Kalkine has a fully transformed New Avatar.

I. Sector landscape and outlook

Crude oil, the World’s largest commodity, is the driving force behind the global economy. Karl Benz through the first gasoline car in 1885 and later by the people’s car “Model T” by Henry Ford in 1908, established oil as the director of global mobility.

Amid the pandemic, the Crude oil went through the roughest patches, beginning with the demand shock, rising inventory, oil price war, Sub-zero oil prices and supply cuts and most recently the recovery to USD40 levels. We have indeed seen it all. We believe Crude Oil industry is essential to be talked about, with demand, supply, prices trends and future anticipations as well as the innate issues of the sector.

Figure 1) Story of Crude oil in 2020.png)

Source: Kalkine Secondary Research

For the same, Kalkine has come up with this sector report where we have exhaustively examined and discussed the intricacies and dynamics of the Global and Australian crude oil industry to understand the pricing and future outlook to demystify the performance of the companies operating within the industry.

Crude Oil Bloodbath: Soon after the onset of 2020, the effect of coronavirus began to impact the oil demand in China following the extensive lockdowns. By mid-March, the outbreak made it to every continent and was responded by extensive quarantine measures and travel ban, limiting Industrial activity and transportation activity of more than half of the global population. Between 6 March and 31 March, prices fell by 53 per cent, on expectations that Russia, Saudi Arabia and the rest of OPEC+ would increase output amid dwindling consumption.

Oil Price War: The bugle of cataclysmic Oil bloodbath: The demand for oil supply cuts to manage the supply glut situation were unattended until March 6, when the OPEC+ came together to resolve the issue but failed to reach to a consensus to continue the supply cut already in place. Saudi Arabia declared an oil price war by increasing the oil production to around 12.5 million barrels per day levels, an increase of almost 1.5 million barrels per day to target Russia, which had earlier declined to cut the supply.

Rising Oil Stocks & Supply Glut, Crippling Crude Oil: The US government continued to buy domestic crude oil to maintain the demand levels and support the Texas and North Dakota oil players, which in the absence of demand resulted in filling of the nation’s stocks to a higher than normal proportions. The US crude oil benchmark Western Texas Intermediate (WTI) futures prices fell to the 18 year low of USD20.37 a barrel in the absence of demand and rising stocks on 18 March 2020. Oil prices declined over 53% amid the geopolitical drama while the demand further slid away.

On 12 April finally, a deal to cut the OPEC+ production by 23% with Saudi Arabia and Russia taking the cut of around 2.5MMb/d each during May to June 2020 was agreed upon.

The delayed action on the supply cut at Cushing and rising oil stocks in absence of buyers resulted in the WTI crude oil future contract for April (expiring on 21 April 2020) dip to the negative USD 35 – USD 40 ranges on 20 April. In April, the global supply exceeded the demand by as much as 25 million barrels.

