Kalkine has a fully transformed New Avatar.

1. Sector Landscape and Outlook

Technological change is the most disruptive force today. Financial sector companies have demonstrated high receptivity towards ground-breaking innovations. Financial Technology, famously referred to as fintech, encompasses any kind of technological advancement that is transforming the traditional methods used in the delivery of financial services.

.png)

Before we understand fintech, it is important that we clearly decipher the industry’s evolution through time.

Evolution of Fintech

Back in the day, the term fintech meant back-end systems of financial institutions. In the pre-financial crisis era, new market entrants found it difficult to break into the financial services industry as the incumbents had an edge in terms of size, large network, client base as well as resources. Today, fintech start-ups have been successful in revolutionising different processes, creating lucrative opportunities.

Fig 3: Fintech Ecosystem.png)

Let’s deep dive to understand the current trends that are taking place in the industry.

Changing Landscape of Payment System: The advent of fintech has revolutionised the way Australians make payments, and the use of electronic payment methods is growing substantially. The shift towards e-payments from cash and cheques has been remarkable over the recent years, as people are seeking novel and more convenient payment solutions.

.png)

Source: Reserve Bank of Australia, AusPayNet, Kalkine

BNPL Transactions Growing Substantially: ‘Buy now, pay later’ or BNPL services have expanded considerably in the recent years, becoming widely accepted by merchants in several retail segments. The popularity of these services is connected with their convenience and characteristic of offering a lower-cost alternative to consumer credit. According to the RBA statistics, the value of BNPL transactions has grown substantially from over $1 billion in 2016-17 to about $6 billion in 2018-19. BNPL service providers have played a significant role in altering the way consumers are making their purchase decisions, especially the millennials.

Neobanks Revolutionising Banking Industry: Supported by the advancement of technology over time, Australians are now conducting a majority of financial transactions via an application on a smartphone. Digital banks or neobanks are giving a fierce competition to the nation’s big four banks, offering higher interest rates and attracting millions of dollars in savings from the customers. A recent report highlighted that the big four banks of Australia had lost around half a billion dollars in saving deposits in just few months, owing to ~16 times higher interest rates offered by neobanks like Judo Bank, Xinja and 86 400. At the time when the official interest rates have dipped down to about 0.75 per cent, these neobanks are offering saving rates of up to 2.25 per cent. To capitalise on the impressive trajectory demonstrated by the digital banks, smart bank Douugh is planning to get listed soon, becoming the first neobank to hit the Australian Stock Exchange (ASX) boards.

Fig 7: Shifting preference towards banking needs.png)

Seeking Cost-Effective Investment Advice? Robo-Advisors can Help You!: Getting a financial advice from a financial planner is sometimes more expensive than the amount an investor intends to invest. In such cases, digital financial advisors can help the customer in availing cost-effective investment management services. Robo-advisors are providing a contemporary way to customers to invest their funds. They operate through a digital platform which collects information about customers’ financial situation and utilizes the data to offer an investment advice, enabling clients to invest their assets efficiently.Since 2014, there has been a proliferation of digital advisory in Australia with an increasing number of existing Australian financial services (AFS) licensees and start-up AFS licensees developing digital advice models. Moreover, the Australian Securities and Investments Commission (ASIC) is also supporting the advancement of a robust and healthy digital advice market in the nation. Significant transition opportunities seem to be visible for robo-advisors in Australia amidst growing competition over pricing and functionality.

