Kalkine has a fully transformed New Avatar.

Company Overview: Cromwell Property Group is a global real estate investment manager. The Company is engaged in property investment, funds management, property management and property development. Its segments include Property investment, Property/internal funds management, External funds management-retail, External funds management-wholesale and Property development. Property investment segment is engaged in the ownership of investment properties located throughout Australia. The Property/internal funds management includes property and facility management, leasing and project management for its managed investment schemes. The External funds management-retail segment includes external funds for retail investors. External funds management-wholesale includes establishment and management of external funds for wholesale investors. The Property development segment includes property development, including development management, development finance and property development related joint venture activities..png)

CMW Details

Rise in Operating Profit: Cromwell Property Group (ASX: CMW) is an internally managed real estate investment trust of Australia and a property fund manager. The group is having operations in three continents and possesses a global investor base. As at 9th January 2020, the market capitalisation of the company stood at ~A$3.09 Bn. For FY19, the company reported statutory profit amounting to $159.9 million. The company’s operating profit rose by 11.1% from the previous year to $174.2 million. Its operating profit amounted to 0.21 cents per security, which is ahead of the full-year guidance of 8.21 cps. Notably, operating profit is being considered by Directors as the best metric which reflects the company’s underlying earnings. During FY19, the company retained some funds for the purpose of re-investment for growing the business and paid out 90% of earnings to securityholders which was as per the strategy of the company. Resultantly, the distributions for the year amounted to $157.5 million or 7.25 cents per security which meets the company’s full-year guidance. In Australia, the core portfolio of the company would continue to support its earnings as well as distribution policy. The company possesses a long WALE, high occupancy and good NOI growth. The company also has numerous ‘active assets’ which would provide additional repositioning opportunities moving forward. At the end of FY19, the company’s total AUM amounted to $11.9 billion which reflects an increase of $400 million.

.png)

Key Financial Highlights (Source: Company Reports, Thomson Reuters)

Gearing of the company stood at 35%, which was in the middle of its through-the-cycle revised gearing target range of 30% to 40%. The weighted average debt expiry was 4.5 years, diversified throughout 12 domestic as well as international lenders and two Convertible Bond issues. The “Invest to Manage” strategy of the company involves investing balance sheet capital for the creation of new funds in order to attract investment from the capital partners, enabling the company to release and redeploy capital towards other opportunities to build the enterprise value. The company’s objective revolves around generating sustainable returns for its securityholders from dynamic allocation as well as deployment of capital towards its business activities. We have applied two relative valuation methods, i.e., P/E multiple and P/CF multiple and have arrived at a target price of lower double-digit upside (in percentage terms).

Moving forward, there are expectations that the company’s “Invest to Manage” strategy, decent operational capabilities and liquidity position might act as tailwinds for long-term growth.

Top 10 Shareholders: The following image provides a broader overview of the top 10 shareholders of Cromwell Property Group:.png)

Top 10 Shareholders (Source: Thomson Reuters)

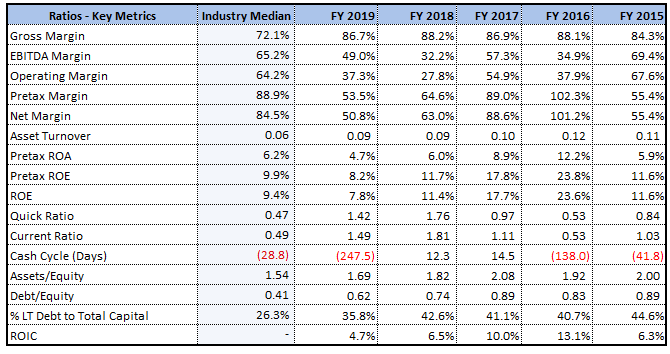

Decent Position of Key Margins: The company’s gross margin stood at 86.7% in FY19, which is higher than the industry median of 72.1%. Also, CMW’s operating margin 37.3%, which is higher than the FY18 figure of 27.8% and, therefore, it can be said the company has been possessing decent operational capabilities. Notably, its EBITDA margin stood at 49% in FY19 as compared to its FY18 figure of 32.2%.