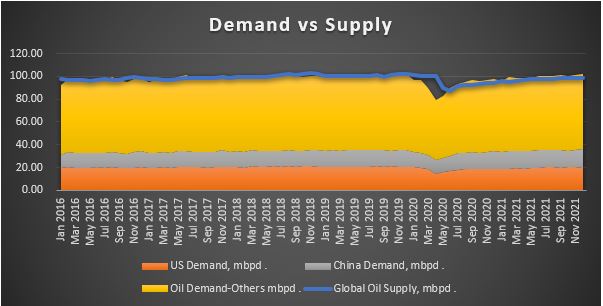

Figure 2) Crude Oil Demand vs Supply

Source: US IEA

Gradual Recovery Path for Crude Oil Ahead

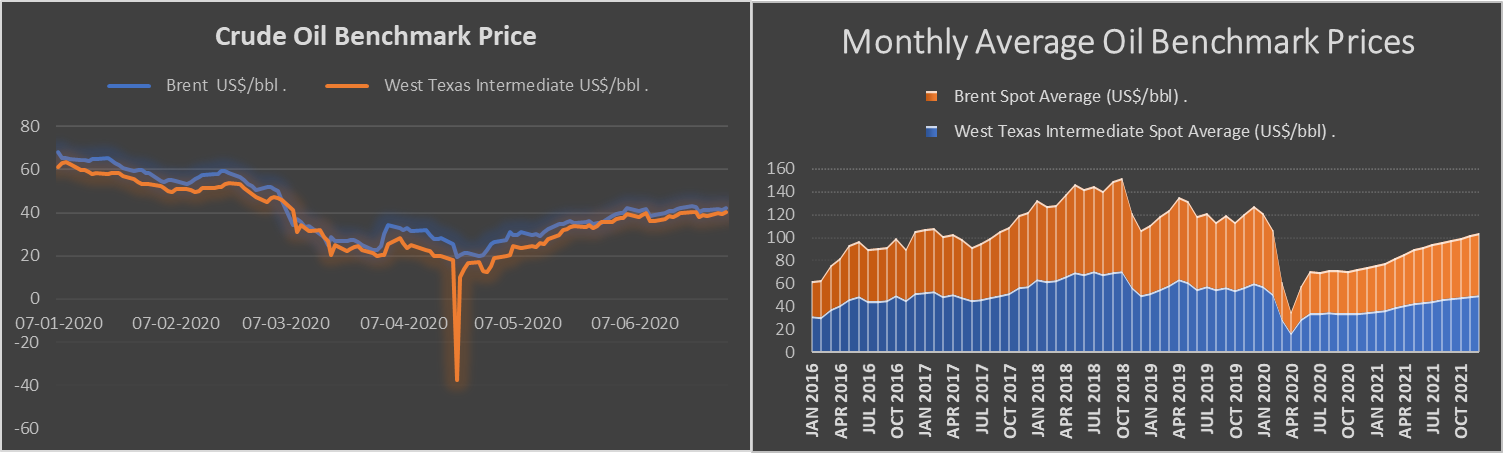

The supply cuts were further extended by OPEC+ on 6 June 2020 until the end of July. The reopening of global economies and extension of OPEC+ supply cut has boosted the Brent oil prices to recover by ~71% from 1 May to 16 June to the current levels. Although the crude oil prices still remain well below the 2015-19 period, a gradual recovery can be expected upon the commencement of transportation and international travel. While the oil demand to reach previous levels may take some time, the crude oil prices are anticipated to gain here on, with the increase in demand across the globe. As per the Australian Department of Industry, Innovation and Science, the Crude Oil prices are anticipated to average around USD43 a barrel in the September quarter and USD44 in the December quarter of 2020.

Figure 3) Crude Oil Benchmark Price (L) Future Price Projections (R)

Having understood the issues plagued by the crude oil industry, let us now shift our focus towards the demand side of the equation.

The Messiah- Global Demand

The global oil demand is anticipated to average at 91 million barrels a day for 2020, registering a decline of 9.2%. The decrease in demand is attributable to both demand generators, the transportation and the industrial segments.

US Showing Signs of Improvements, Demand Increasing from the April Lows: Amid extensive lockdown and travel ban, demand declined by 50% across several parts of the world. In early April, The US Crude Oil Demand fell to 14.29 million tonnes, a decrease of over 30% against pre-COVID levels and the lowest since 1990. The decline in demand saw the US refiners, including Marathon (the largest refiner in the US) to cut the refining throughputs. However, a recovery has been seen in the past months as the ISM Manufacturing PMI levels for the US jumped to 52.6 in June 2020 from 43.1 & 41.5 in May and April, respectively. As per the US IEA, demand in May from the US improved to 16.08 million barrels.

China achieves 90% Demand Recovery: In May 2020, China imported record levels of crude oil at 11.34 million barrels a day, an increase of 160,000 barrels a day against April. By May, China achieved a demand recovery of 90%. The easing travel restrictions and behemoth stimulus package is assisting the world’s second largest crude oil consumer in accelerating its recovery. Similar recovery trends can be expected from other regions in Europe and Asia where the quarantine measures have been eased, and industrial activities are gaining pace.

With demand being tepid, let us gauge through the supply side of the story.

