Company Overview – Decmil Group provides engineering and construction services to the Australian Resources and energy sectors. The company focuses on accommodation villages and facilities as well as civil works. It undertakes construction of remote site accommodation villages on either a permanent or temporary basis for LNG, Mining and Government clients; civil works, including concrete formwork for the resources sector; construction of non-process ancillary buildings such as workshops, storage facilities, offices etc. for the resources sector; Build, own and operate accommodation villages for the resources sector. Decmil owns a 1392 person camp in Gladstone, Queensland.

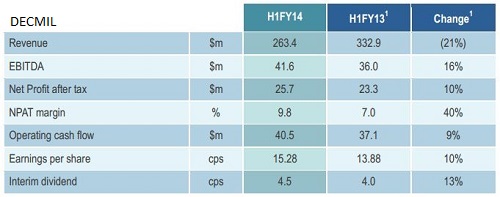

Analysis – Decmil group reported 1H Net Profit After Tax (NPAT) of $25.7m, reported a dividend of 4.5 cents per share. EBITDA was $41.6m, operating cash flow was $40.4m and Net Cash was $43.7m. Decmil has a strong reputation in the resources services industry and has a tier 1 client list in government, mining and LNG. It’s exposure to LNG is one of the highest of its peers. Decmil ranks very highly against other contractors; its long term cash flow conversion is excellent. The Gladstone accommodation village adds a large portion of recurring earnings. The Manus Island detention centre contract has been materially increased and further detention centre work could eventuate. The recent contract wins ensure that a high proportion of FY2015 revenue is locked away.

While revenue of $232m was down on the previous corresponding period the company has guided that it has $314 million of work in the order book relating to the 2H2014 and in addition we expect revenue in the accommodation division to be materially ahead of what is contracted. Margins were described as likely to fall marginally in 2H2014 none the less we are expecting a better 2H overall result over the 1H due to a larger revenue increase. We expect the full year capex to remain roughly in line with depreciation of $7 Million. We see Decmil’s balance sheet as well positioned to continue to invest in growth.

The 1H2014 result is a continuation of the consistently strong cash flow generated at Decmil over the past years. The working capital inflow of the main accounts was $10 Million. This appears to mostly relate to receiving monies that was withheld at the prior reporting period by a major client. The interim dividend was 4.5cps, 100% franked. Overall Earnings Before Interest & Tax (EBIT) margins improved to 14.5%. The increase is attributable to the high margin accommodation village operating at close to capacity. Decmil guided that it has $600 million of revenue in its order book. The increase in the order book is a positive sign we feel as a large chunk relates to government work. Decmil has track record in gaining scope increases on jobs it is working on and has indicated that it has a strong chance to win more lumpy work at Manus Island. Revenue guidance for the 2H was pretty specific in that it has $314 million of secured revenue and that the accommodation village should deliver revenue similar to the 1H. This implies revenue of at least $335 million in the 2H.

Source – Company Reports (1. Excluding gain arising from business combination for comparative period)

Source – Company Reports (1. Excluding gain arising from business combination for comparative period)

Decmil has won two construction contracts for the detention village on Manus Island, totalling $284 million. Decmil indicated that the camps they are building are away from the existing camp and to date they have not been impacted by the issues at the existing camp. It was also indicated that Manus Island scope could be further increased by the government.

The revenue and EBIT of the

construction and engineering division came in at $232 million and $21 million. EBIT margins were 9.2% versus 9.1% at 1H2013 and 9.9% at FY2013. We think the margin decline is mainly due to increasing competition within the infrastructure sector and conservative profit accrual in the early stages of projects partially offset by productivity and overhead improvements. The construction and engineering division was awarded $400 million in new contract and contract extension in 1H2014 with tier1 clients within the resource space as well as with the federal government. The projects highlighted in the construction space include a second contract of $147 million contract on the Manus Island and a $29 million contract for LNG onshore facility construction with Shell.

DCG Daily Chart (Source – Thomson Reuters)

DCG Daily Chart (Source – Thomson Reuters)

|

Price |

Price % Change |

|

Close: |

2.21 (03-Mar-2014) |

3M: |

16.67% |

|

52 Wk High: |

2.70 (10-Sep-2013) |

6M: |

(8.05%) |

|

52 Wk Low: |

1.35 (13-Jun-2013) |

1Y: |

(11.79%) |

|

Dividend |

|

Yield |

5.76 |

FY |

|

|

2.99 |

5yr Av |

|

Payout Ratio |

31.35 |

FY |

|

|

28.09 |

5yr Av |

The revenue and EBIT for the

accommodation division came in at $31 million and $17 million. EBIT margins came in at 53.9% versus 28.9% at 1H2013 and 38.4% at FY2013. EBIT margins were strong owing to a strong occupancy ratio across a diverse customer base, including coal, LNG, rail and port infrastructure. The strong EBIT margin in this division also helped to lift the EBIT margin at the group level as well. The company notes that there are 2100 rooms in total in the Gladstone area and with 1392 rooms the company has a strong position. CY2015 occupancy is showing increased enquiry rates. Decmil is in discussion with multiple potential occupants for the village in CY2015 including Sntos, Origin and BG.

Some of the main risks associated with Decmil are as follows: 1- Decmil is primarily a construction company, leveraged to the resources capex cycle. The volume of work available is subject to wide fluctuations. 2 – Decmil undertakes large projects on a lump sum basis. Should a project go wrong it could materially impact earnings. 3 – Market sentiment towards the mining services sector can swing dramatically, resulting in large share price fluctuations. Mining services share prices are particularly volatile.

|

DCG, AUD Millions |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Total Revenue |

528.8 |

555.6 |

394.2 |

329.0 |

254.9 |

|

Total Operating Expense |

436.6 |

499.6 |

360.9 |

301.8 |

236.7 |

|

Operating Income |

92.2 |

56.0 |

33.3 |

27.2 |

18.3 |

|

Net Income Before Taxes |

92.2 |

56.0 |

33.3 |

27.2 |

18.3 |

|

Provision for Income Taxes |

27.8 |

16.9 |

9.9 |

8.4 |

6.1 |

|

Net Income After Taxes |

64.4 |

39.1 |

23.5 |

18.8 |

12.2 |

The company is increasingly diversified and no longer depends on winning very large contracts. The two Manus Island contracts with the Department of Immigration and Border Protection adds material diversification. There are rising, recurring revenue streams exposed to upstream and downstream LNG. Opportunities for Build-Own-Operate accommodation villages also makes the investment view attractive. Also DCG has a strong balance sheet which allows it to act quickly on opportunities. We will be putting a BUY at the current price of $2.21.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...