Talking about the liquidity levels, the company’s current ratio stood at 1.49x, which is higher than the industry median of 0.49x. It looks like CMW’s decent liquidity standing might help the company in meeting its short-term obligations. Moreover, it provides the headroom for making decent deployments towards strategic growth objectives which might help it in achieving long-term. The company’s Debt/Equity ratio stood at 0.62x in FY19, which lower than the FY18 figure of 0.74x.

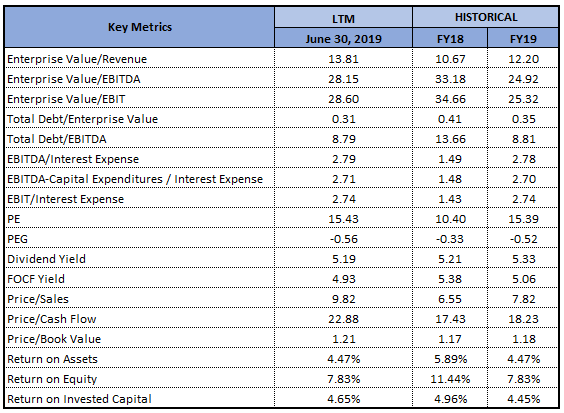

Key Metrics (Source: Thomson Reuters)

A Look at Recent Updates: Recently, the company issued a release stating that the Panel declined to conduct proceedings with respect to an application on behalf of Cromwell Property Group with regards to Cromwell’s affairs. As per the release, Cromwell has submitted that ARA Real Estate Investors XXI Pte Ltd and related entities, Ms Jialei Tang, Senz Holdings Limited, as well as people and companies connected to Mr Gordon Tang were associated and held a combined, however undisclosed, relevant interest along with voting power of up to 35.85% in the company.

Cromwell Property Group came forward and made an announcement about the retirement of Non-executive Director named Michelle McKellar after she has served the company for 12 years.

As per the release, Ms McKellar retired as the Director of Cromwell Corporation Limited and Cromwell Property Securities Limited (which happens to be the responsible entity of the Trust).

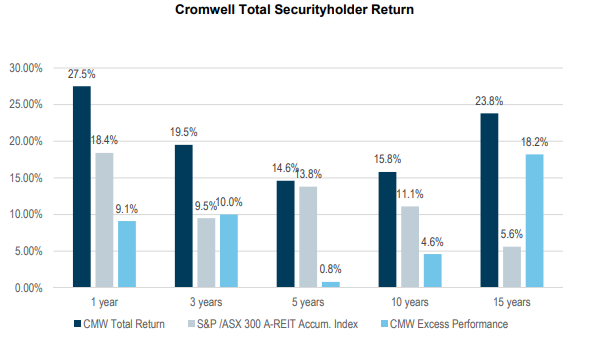

Total Securityholder Return of CMW: The company has recently released its quarterly business update and the key personnel has provided important information about total securityholder return. The following picture provides information about the total securityholder return:

Total Securityholder Return (Source: Company Reports)

In the same release, the company stated that, in Australia, the company has been recycling capital from assets where it has added significant value into new opportunities. It sold its 50% interest in Northpoint Tower for the consideration amounting to $300 million and made the acquisition of 400 George Street in Brisbane for an amount of $524.75 million. The company continues to progress its $1 billion pipelines of active asset opportunities. Coming to Europe, the company has signed formal binding agreements to acquire all of the third-party investor interests in Cromwell Polish Retail Fund (or CPRF). It is important to note that CPRF consists of 7 catchment-dominating retail centres having gross asset value amounting to around $1 billion.

With respect to Singapore, the company stated that The Cromwell European REIT (or CEREIT) has been growing. Moreover, wrapping up an €88.8 million acquisition of office asset in Poznan in Poland reflects that its portfolio comprises 102 properties in 7 European countries. Also, Cromwell’s 32% stake has been worth around €400 million.