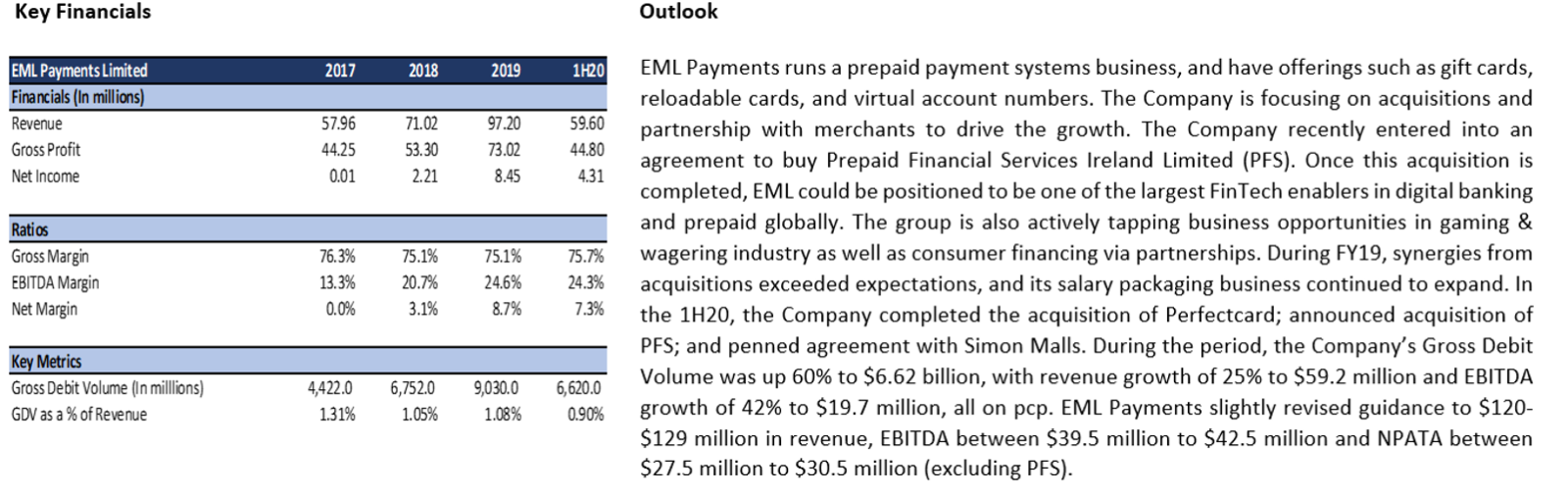

Enterprise Management Systems Simplifying Business Processes: Increasingly, financial institutions are opting for technologies such as cloud solutions, API architectures, and ‘as-a-service’ and ‘as-a-platform’ offerings to simply different processes. Thus, several options exist for enterprise technology vendors. For instance, Australia-based Bravura Solutions provides software solutions and services for the administration of superannuation, pensions, life insurance, investment, private wealth and funds. EML Payments Limited empowers clients to gain control, transparency and flexibility over their payment processes, to attain end-to-end efficiency and security. Increasingly, companies are needing to address high speed marketing of new products, seamless digital experience, ongoing changes in financial services regulation, and pressure to increase operational efficiency. At the backdrop of global economic uncertainty, several CEOs in Australia have narrowed their focus on cost cutting and operational efficiencies. These shifts are presenting a good investment case for enterprise management solution providers as companies like Iress Limited are running automation programs for super funds.

Blockchain Empowering Financial Services Sector: There is growing interest and investment in blockchain as a decentralised, peer-to-peer solution with the potential to deliver significant cost savings. People have lower trust in social and traditional media, and banks to report the truth, protect privacy, and act in the interests of everyday consumer. As per Gartner, Blockchain is expected to generate USD 175 billion in business value per annum by 2025 and ~USD 3 trillion by 2030, with its expanding application in sectors like finance, agriculture, healthcare, real estate, retail, etc. By 2023, blockchain is expected to support movement and tracking of ~USD 2 trillion worth of goods and services annually. For the financial services industry, Deloitte analysts expect blockchain to deliver USD 15–20 billion in annual savings by 2022. Australia’s leading industry for blockchain activities is Financial and Insurance services (See Figure below) and the country has recently rolled out its National Blockchain Roadmap.

Fig 8: Share of Australian blockchain activities by Industry.png)

Source: Department of Industry, Science, Energy and Resources; CSIRO’s Data 61

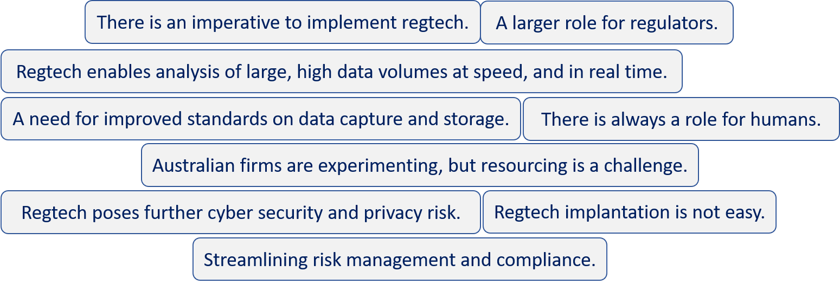

Upcoming Opportunities in Regulatory Technology (Regtech): According to the Australian Securities and Investments Commission (ASIC), there is great potential in regulatory technology (regtech) sector to help businesses establish and maintain a culture of compliance, discover learning opportunities, while also save time and money concerned with regulatory matters. ASIC had received federal government funding in August 2018 for FY 2018–19 and FY 2019–20 to promote development and adoption of regtech solutions for fintech related risk management and compliance problems in Australia. Thanks to this funding, ASIC launched a series of Regtech Initiatives in FY 2018–19.

Fig 9: Regtech Initiatives.png)

Fig 10: Observations of ASIC’s Regtech Initiatives

Having extensively scanned through various sub sectors within the fintech industry, it is quite clear that fintech as an industry is thriving and at a rapid pace. This contemporary sector is drawing the attention of Venture Capitalists across the globe, and a great deal of traction is currently underway. Let’s visit the funding space and gauge the mood.

VC Activities and Mergers & Acquisitions

During the first half of 2019, the Investment in Australian fintech sector dipped, reaching USD 101 million as compared to USD 223 million in the prior corresponding period (pcp) in 2018 at the backdrop of a subdued global fintech investment, which also fell to $ 37.9 billion from $62.8 billion in pcp.

Nevertheless, in the last few years, Australia has seen the creation of a healthy and active fintech sector. As per KPMG’s Pulse of Fintech Report 2019, one of the largest fintech transaction recorded in the first half of 2019 was the Airwallex USD 100 million Series C funding in March 2019, that was also the third biggest deal in Asia during this period. More deals are expected in the upcoming time as Australian SME challenger bank, Judo raised $400 million in August 2019, and the SME lender Prospa Group Limited successfully debuted on the ASX in June 2019.

The largest IPO of the year by market capitalisation in Australia was that of Tyro Payments, a fintech business backed by Tiger Global, TDM Growth Partners and Atlassian co-founder Mike Cannon-Brookes. Tyro raised $287 million and listing market cap of $1.36 billion.

Globally, the incumbent players are allying with fintechs to gain access to the new technologies. In February 2020, Commonwealth Bank of Australia announced its plans to launch 25 new fintech-focussed business in the next five years. The Bank has also confirmed to raise its $ 1 billion annual tech investment budget with the launch of its new platform for allocation of capital and provision of industry expertise to local fintech start-ups. Westpac and National Australia Bank have also established venture capital funds for strategic position in fintech companies.

Key factors driving investment in fintech sector include- Regulatory Technology (RegTech) witnessing a demand spike amid regulatory pressure; Investments in Blockchain, and adoption of Open Banking.

The sector is thriving and thus slew of funding activities are underway. It becomes important for the customers to be protected from undue exploitation and thus a clear understanding of the regulatory landscape becomes imperative.

Regulations around Fintech are Relatively Flexible!

Australia follows the lines of the United States with regard to financial technology innovation, which is considered as top fintech hub across the globe. The fintech businesses in the US are not controlled by any specific state or federal regulator, subjecting new entrants to supervision and regulation by multiple state regulators.