Global Supply under Lens

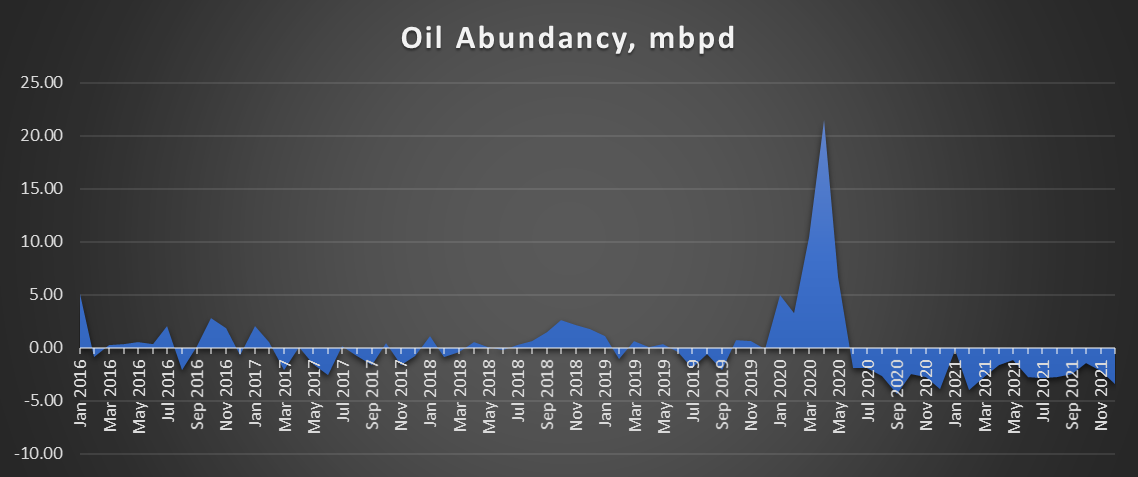

The US EIA anticipates the supply to average at 92.6 million barrels a day, achieving an average of 1.6 million barrels oil abundancy against the average demand levels in 2020. The supply would be hit substantially by almost 7.6 million barrels per day against 2019 levels. As per the Baker Hughes operational oil rig count, only a total of 1083 oil rigs are operational as of 28 June 2020 as against 2217 in the previous year.

Further extension of oil supply cut may be required by the oil producers to keep the oil supply in check. The US EIA believes the global oil supply to average at 92 bpd in the September quarter of 2020.

Figure 4) Crude Oil Abundancy, mbpd

Source: US EIA

Bloodbath Extended to LNG

The LNG sector, which had already been facing the demand decline due to hotter than normal winters in China and Japan faced another big test with the declining crude oil prices. Multiple Chinese and Indian LNG buyers including CNOOC announced force majeure on their supply contracts.

Let us now shift our focus towards the domestic opportunity.

