate of 2.87% as compared to 3.31% in the corresponding period last year, which is still a decent performance. Overall, in the first four months of FY17, DNA has reported the revenue of A$42.0 million, which is $9.8 million lower than the corresponding period last year, on the back of strong comparative period at DNA Star Vegas last year. On a normalized basis, the net profit after tax is approximately A$1.7 million which is lower than the first four months of FY16.

Improving Outlook for FY17: Star Vegas would get the benefit from new markets and VVIP gaming growth, while the Star Paradise expansion would lead to new Thai junkets and players which would contribute further towards recurring revenue from FY17. The marketing strategies for Aristo are expected to increase several mass-market players visiting the property and expected to reduce the volatility in win rate and earnings. Additionally, DNA started discussions with the Thai partner regarding the on-going management of DNA Star Vegas into FY18 and beyond. Though these arrangements are not yet finalized, they would be commercially based and reflective of senior executive remuneration packages.

Stock Performance: DNA stock price fell about 15.5% in the last four weeks (as of December 19, 2016) partly owing to certain sector driven headwinds on casino and gaming players. However, the stock is placed at attractive valuation and available at a very cheap P/E, while growth prospects are seen going forward. We believe the group is in a growth phase and the company is aiming to retain sufficient cash to pursue growth opportunities and repay the debt as a priority. Moreover, DNA is well positioned to take advantage of consolidation and growth opportunities in the leisure and hospitality industry in the Asia-Pacific region. Additionally, the corporate costs as a percentage of revenue are expected to decline as the business scales up. All-in-all, growth prospects from gaming in Asia region, high margin status of its properties, strong cash flows, debt repayment and dividend payments are key factors to look upon. We give a “Buy” recommendation on the stock at the current price of – $ 0.38

DNA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...