Both the US and Australia share the similarity in terms of evolving fintech regulatory framework, while the former one is quite ahead of the latter.

It is worth stating that the fintech companies are not subject to a similar level of regulation as other traditional financial service providers in Australia. For instance, BNPL player such as Afterpay Limited is not recognised under the nation’s law as credit providers and hence, its services are not included under the NCCPA (National Consumer Credit Protection Act) 2009.

Amidst the current scenario, conventional banks have demanded an elimination of existing no surcharge policies applicable on BNPL players, for creating a level playing field in the domestic payment industry.

Moreover, the regulations surrounding the fintech industry are quiet flexible in Australia to stimulate innovation. On the one hand, ASIC’s Innovation Hub is supporting eligible fintech startups receive informal assistance as they navigate nation’s financial regulatory system, while on the other hand, Australian Prudential Regulation Authority (APRA) is in the process of developing its own approach to regulate fintech businesses in Australia.

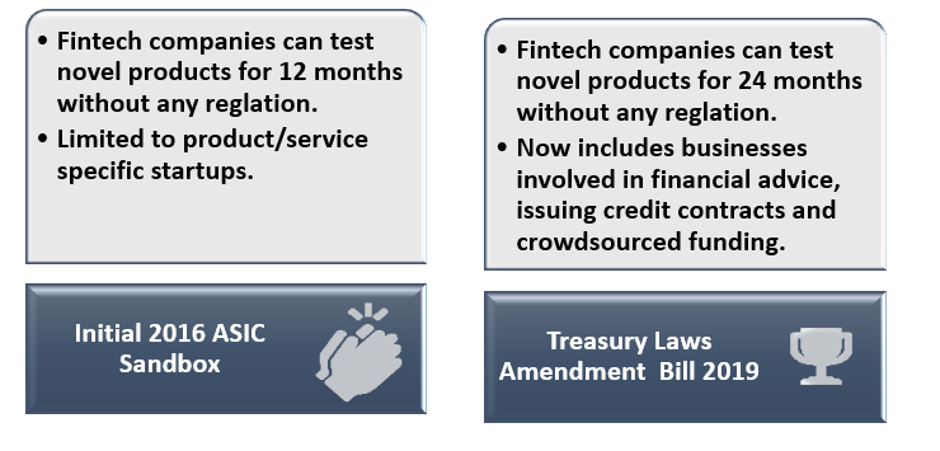

Notably, the Australian government is leaving no stone unturned to reinforce the regulatory framework of fintech companies. The government has recently passed Treasury Laws Amendment Bill 2019, expanding the time span fintech companies can spend in a regulatory sandbox, thereby enhancing the scope of firms that are permitted in.

Fig 11: Key Developments

The Government’s across the world and more so in Australia are focused towards job creation. Let’s have a quick look at the various initiatives taken by the Government to aid this burgeoning industry.

Initiatives for Fintech Sector

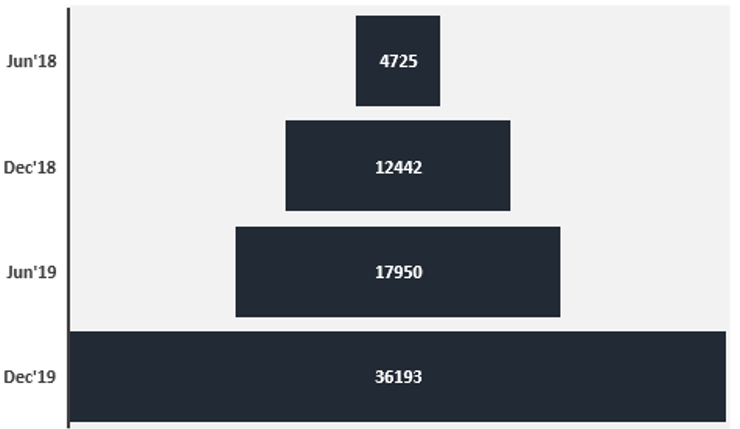

Numerous policy initiatives have been set in place in Australia to push the fintech sector realize its potential. From launching an ASIC regulatory sandbox in 2016 to introducing a New Payments Platform (NPP) in 2018, the government and regulators have continued to explore a broad range of potential growth initiatives for the fintech sector.

Figure 12: Number of NPP transactions (‘000)

Source: RBA, Kalkine

Moreover, the Australian Competition and Consumer Commission’s (ACCC) recent open banking initiative is expected to support fintech firms to enable access to customer banking data using an Application Program Interface (API). ACCC’s open banking regime, which will take effect from July 2020, will allow accredited start-ups obtain customer data from banks through a secure channel after customer’s consent. It is expected to open a wide range of market opportunities for the fintech sector, which will be able to offer potentially better deals to customers.

Is Fintech Sector Facing a Headwind in Australia?

While the number of fintech players is growing quickly in Australia amidst favorable market opportunities, worries over anti-competitive conduct from some of the incumbent banks do exists. Australian fintech entities have recently approached regulators and government to come up with new laws to restrain well-known banks from indulging in anti-competitive practices.

In the BNPL sector, the RBA may intervene and take policy action over service providers preventing retailers from passing surcharge costs on to consumers. If retailers begin to add surcharges on BNPL-backed orders, the cost of each purchase would rise for consumers using BNPL. This could turn out to be a risk for BNPL service providers, like Afterpay, who believes that the RBA’s move could stifle innovation in the sector and reduce competition.