The Australian Opportunity

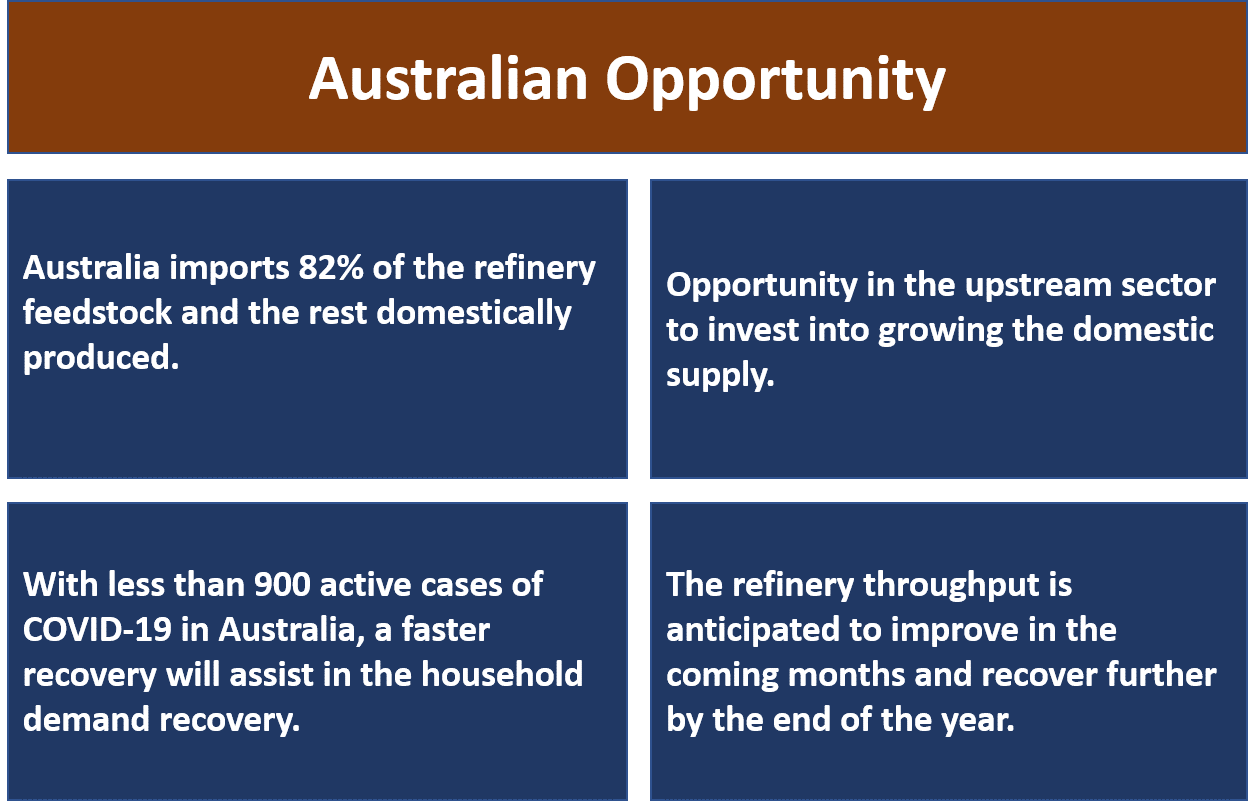

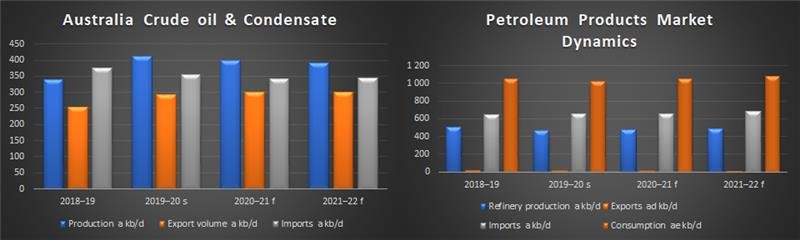

Figure 5) Australian Opportunity

Australia presently imports almost 82% of the refinery feedstock and domestically produced only a meagre 18%. The Australian household demand is anticipated to pose a risk to the existing 4 refineries in the country, but it does pose an opportunity for the nation’s Oil & Gas firms especially the upstream sector to invest into growing the domestic supply. When it comes to Crude Oil, Australia plays the role of a price taker and not a price setter.

In the wake of low household demand, the downstream sector including Caltex Australia refinery has announced the closure of its Brisbane refinery until margins recover. Australia now holds less than 900 active cases of Coronavirus and a sooner recovery would assist in the household demand recovery. The refinery throughput is anticipated to improve in the upcoming months and recover further by the end of the year. Australia consumption is anticipated to recover faster against global peers on the easing of further restrictions in H2, 2020. The travel and aviation demand can be expected only from the domestic or Oceania region and will add substantially to the recovery given the fact that the Australian aviation sector accounted for 15% of total domestic oil consumption in 2019.

During 2019-20, the Australian Crude and condensate production is anticipated to increase to 412,000 barrels a day, a 21% increase due to the commencement of large projects including Woodside petroleum’s Greater Enfield project.

Figure 6) Australia Crude Oil & Condensate (L) Petroleum Products Market dynamics (R)

