Kalkine has a fully transformed New Avatar.

The trial and tribulations appear to continue for HYQvia, Baxter’s product that combines plasma-derived 10% immunoglobulin with recombinant human hyaluronidase for subcutaneous (sub-Q) administration in patients with primary immunodeficiency disease as FDA recently requested an additional three months to review safety data and called upon the Blood Products Advisory Committee to discuss the application. While we view continued delays of HyQvia as positive for CSL’s ongoing dominance of the estimated A$1.6bn+ sub-Q space with Hizentra, we believe HyQvia is approvable and view its differentiated therapeutic profile (eg faster infusion rates, fewer injections, improved tolerability and possible health savings) as a competitive threat.

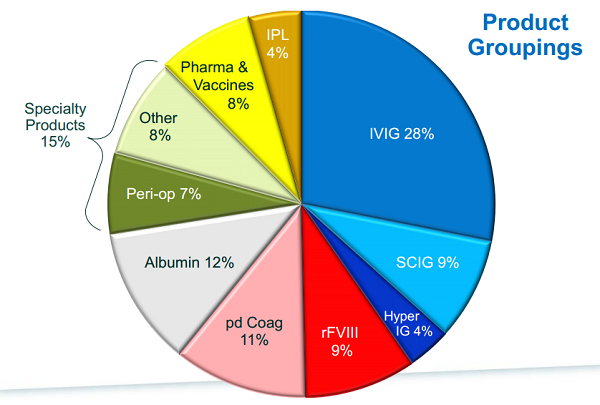

Immunoglobulins Sales ( Source - company Reports)

Subcutaneous (sub-Q) Ig- What is it?

Subcutaneous (sub-Q) administration of immunoglobulin (Ig) relies on drug delivery via injections under the skin, compared to traditional intravenous administration where Ig is given via a vein. We believe sub-Q differentiation stems from its potential for self-administration in the home setting compared to IVIg, which must be administered by a registered nurse, usually at a hospital. However, the major concern with sub-Q administration is the poor bio-availability (ie ability to enter the systemic circulation). Thus, significant swelling occurs at the site of injection resulting in significantly slower infusion rates and reduced bioavailability of the Ig as it slowly works its way through the tissue. These draw backs ultimately mean patients need to infuse more regularly (one-to-three times per week) at multiple injections sites.

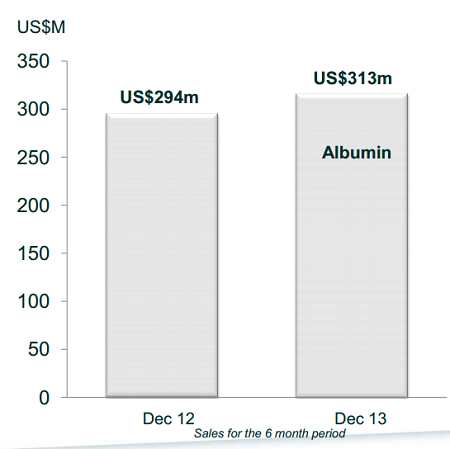

Albumin Sales (Source - Company Reports)

CSL is the dominant player in the sub-Q Ig space holding an estimated 65% share of a US$1.6bn+ market. While major competitors entered in 2011 with 10% concentrated products. CSL has had a presence in the US for seven years and in other jurisdictions for more than 10 years with Vivaglobin, a 16% Ig formulation. CSL improved upon its sub-Q franchise with the March 2010 launch of Hizentra, a 20% Ig formulation that offered greater convenience than Vivaglobin (11% shorter infusion times), enhanced flexibility with room temperature stability, improved yields and a higher price point. The benefits of transitioning patients to Hizentra from Vivaglobin are clearly seen in FY11-12 sales growth rates, with sales slowing into FY13 as the mix shift ended.

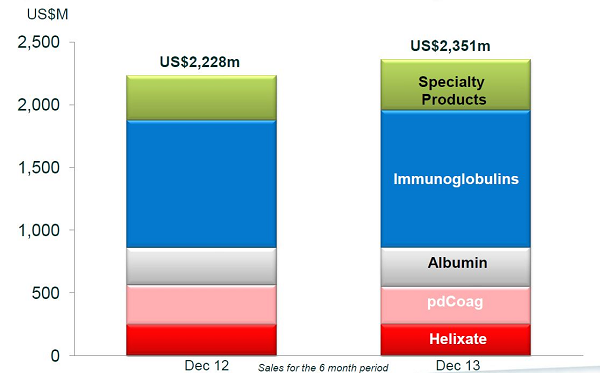

CSL Behring Product Sales (Source - Company Reports)

We estimate the current targeted market of primary immunodeficiency (PID) patients comprises 25% of the total Ig users. Out of these patients, we believe 60% use Ig chronically and 50% of those would be candidates for sub-Q use. Thus, about 7.5% of the total IVIg patient population would be amenable to sub-Q therapy. Given an estimated 123 tonnes of Ig solid in 2014, split between the US and ROW (45/55), and Hizentra pricing we estimate global market at US$1.6bn growing toUS$2.3bn by 2019.

CSL Daily Chart (Source - Thomson Reuters)

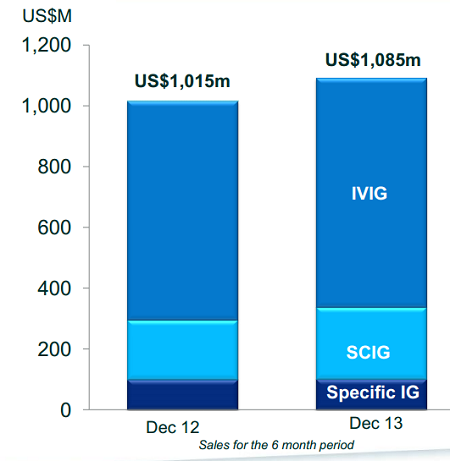

CSL Behring sales of US$2.4 billion grew 6% in constant currency terms when compared to the prior comparable period. Immunoglobulin, Albumin and specialty products sales showed strong sales growth during the first half. Haemophilia product sales of US$550 million declined 4% in constant currency terms. Humate sales in the U.S. were strong arising from increased usage in surgery. However, this was offset by the conclusion of a number of treatment programs for immune tolerance therapy patients. In addition the timing of plasma derived haemophilia product sales in tender markets can be uneven.

CSL holds 30% of the global open market plasma supply. The industry has consolidated to 3 major fractionators controlling 85% of the open market, consolidation appears to have reduced duration and severity of the supply demand cycles. With R&D investment, CSL medium term outlook is encouraging: recombinant portfolio to be commercialized from 2016, with CSL being able to participate in total market value of US$5.2bn. Continued robust global demand growth at high single digit; but for major commercial fractionators demand is more than 10%. Demand for Albumin remains robust.

We maintain that CSL's track record in unlocking the value in its R&D portfolio is key to valuation upside. We underline CSL’s strength in the form of new product label and geographical extensions as well as positive momentum in its Breakthrough Medicines portfolio with the progression of CSL112 (which has a significant addressable patient population), we retain our BUY recommendation on the stock at the current price of $66.55.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Please wait processing your request...

Please wait processing your request...