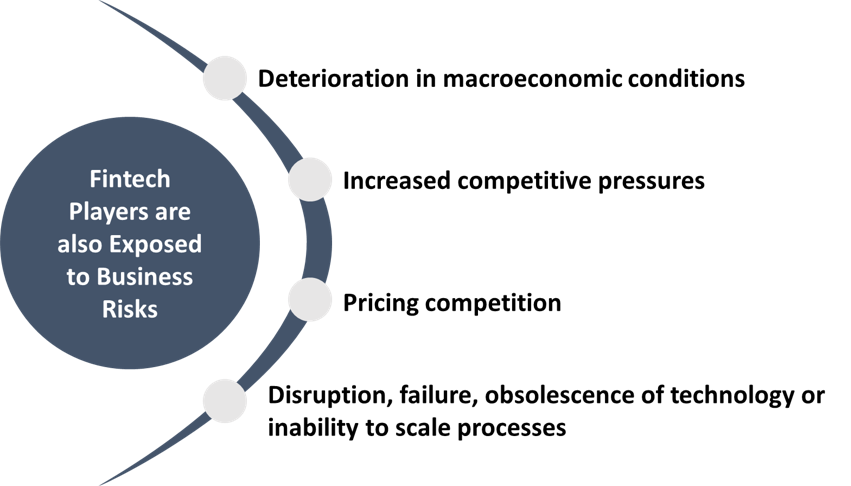

Fig 13: Key Risks

Interestingly, Fintech sector is offering huge investment opportunities in companies that provide enterprise management services, platform services, automation etc. to other financial services business. And, such businesses are quite immune to adverse developments in consumer confidence, economic activity, household debt, household spending, retail trade, inflation, interest rates etc. In the meantime, these adverse developments could take a toll on companies operating in BNPL, payment services, neobanks, etc.

2. Investment Theme and Stocks under Discussion

Following the global stock market turmoil on account of Coronavirus outbreak, most of the stocks recently took a beating. Despite the current challenging market conditions, we believe that the outlook for fintech stocks are positive in the medium to long run and current downtrend in the stock prices provides a decent opportunity for accumulation.

After understanding the sector, let’s take a detailed look at five stocks in terms of their outlook and performance. To gauge the potential of the fintech stocks, we have followed the market multiple approach and used ‘Price/Sales’ multiple. The peer group for each stock has been shortlisted based on their respective market capitalisation.

Fig 14: Relative price performance of the stocks under discussion

Comparative Price Chart (Source: Thomson Reuters)