source: Australia DIIS

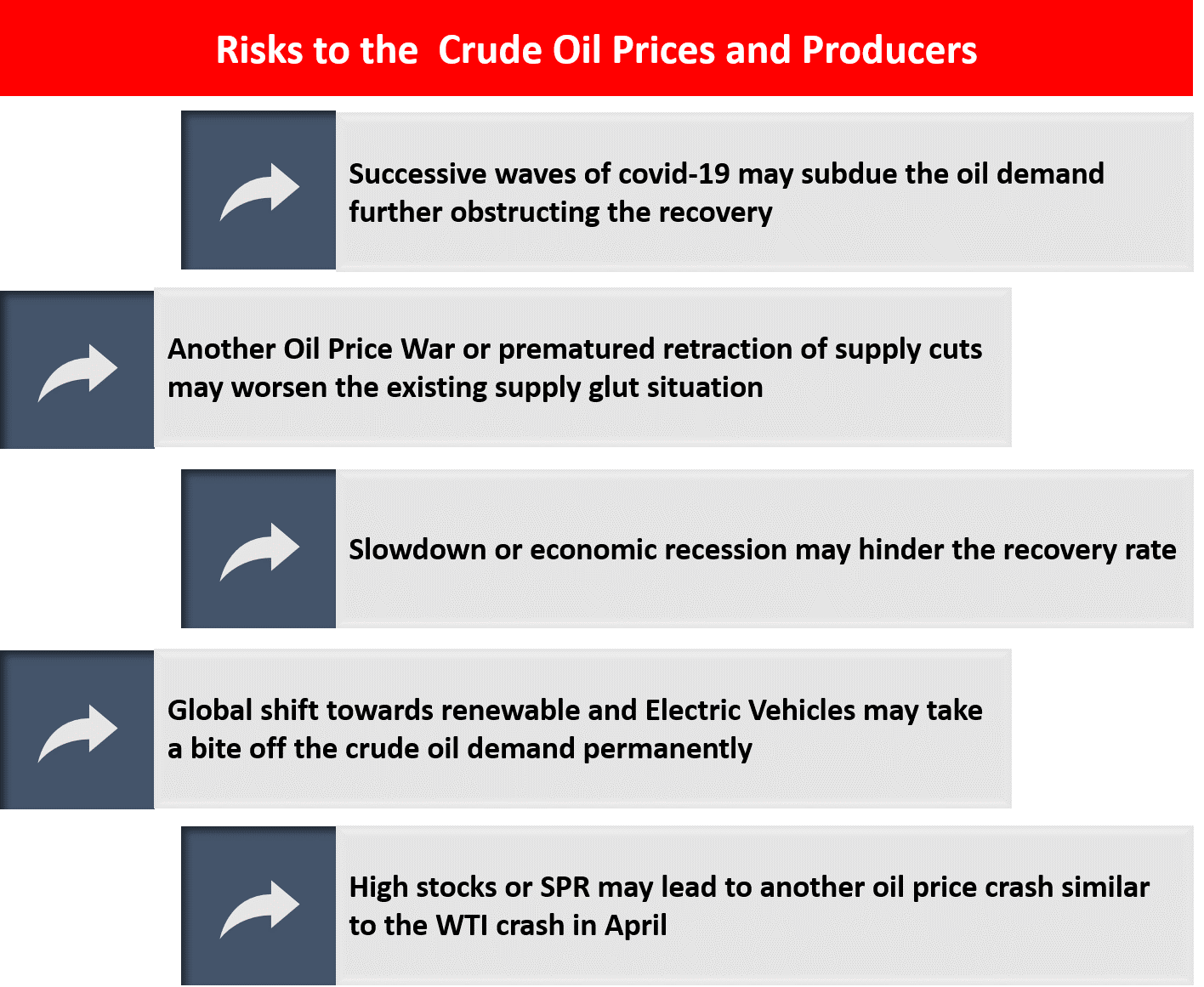

Understanding the risks that the oil sector is exposed to is paramount, let us look at major risks to the sector.

Figure 7) Crude Oil Market Risk

Source: Kalkine Secondary Research

The crude oil market is in an unprecedented situation with issues thawing from both the demand and supply end. Governments across the world are trying to put their best foot forward to curtail the spread of COVID-19 any further, and at the same time to keep the economic engine from shutting down. The demand pick is expected as and when more confidence emerges with regard to the vaccine/drug development. The supply end of the story is currently in calm waters with major producers being in sync with each other and participating in a coordinated production cut. Strong players within the oil sector could stand to gain as and when the dark cloud around the uncertainty lifts.

II. Investment Theme and Stocks under Discussion (WPL, OSH, SXY and BPT)

After understanding the sector, let us now look at four companies listed on the ASX. The price potential of the companies under discussion has been analysed based on ‘Discounted Cash Flow’ methods.

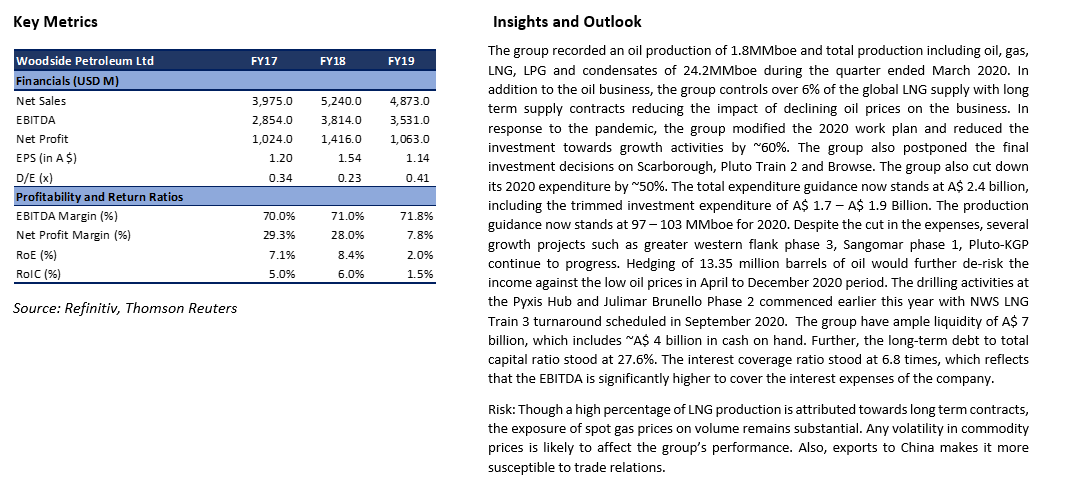

1. ASX: WPL (WOODSIDE PETROLEUM LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: A$ 20.66 Billion)

Woodside Energy is the largest petroleum exploration and production company in Australia.

