CompanyOverview – CSL Limited develops, manufactures and markets human and veterinary pharmaceutical and diagnostic products derived from human plasma. The company markets its products - human and animal vaccines, antibiotics and anticoagulants – nationally and internationally. Recently the company has acquired Telecris in the US subject to regulatory approval. The Company is engaged in the research, development, manufacture, marketing and distribution of biopharmaceutical and allied products. The Company operates in three segments: CSL Behring, Intellectual Property Licensing and Other Human Health. CSL Behring manufactures markets and develops plasma products. Intellectual Property Licensing includes revenue and associated expenses from the licensing of Intellectual Property generated by the Group to unrelated third parties. Other Human Health consists of CSL Bio plasma and CSL Biotherapies. These businesses manufacture and distribute bio therapeutic products. It operates in four geographic areas: Australia, the United States of America, Switzerland, and Germany. Its subsidiaries include CSL Employee Share Trust, CSL Biotherapies Pty Ltd, Cervax Pty Ltd, CSL Biotherapies (NZ) Limited, Iscotec AB, Zenyth Therapeutics Pty Ltd, CSL International Pty Ltd and CSL Finance Pty Ltd.

Analysis– The well flagged and widely expected FDA green light for the use of plasma derived Kcentra (Prothrombin Complex Concentrate – PCC) for the reversal of the blood thinning effects of Warfarin in patients undergoing urgent surgery/invasive procedures. The approval was based on 168 patient clinical trial that showed Kcentra was superior to plasma, the current standard of care in restoring bleeding control, increasing major clotting factors with less volume, lowering infusion time and had an equivalent safety profile.

We view the expanded use of Kcentra as incremental positive as it follows on the heel of US approval for use in patients with major bleeding favorably positioning the brand as the only major PCC. We estimate the total US market opportunity at US$100m+ helping to support management’s 15% growth expectations in the specialty products division, with contribution from major bleeds and urgent surgery/invasive procedures. However while clinical data is supportive across both indications, we view incremental operating income of US$70m+ across the franchise as likely to be gained over time as broad based adoption requires shift in the current treatment mindset. Sales of CSL's specialty blood products rose by 16% in constant currency terms to US$403 million during the 1H14 due to treatments like Kcentra.

We think that CSL’s top line will continue to be supported by strength in Immunoglobulin (IG) and Albumin demand. Immunoglobulin, or Ig, is a component of healthy human blood plasma. Some people are born with low or absent levels of Ig in their blood, or with an immune system that does not function properly. Such a condition makes fighting off common germs and infections extremely difficult – if not impossible. Immunoglobulin therapy replaces Ig that is present in an insufficient quantity. Going forward delays around Baxter International’s (CSL’s main competitor) Sanquin contract providing extra capacity will underpin CSL’s top line growth for approximately 2 more years at above market growth. The approval of HIZENTRA, for a biweekly dosage in September 2013 also offers further patient convenience and support to growth. Further we believe that Albumin sales will have benefited from strong demand and pricing out of china.

We forecast double digit growth for specialty products driven by the success of BERINERT, which in April 2013 received European Medicines association (EMA) approval for use in short term intravenous prophylactic treatment of both adults and children. We are also encouraged by KCENTRA’s (also marketed as BERIPLEX) granting of orphan drug status in December 2013. This designation is for the urgent reversal of Warfarin in adults requiring surgery and expect CY14 will see hospitals around the US build inventory in KCENTRA.

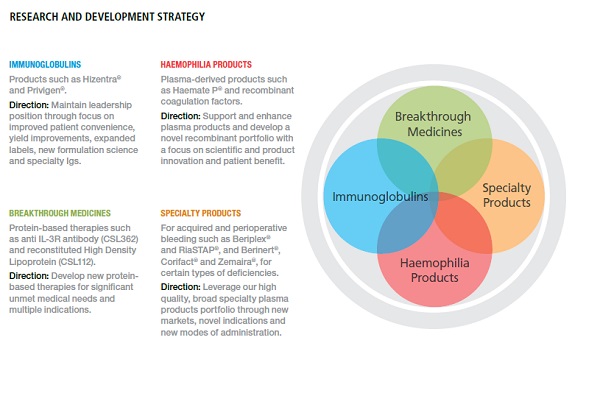

CSL’s R&D Strategy (Source – Company Reports)

We maintain that CSL’s track record in unlocking the value in its R&D portfolio is key to the valuation upside. With management’s briefing underlining this strength in the form of new product label and geographical extensions as well as positive momentum in its breakthrough medicines portfolio with the progression of CSL112 which has significant addressable patient population.