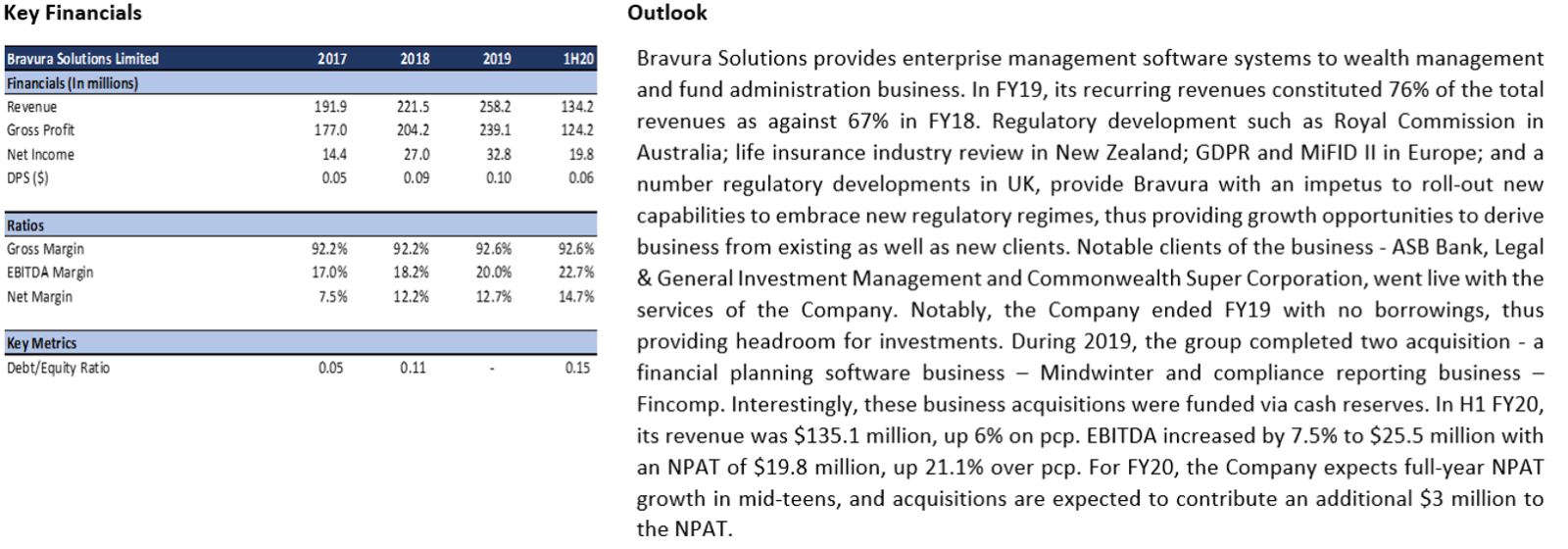

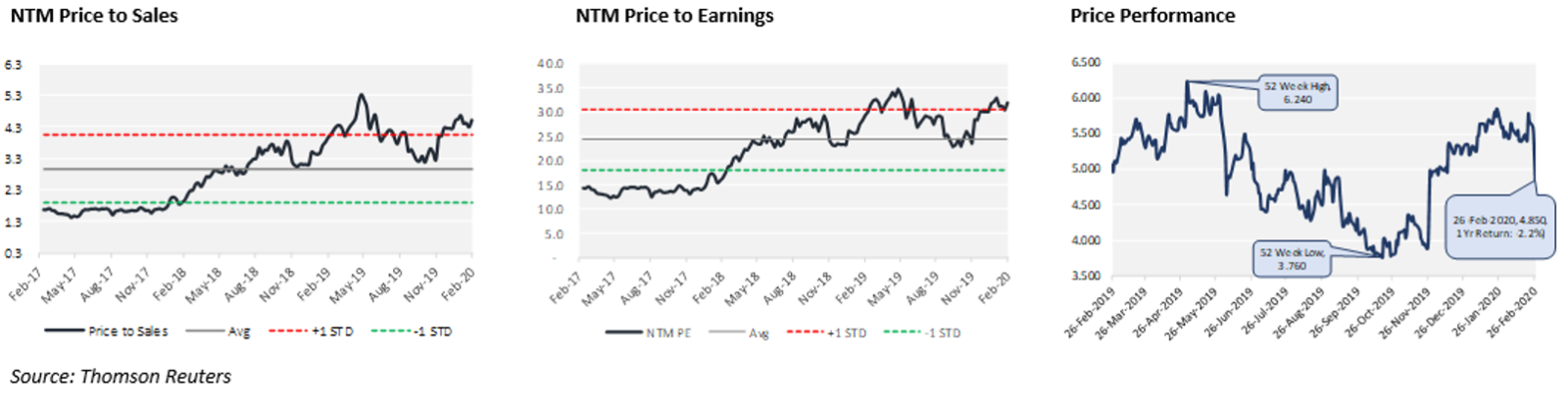

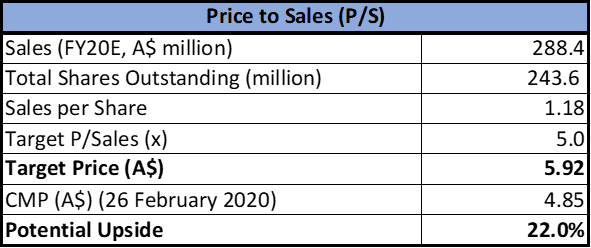

(1) ASX: BVS (BRAVURA SOLUTIONS LIMITED)

(Recommendation: Buy, Potential Upside: 22%)

Valuation

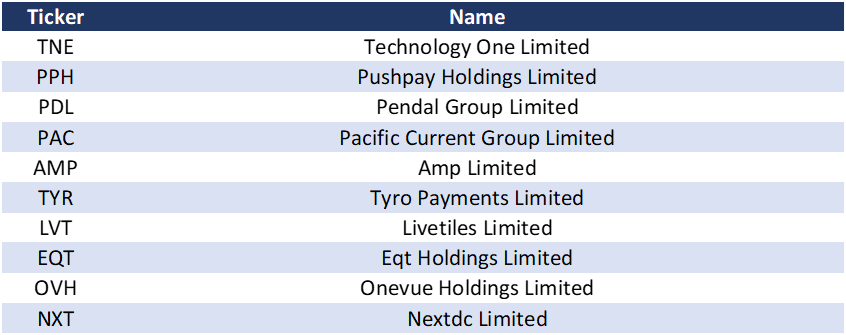

Our valuation model suggests that stock has a potential upside of ~22% on 26 February 2020 closing price. We have taken TNE, EML and PPH as peer group for comparison purpose. Although, the stock witnessed a correction in the last few days; we believe this provides an opportunity to accumulate more. The group recently reported a decent 1H20 results and the outlook and fundamentals remain strong.

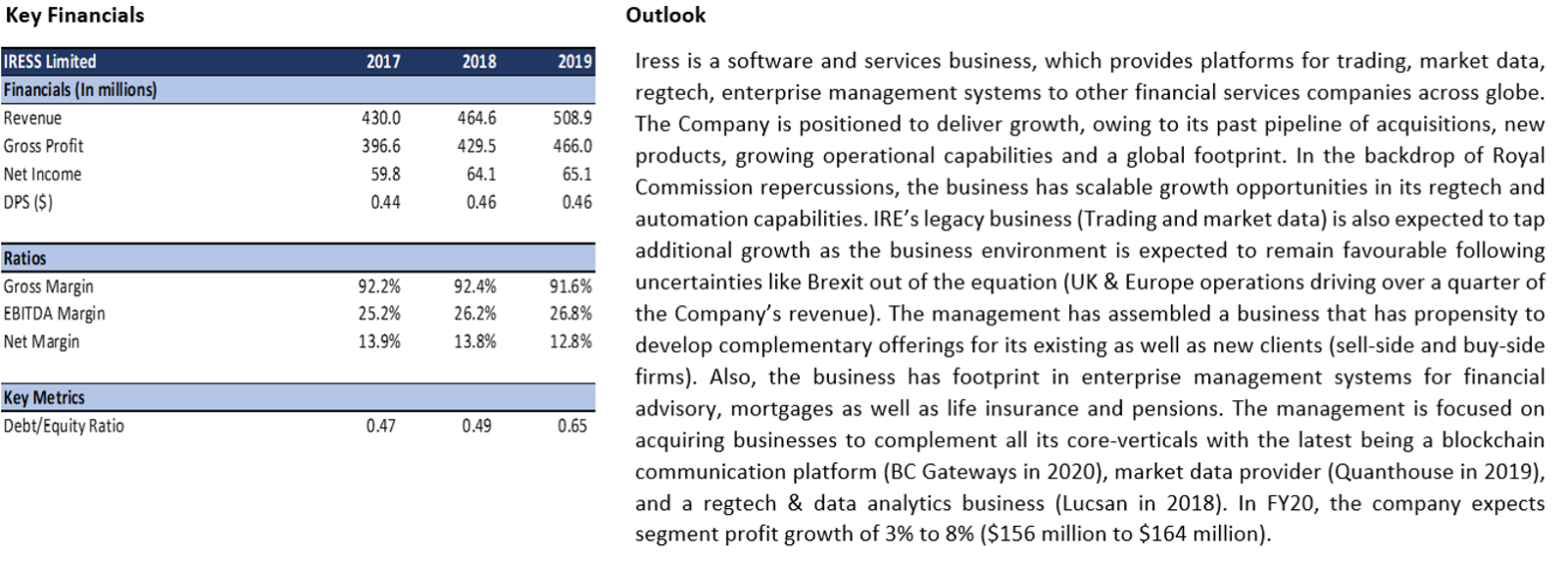

(2) ASX: IRE (IRESS LIMITED)

(Recommendation: Buy, Potential Upside: 15%)

Valuation

Our valuation model suggests that stock has a potential upside of ~15% on 26 February 2020 closing price. We have taken TYR, EML and BVS as peer group for comparison purpose. Although, the stock witnessed a correction in the last few days; we believe this provides an opportunity to accumulate more. The group is focusing on inorganic methods (acquisitions) to drive the growth which is expected to help the company to achieve better financial numbers on account of synergies achieved.