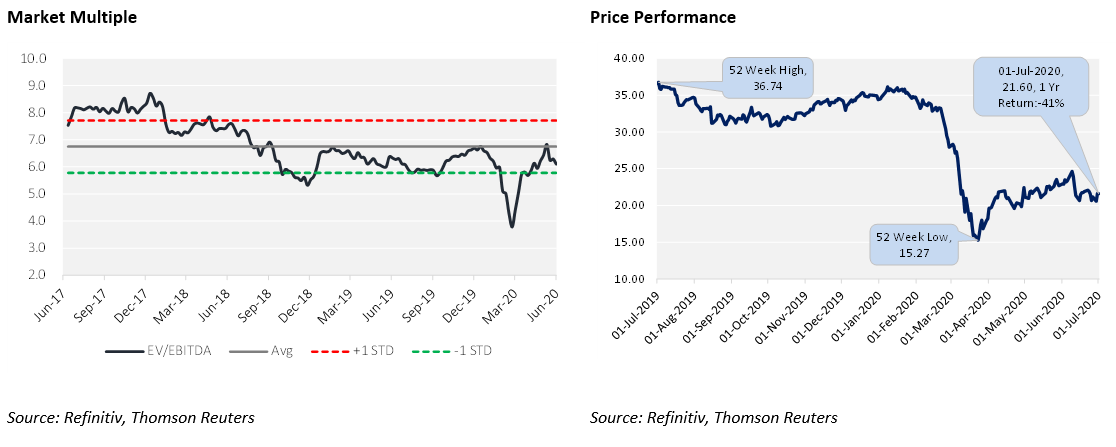

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~17% on 2 July 2020 closing price. At the same price, the stock is offering a dividend yield of ~9.0%.

.png)