In regards to the recent result released sales of $2.9b was above market expectations. The highlight of the 1H14 result was an improvement in margins where underlying EBIT margin expanded 160 basis points to 32%. Reported net profit after tax of $646m was above our expectations with a lower than expected tax rate helping to boost the underlying operating result.

Despite the difficult environment there was a solid lift in group margins after stripping out the impact of the class action settlement and the one off payment from Janssen Biotech. Underlying EBIT margins expanded 160 basis points in 1H14 which we believe largely reflected increased scale and efficiency at the core plasma and the benefit from the strong growth of the high margin specialty products. This improvement came despite a large lift in R&D allocation relative to the previous corresponding period and lower average prices for IG due the unfavorable geographic mix.

IG volumes were up 10% suggesting CSL continues to gain share in this space thanks to its leading position with Hizentra. IG revenues were only up 8% due to stronger sales in the lower priced European markets. Management has reported that CSL has not lost any share in the better priced US market. Market growth is reportedly in the high single digits.

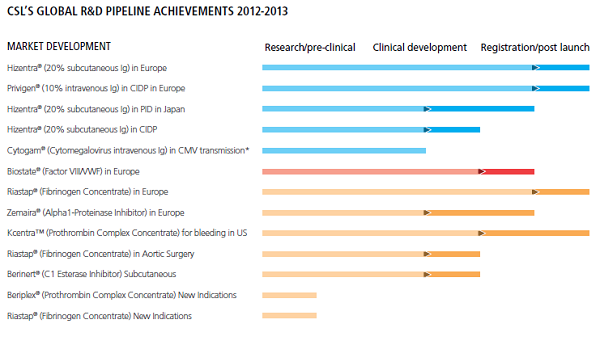

CSL’s Global R&D Pipeline (Source – Company Reports)

|

CSL (Millions, US Dollars) |

2013 |

2012 |

2011 |

2010 |

2009 |

|

Total Revenue |

5,129.5 |

4,813.6 |

4,262.3 |

4,056.5 |

3,690.7 |

|

Gross Profit |

2,559.0 |

2,226.5 |

2,030.4 |

1,998.8 |

1,633.6 |

|

Total Operating Expense |

3,662.1 |

3,543.6 |

3,071.8 |

2,842.3 |

2,684.0 |

|

Operating Income |

1,467.4 |

1,270.0 |

1,190.5 |

1,214.1 |

1,006.7 |

|

Net Income After Taxes |

1,216.3 |

1,023.9 |

936.5 |

926.7 |

842.2 |

Albumin sales were up 7%. Chinese sales were up 25% along with that US and European demand remained solid as clinicians switched away from hydroxyethyl starch solution to albumin. Management noted it was struggling to keep up with demand, especially in china. While this will be alleviated as the new albumin capacity is coming on line, total output is limited by the growth in the group’s IG sales.

Source - Thomson Reuters

Specialty products outlook looks solid, sales were up 16%. CSL cited strong demand for K-centra in the US, following its approval and launch, Berinert self-administration label is driving new patient take up and the launch of its new testing kits driving new patient growth in ALPHA1. In an effort to highlight the growth potential of this segment CSL provides estimates for the current potential markets for its specialty products totaling $2.1b compared to its current sales of $770m. Management reiterated it has continued its ongoing capacity expansion plans reflecting its confidence in the market fundamentals. At the end of FY13 CSL had 80 centres in the US, 8 in Germany and has opened 8 new centres in the US resulting in a global total of 96. We will be putting a

BUY recommendation on CSL at the current price of $69.20.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...