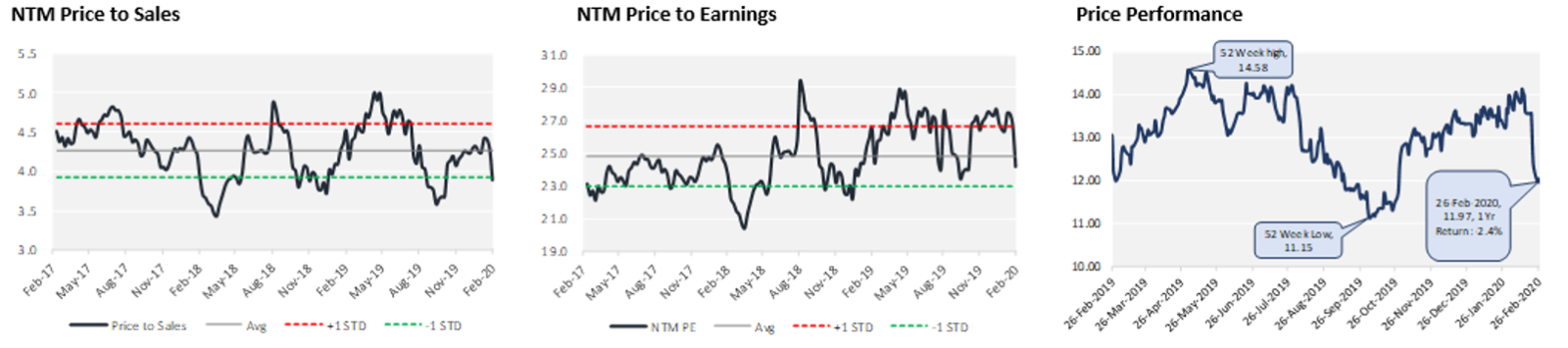

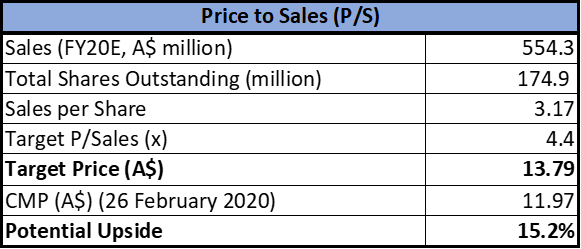

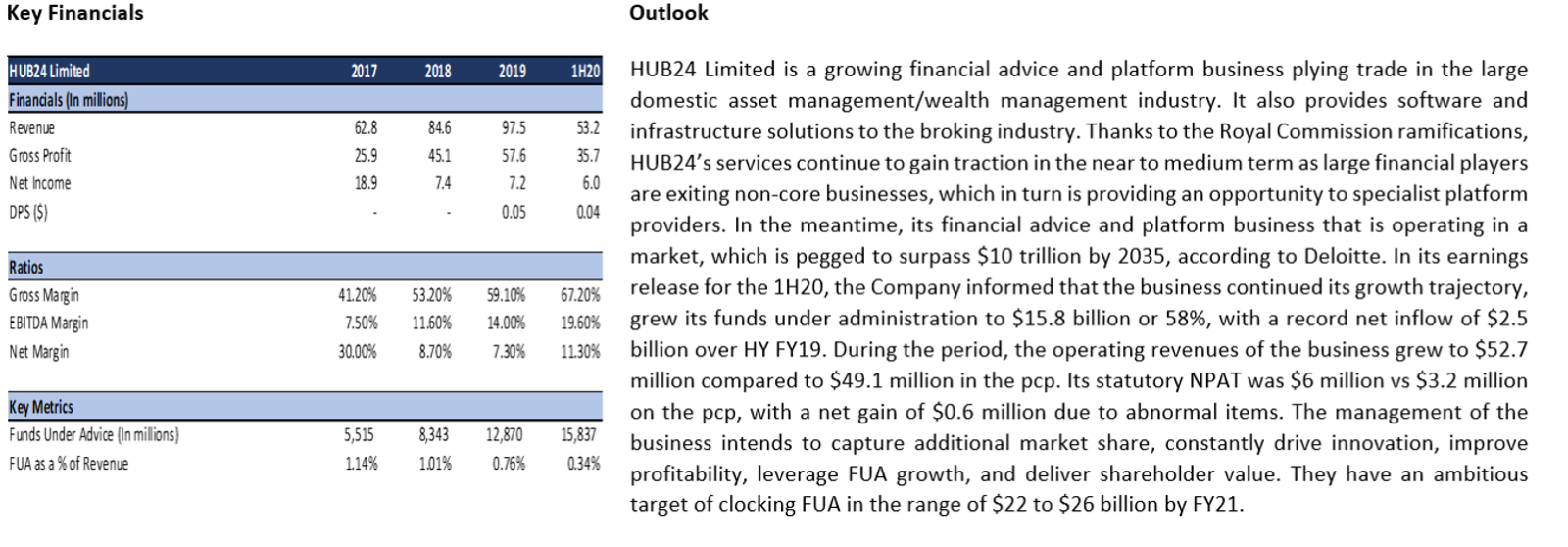

(3) ASX: HUB (HUB24 LIMITED)

(Recommendation: Buy, Potential Upside: 11%)

Valuation

Our valuation model suggests that stock has a potential upside of ~11% on 26 February 2020 closing price. We have taken PDL, PAC and AMP as peer group for comparison purpose. The group has reported a decent half yearly result and guided for a strong second half. Also, recent development such as Royal Commission repercussion is expected to provide an opportunity to drive the business.