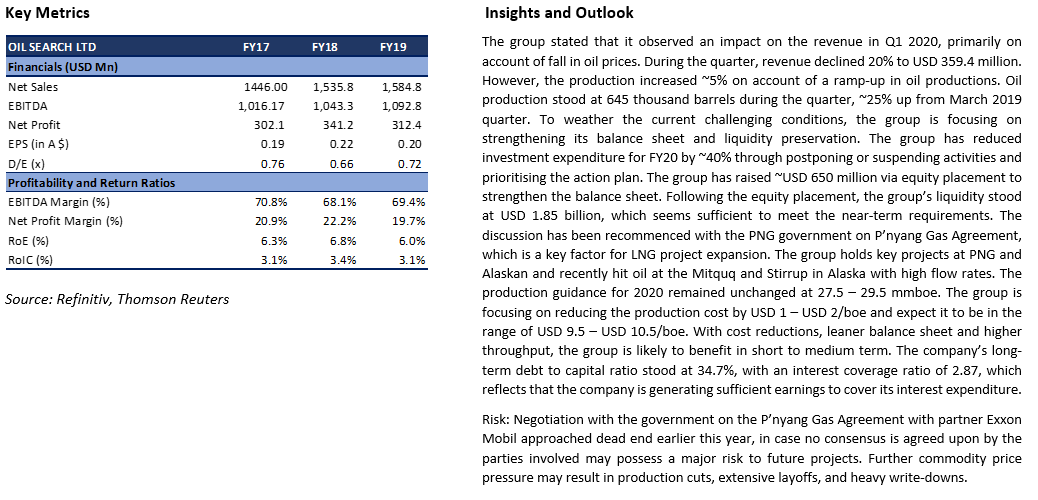

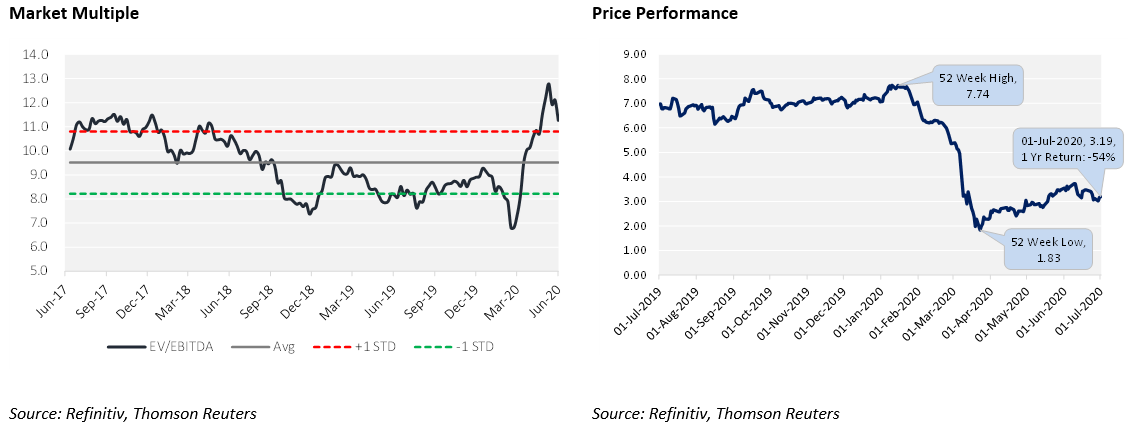

2. ASX: OSH (OIL SEARCH LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap: A$ 6.59 Billion)

Oil Search Limited is the largest oil and gas exploration and development company incorporated in Papua New Guinea, which operates all of Papua New Guinea's oilfields.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~19% on 2 July 2020 closing price. At the same price, the stock is offering a dividend yield of ~4.3%. .png)

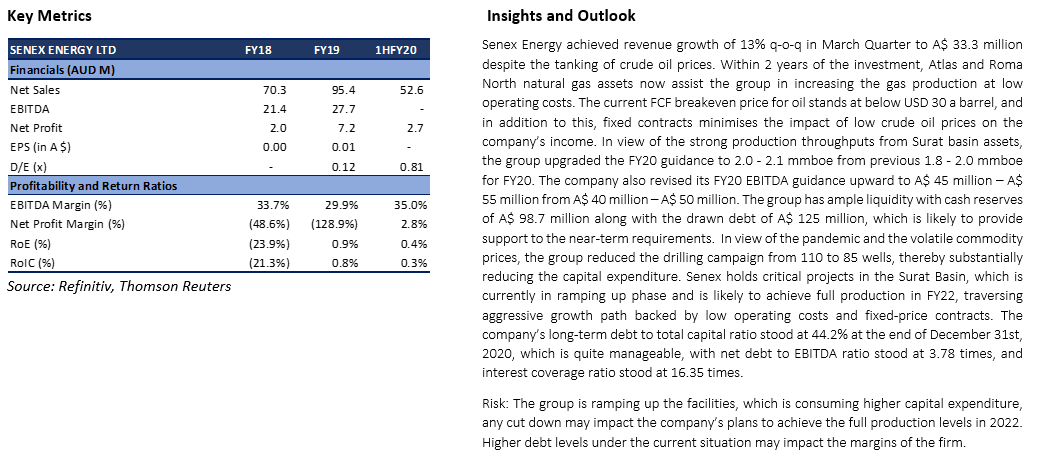

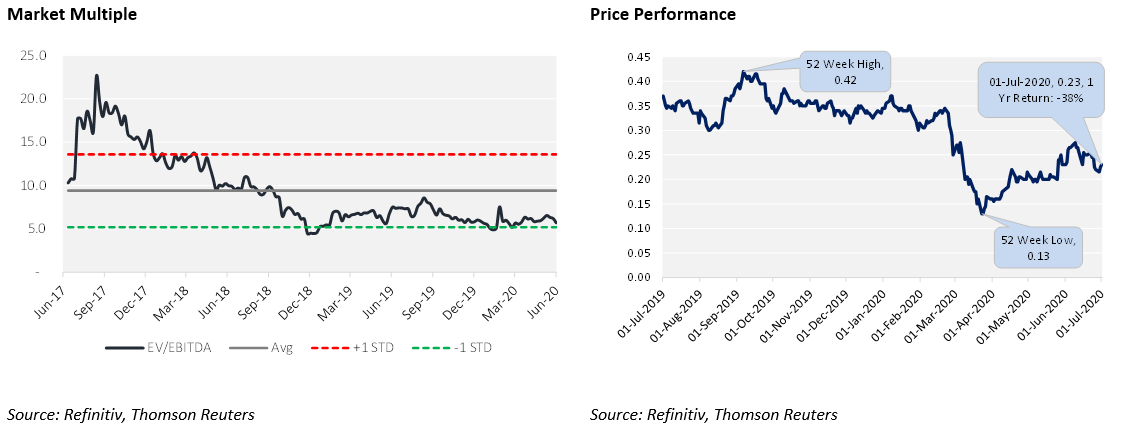

3. ASX: SXY (SENEX ENERGY LIMITED)

(Recommendation: Speculative Buy, Potential Upside: Low Double Digit, Mcap: A$ 328.0 Million)