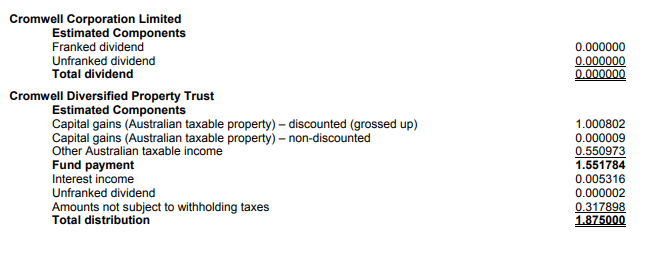

Recent Update on Distribution Components: The company has provided information about distribution for September 2019 quarter and the following picture provides the information about components:

Key Information (Source: Company Reports)

The distribution payment was made on November 22, 2019, to the persons who held Cromwell Property Group stapled securities at September 30, 2019.

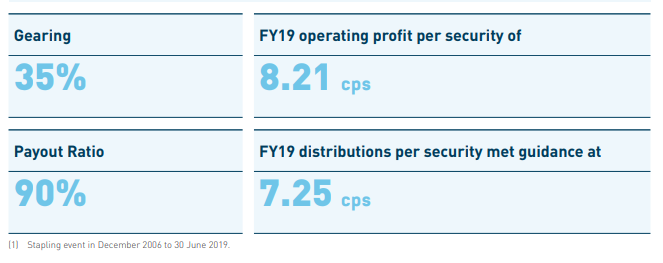

Decent Dividend Related Parameters: In FY19, CMW declared distributions per security amounting to 7.25 cps and, as a result, the company managed to meet its guidance for the full year and posted its payout ratio of 90%. Therefore, it can be said that CMW has been managing its operations quite well and is focusing on improving the returns to its shareholders. The company offers its securityholders a combination of stable long-term cash flows, sound asset enhancement capabilities, and transactional profits, as well as low-risk exposure to international capital flows and European economic growth.

Key Dividend-Related Parameters (Source: Company Reports)

What to Expect from CMW Moving Forward: The company is focused towards continuing execution of ‘Invest to Manage’ strategy, capital recycling as well as value-add development opportunities. Moreover, balance sheet of the company happens to be robust and the company is well placed to reap the benefits of opportunities that it has in its pipeline, and those that it identifies in the volatile market in general. In Australia, the company’s Core and Core+ portfolios would continue to drive NOI and support its earnings and distribution policy. Moreover, its $1 billion pipelines of development opportunities would be providing upside in the asset values along with opportunities to attract the new capital partners.

For FY 2020, the company has affirmed its guidance for operating profit of minimum 8.30 cps and it has also affirmed the distribution guidance of minimum 7.50 cps.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

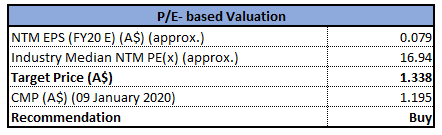

Method 1: P/E Based Valuation

P/E Based Valuation (Source: Thomson Reuters)

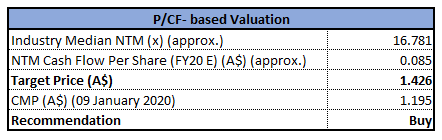

Method 2: P/CF Based Valuation

P/CF Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

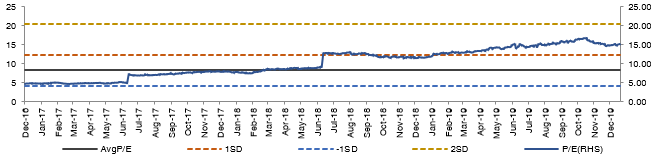

Historical P/E Band (Source: Thomson Reuters)

Stock Recommendation: The stock of CMW has delivered a return of 20.30% in the span of the previous one year and, on YTD basis, it has posted a return of 1.72%. The company would be prudently deploying capital and executing the transactions when there are opportunities and has a focus on long-term value creation. Moreover, it was added that securing investments, deploying investment capacity along with recycling of the balance sheet capital would be resulting in the company’s gearing oscillating, in the short to medium term. However, it was added that this would be within and around the target gearing range of 30 – 40%. Over the longer term, there are intentions to maintain its normalised gearing within the target range. Based on the foregoing, we have applied two relative valuation methods, i.e., P/E multiple and P/CF multiple and have arrived at a target price of lower double-digit growth (in percentage terms). Hence, we give a “Buy” rating on the stock at the current market price of $1.195 (up 0.844% on 9 January 2020).

CMW Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...