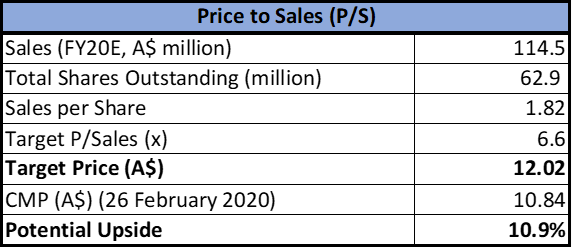

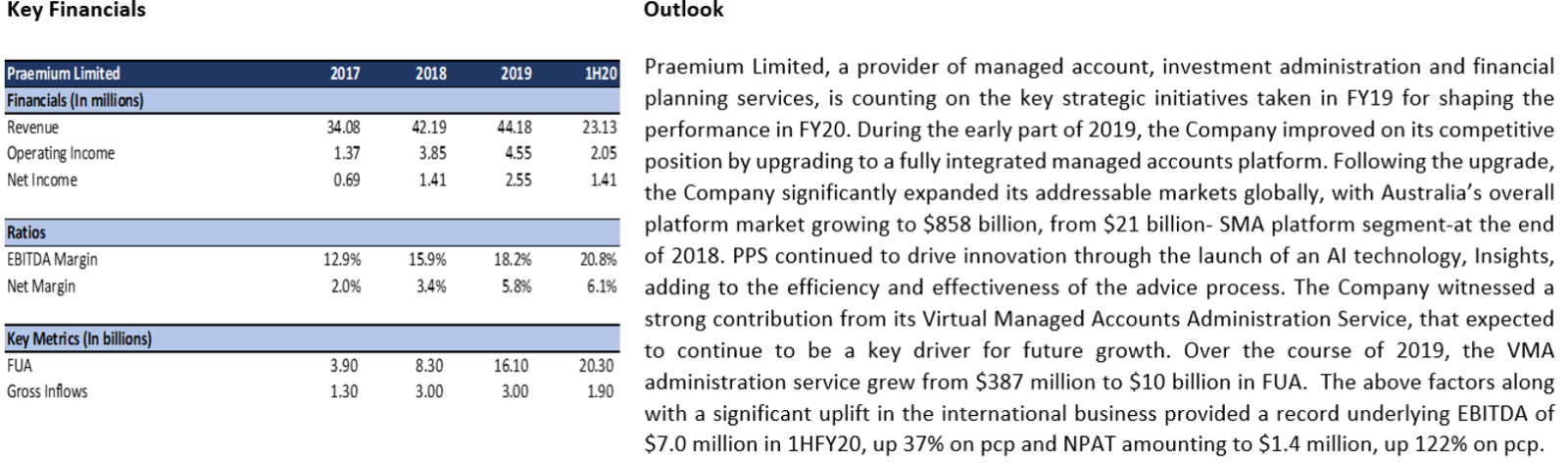

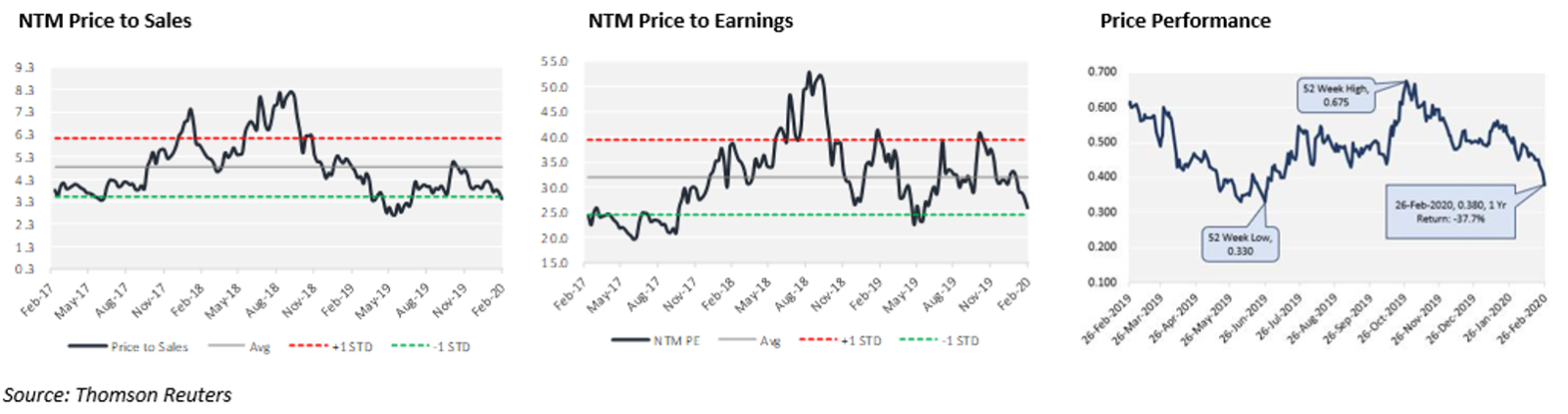

(4) ASX: PPS (PRAEMIUM LIMITED)

(Recommendation: Buy, Potential Upside: 16%)

Valuation

Our valuation model suggests that stock has a potential upside of ~16% on 26 February 2020 closing price. We have taken LVT, EQT and OVH as peer group for comparison purpose. We believe continuous strategic initiatives to strengthen the competitive position and investment in technology are key positives.

