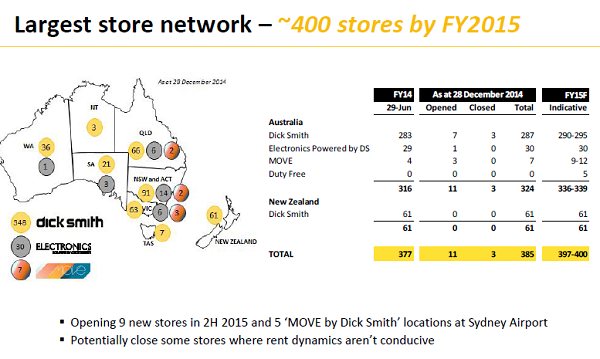

The Company’s strategy entails to have profitable growth in sales by delivering to consumers the products of their choice at affordable prices using locations and platforms most convenient for them. This is being implemented by giving consumers the choice of shopping at an unparalleled network of 385 stores throughout Australia and New Zealand as well as an online purchasing experience delivered through multiple platforms. Since the launch of the growth strategy 18 months ago, the Company has opened 65 new stores and grown as the fastest growing consumer electronics store network in Australia with 11 stores opened in first half of 2015 and a further 9 new stores planned for the second half of 2015. The segmentation of the network into three new formats catering to different demographics has attracted new demand as well as increased brand awareness and improved consumer perceptions. Online sales have grown from 5% of retail sales in the previous half year to 7% in the current period and the Company is confident of achieving its objective of 10% before the stipulated date of financial year 2017. The private label sales have also shown encouraging results amounting to 12% of retail sales for the half-year and the Company is well positioned to achieve its goal of 15% by the financial year 2017.

Store Network (Source: Company Reports)

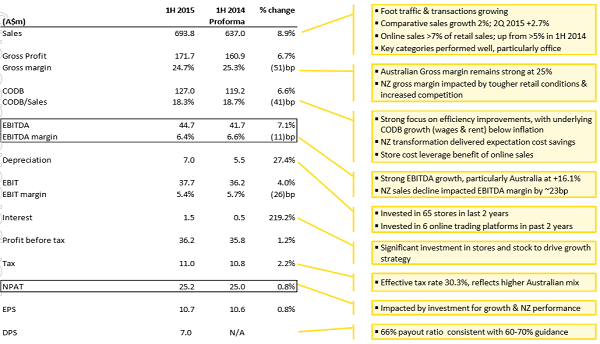

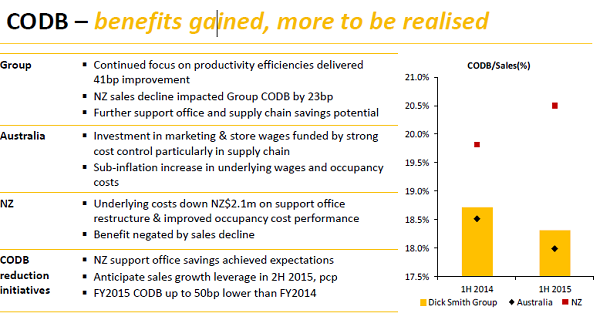

As mentioned above, the Company achieved a gross profit margin of 24.7% of sales (25.3% in the previous half year). The gross margin was well protected through product mix and Private Label sales though the gross profit was hit by a 2.01% decline in the New Zealand gross margin due to the significant increase in competitive activity and a deteriorating retail market. The Company continues to focus on achieving cost efficiencies throughout the business and CODB in the first half of 2015 was 18.3%, down 0.41% on the previous period. The reduction was because of the benefits of the amalgamation of the New Zealand support office into Australia in February 2014, which resulted in New Zealand’s CODB reduce by NZ$2.1 million along with increased efficiency initiatives in Australia and fixed cost leverage resulting from the new stores opened in Australia. The reduction was achieved despite the negative effect of approximately 23 basis points arising out of the softness in New Zealand sales.

CODB (Source - Company Reports)

We like DSH’s strong balance sheet with no outstanding debt as at 28 December, 2014 indicating the conservative approach to leverage. Inventory was strongly controlled throughout the period and the increase in inventory levels places the Company in a strong position to continue sustainable growth. This includes the continuing opening of new stores and expansion of Private Label brands, utilising warehousing capacity in Sydney and Auckland to reap the benefits of favourable currency movements and catalysing future growth including five new ‘MOVE by Dick Smith’ locations at Sydney Airport. The Company also took advantage of a number of opportunities in January/February, which necessitated purchasing inventory prior to the peak Christmas season.

The sales performance for the second half of 2015 so far has been superior to the 8.9% growth in the first half despite the continuation of difficult trading conditions in New Zealand. January sales are up by more than 17% and February sales have been shown to have double-digit growth. Total sales growth in the year were recently reported to be more than 10% and comparative sales growth has been around 3%.Nick Abboud, Dick Smith Managing Director & CEO, expects to achieve a minimum of 10% growth for the financial year 2015 and believes that the Company is well placed to deliver further strong sales and profit growth over the next 18 months. In addition to the Sydney Airport Duty Free stores that commenced lately, the Company intends to open 9 new stores in 2H 2015 and 20 new stores in FY2016. In FY2015, EBITDA growth of 7-9% and NPAT and EPS growth of 3-5% has been estimates, which in a way reflects the continued investment in future growth opportunities.

.png)

Online Sales (Source – Company Reports)

The Company unveiled its latest cost-cutting initiatives in the third week of March 2015 by announcing about elimination of 80 jobs from its head office, IT and supply chain management. This is the latest response to the generally weaker trading conditions reflected in the up-to-date half yearly results and is expected to generate cost savings of between $ 8 million and $ 12 million as of July 2015 though there will be one-off costs associated with the initiative. The Company expects that the initiative will keep it on track in achieving the objective of slashing cash costs of doing business to around 18% by the financial year 2017. Increased revenues from rolling out new stores and strategy to focus more on low-cost online sales appear to be fruitful for DSH.

.png)

Profit and Loss_Australia (Source – Company Reports)

Overall, positive results for the first half year, increase in dividend yield and the positive outlook on sales growth look appealing. Growth in EPS is expected in long term from the opening of additional new stores, cost-cutting initiatives, the increasing share of private brands in revenues and a greater share in revenues of lower-cost online sales.

DSH Daily Chart (Source - Thomson Reuters)

We believe that the future growth prospects are attractive on a realistic basis and the focus on private label sales and online sales will improve gross margins especially when combined with the continuing cost savings. We also believe that the Company will be able to overcome the weakness in share prices seen over the past few months owing to the soft retail environment in Australia and New Zealand as well as the difficult trading conditions in New Zealand. Despite these concerns, DSH has taken proactive and aggressive measures to continue the upward trend of revenue growth. In fact, we believe that the recent share price weakness has created a buying opportunity.

Accordingly, we put a BUY recommendation for this stock at the current price of $1.97.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...