Senex Energy Limited is an oil and gas exploration and production company. The Company's segments include Surat/Bowen Basin and Cooper/Eromanga Basin.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~22% on 2 July 2020 closing price. .png)

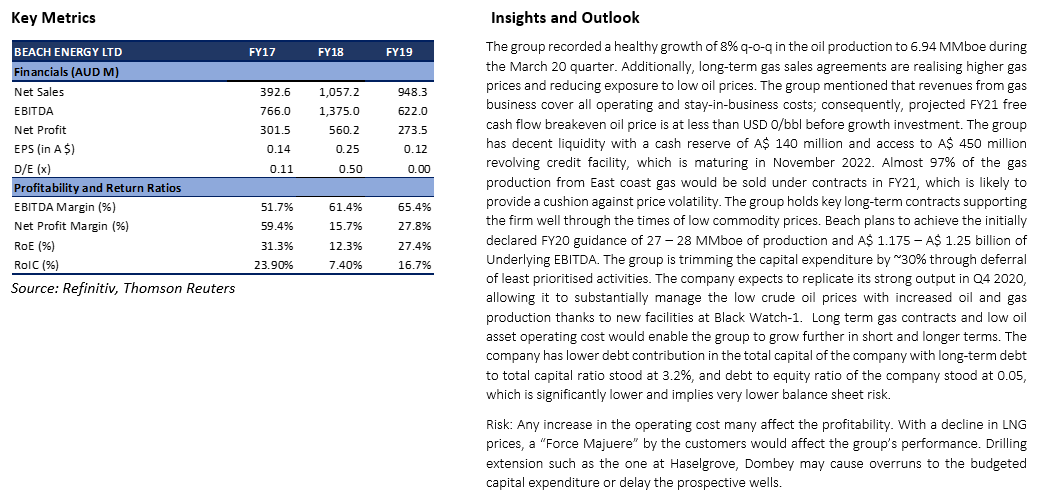

4. ASX: BPT (BEACH ENERGYLIMITED)

(Recommendation: Hold, Potential Upside: Mid-Single Digit, Mcap: A$ 3.47 Billion)

Beach Energy Limited is an oil and natural gas, exploration and production company. The Company’s operating segments include SAWA-South Australia and Western Australia, Victoria and New Zealand.

Valuation

Our illustrative valuation model suggests that stock has a potential upside of ~6% on 2 July 2020 closing price. At the same price, the stock is offering a dividend yield of ~1.9%. .png)

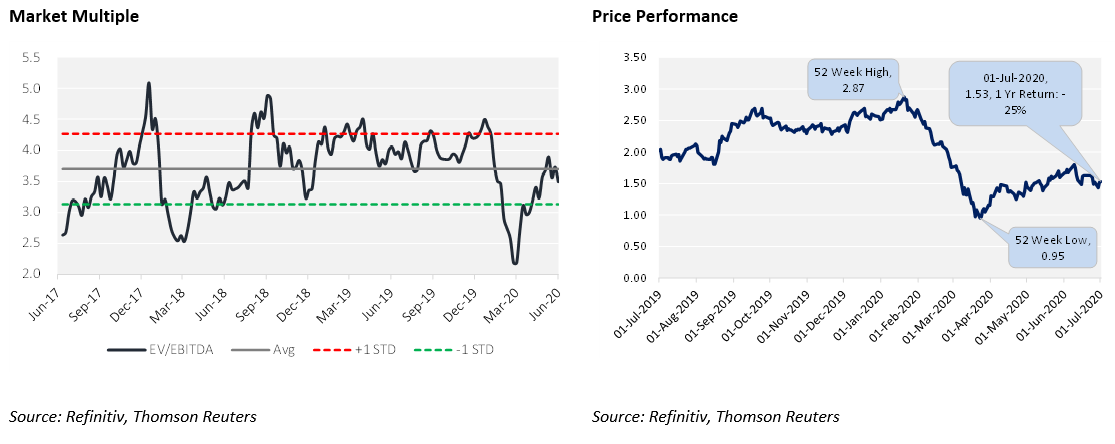

Note: All the recommendations and the calculations are based on the closing price of 2 July 2020. The financial information has been retrieved from the respective company’s website and Refinitiv (Thomson Reuters).

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...