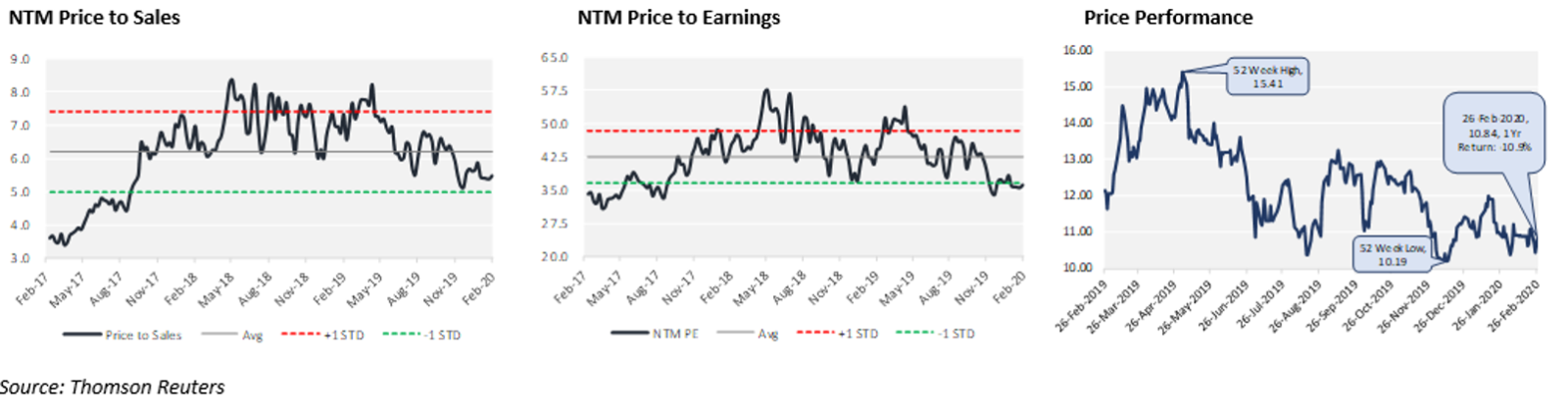

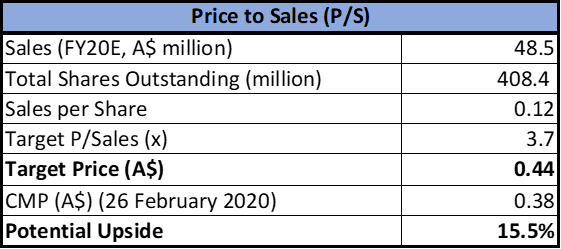

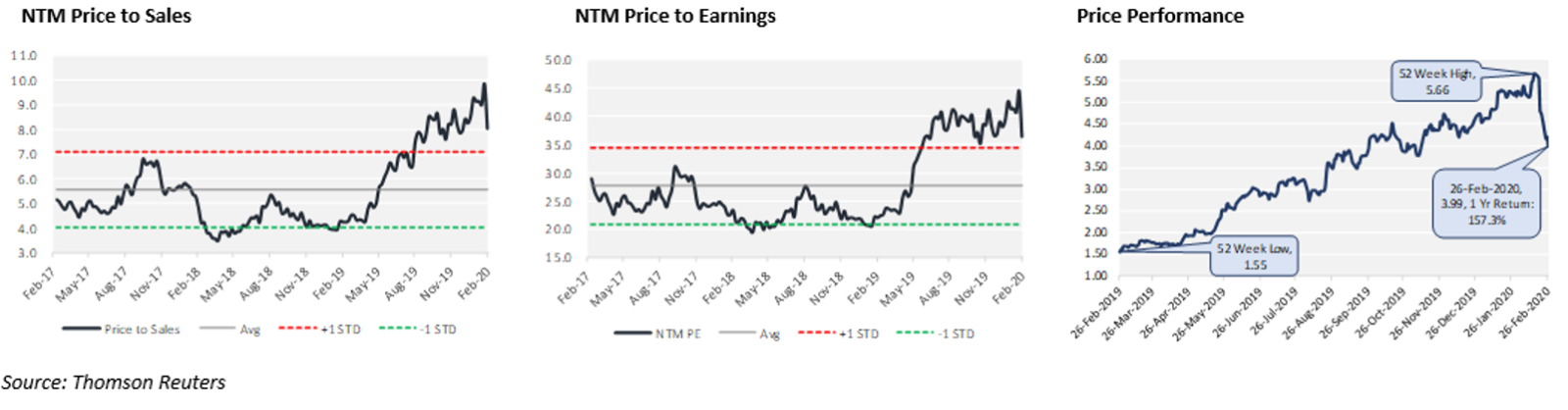

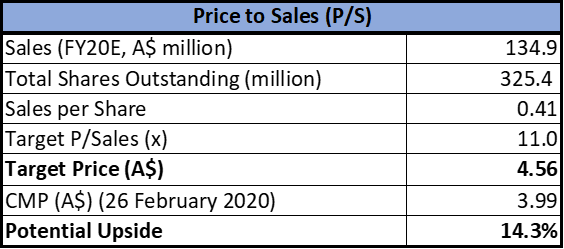

(5) ASX: EML (EML PAYMENTS LIMITED)

(Recommendation: Hold, Potential Upside: 14%)

Valuation

Our valuation model suggests that stock has a potential upside of ~14% on 26 February 2020 closing price. We have taken TYR, NXT and PPH as peer group for comparison purpose. Although the group has recently reported a decent result and expected acquisition further strengthen the outlook; we believe all the positive are accounted for in the current price levels.

Note: All the recommendations and the calculations are based on the closing price of 26 February 2020. The financial information has been retrieved from the respective company’s website and Thomson Reuters.

Following table represents the companies used for peer group selection.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...