Company Overview – Decmil Group provides engineering and construction services to the Australian Resources and energy sectors. The company focuses on accommodation villages and facilities as well as civil works. It undertakes construction of remote site accommodation villages on either a permanent or temporary basis for LNG, Mining and Government clients; civil works, including concrete formwork for the resources sector; construction of non-process ancillary buildings such as workshops, storage facilities, offices etc. for the resources sector; Build, own and operate accommodation villages for the resources sector. Decmil owns a 1392 person camp in Gladstone, Queensland.

Analysis – Decmil’s contracts with the Australian Department of Immigration and Border Protection on Manus Island comprise a significant proportion of DCG’s work in hand of $314m in 2HFY14 and a further $283m extending into FY15. We understand that work under the phase 1 contract for the Manus Island Offshore Processing Centre (OPC) at Lorengau (contract value: $137m) is on track for expected completion in late September 2014. The Manus Island Phase 2 contract (OPC Lombrum; initial contract value: $147m) on the current scope has an expected completion date of mid – January 2015.

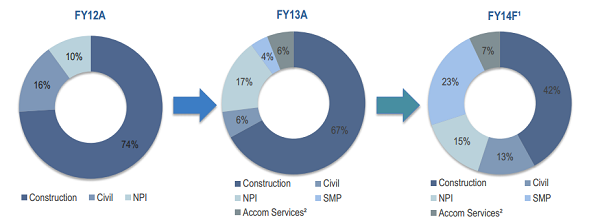

Revenue By Capability (Source - Company Reports)

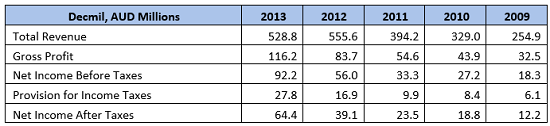

The $80m extension to EDE’s QCLNG Wellhead Installation Services Contract (Value: up to $196m) involves a scope of 800 wells (completion Sept-Dec 2014) and comprises the second increment of a possible 5,000 well program. In addition to this contract ( with good revenue visibility), EDE has other wellhead and fabrication opportunities. Decmil reported a record half that delivered NPAT of $25.7m above our expectations. Gross operating cash flow to EBITDA conversion came in at 123% and continued the trend of very strong cash conversion. This saw Decmil’s net cash position increase to $44 million (from $21 million at FY2013). Decmil’s balance sheet leaves it positioned for growth. Management has disclosed that 2H revenues are likely to be 28% higher than the 1H. Management expects the FY2015 revenue to be higher than FY2014.

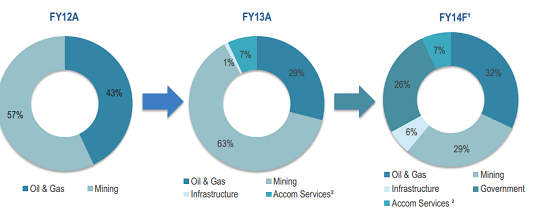

Revenue By Geography (Source - Company Reports)

Revenue By Geography (Source - Company Reports)

DCG had $1.8bn in tenders and EOI’s as at 31

st January 2014. Since then DCG has missed out on the Roy Hill Package One Concrete and Detailed Earthworks Contract (value: $200m) awarded to NRW Holdings on 17 April 2014. DCG has high visibility and high occupancy at Gladstone for contracted and non contracted tenancies ( the latter with higher room rates) through to end CY14. We assume softer demand for accommodation during CY15. We share DCG’s confidence that demand from LNG sector tenants and others will rise starting from CY16 based on expectations for maintenance/shutdown services. As an example of the potential demand for shutdown services there were 300 service personnel staying at Homeground Villages in Gladstone (capacity: 1392 rooms) for the March Quarter Shutdown at the Boyne Island aluminium smelter.

Revenue By Sector (Source - Company Reports)

Revenue By Sector (Source - Company Reports)

Decmil has a strong reputation within the resources services industry and has a tier 1 client list in government, mining and LNG. It’s exposure to LNG is one of the highest of its peers. On financial benchmarking against other contractors, Decmil ranks very highly. Its long term cash flow conversion is excellent. The Gladstone accommodation village adds a large portion of recurring earnings and could see the company carry a higher multiple. The Manus Island detention centre contract has been materially increased and further detention work could eventuate. The recent contract wins ensure that a high proportion of FY2015 revenue is locked away. With Eastcoast Development Engineering (EDE) acquisition, Decmil has diversified from mining early.

Group's Prescence outside Western Australia (Source - Company Reports)

Group's Prescence outside Western Australia (Source - Company Reports)

Over the past year DCG has executed a diversification strategy securing work in new regions ( Northern Territory and Papua New Guinea); in new sectors (Government) and with new service offerings ( structural mechanical and piping; and R4/B2 Main Roads accreditation to extend the Group’s civil offering).Oil & Gas sector represents $185m worth of revenues for FY 14 (slightly adjusted) mostly the QCLNG contract but also the balance of the Gorgon construction village for Chevron and Shell’s Prelude supply base ($29m); Mining sector represents $164m worth of revenue including early revenues for three Roy Hill contracts ( terminal buildings, port buildings, diesel fuel infrastructure); Buffel Park Village construction for Caval Ridge; RIO’s Western Turner workshops ($30m) and Mt Webber Roadworks for Atlas Iron ($36m); Government sector represents $145m worth of revenue which includes the Phase 1 contract for the Manus Island Offshore Processing Centre (OPC) at Lorengau ( contract value:$137m). Infrastructure sector represents $34m worth of revenues which include the construction and realignment of 5KM of the Bruce Highway for the Department of Transport and Main Roads ($34m).

DCG had $1.8bn in tenders and EOI’s as at 31

st January 2014. Since then DCG has missed out on the Roy Hill Package One Concrete and Detailed Earthworks Contract (value: $200m) awarded to NRW holdings. There is an adjusted $1.6bn pipeline of tenders and EOIs (excluding any recent tenders/EOIs). This would comprise of Oil & Gas ($468m) targeting upstream and midstream LNG in QLD. Also includes a Wheatstone LNG tender. Mining ($556m) of which now iron ore accounts for $270m (previously $470m). Coal comprises only $40m. Government ($504m) and infrastructure (35m) of which roads and bridges combined comprise of $350m. Government tenders have been boosted by DCG’s relatively recent R4/B2 Main Roads accreditation which has extended the company’s civil capability. There are potential scope extensions at Manus Island.

DCG Daily Chart (Source - Thomson Reuters)

DCG Daily Chart (Source - Thomson Reuters)

DCG delivered another stronger than expected result, demonstrating solid construction margins against a tough backdrop and better than projected Accommodation profitability. The outlook for the business appears good with the diversification strategy providing offsets against the mining sector downturn. We regard DCG as relatively well placed within the sector. The balance sheet is strong and the mix shift towards more recurring Accommodation earnings is a positive in our view. We reiterate our BUY recommendation on the stock at the current price of $1.82.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...