Company Overview: Credit Corp Group Limited (ASX: CCP) is one of the largest providers of sustainable financial services in the credit‑impaired consumer segment in Australia. It operates within the Australian debt collection and consumer lending industry. The company reports its performance under two major segments, including Debt ledger purchasing and consumer lending. The debt ledger purchasing segment is engaged in purchasing consumer debts at a discount, and consumer lending provides the cheapest and most sustainable loan products to consumers who have limited borrowing alternatives..png)

CCP Details

Consistent Record of Success and Continued Growth: Credit Corp Group Limited (ASX: CCP) is one of the largest providers of sustainable financial services in the credit‑impaired consumer segment in Australia. It operates within the Australian debt collection and consumer lending industry. As of 25th May 2020, the market capitalization of the company stood at ~$948.42 million. During FY19, the company delivered a consistent record of success and continued growth with an increase of 8% in revenue to $324.3 million and a growth of 14% in income-generating assets to $586.5 million. In a chaotic and turbulent year for financial services companies in Australia, Credit Corp Group Limited stands out as a focused and value-driven organization. The company continued to reap the benefits of past improvements and reported an increase of 9% in Net Profit After Tax to $70.3 million. CCP is in a decent position to realize the returns of its long-term outlook and sustainable approach. The strong financial performance resulted in an increase of 5% in earnings per share to 141.9 cents. The company also paid a full-year dividend of 72 cents per share in FY19. CCP has developed a sophisticated understanding of credit-impaired consumers and has the ability to predict their behaviors. The company has built a flexible collection platform incorporating leading analytics, technology, and a workforce which leveraged in expansion. Over the span of 4 years from FY15 to FY19, the company reported a CAGR of 14.15% in total revenue and a CAGR of 13.89% in gross profit, reflecting a disciplined growth strategy, positioning the company to benefit from the increased business opportunities. The company has superior analytics capabilities, advanced technology, and sustainable approach, which will help the company to stay ahead of the market.

The company has also released its interim results for the half-year ended 31 December 2019, wherein it reported strong growth in all its segments. CCP grew its market share for the purchased debt ledger segment in the later first half. Credit Corp Group Limited continued to achieve operating metrics and has delivered sustained growth and returns.

The company increased investment across all businesses and is planning to further increase investment in the coming years with the hope of continued growth in earnings. The sustainable advantages reflected in the company’s performance and outlook have been built on rigorous adherence to its values. The stance for consumer lending and US debt purchasing is positive with strong growth in profit and increased investment.

FY19 Financial Highlights (Source: Company Reports)

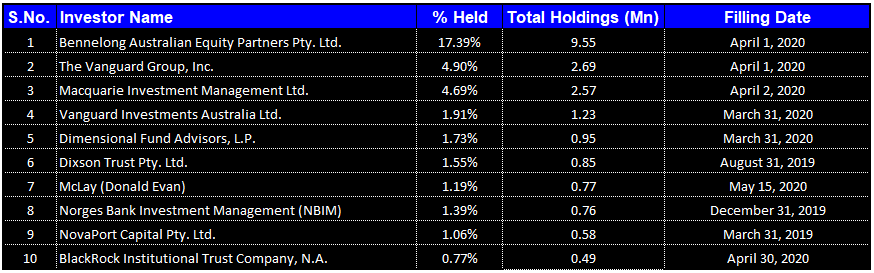

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Credit Corp Group Limited. Bennelong Australian Equity Partners Pty. Ltd. is the largest shareholder in the company, with a percentage holding of 17.39%.

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

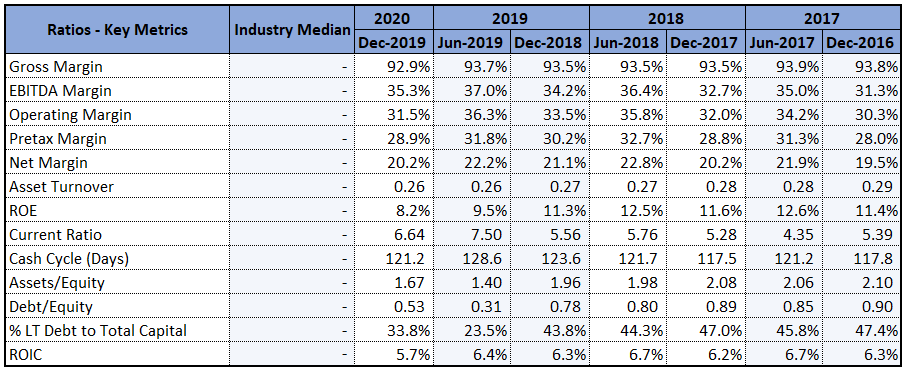

Increased Profitability and Financially Stable Balance Sheet: During 1H20, EBITDA margin of the company witnessed a YOY increase and stood at 35.3%, up from 34.2% in 1H19, indicating increased profitability. Over the past three years from 1H17 to 1H20, net margin of the company went up to 20.2% from 19.5%. This indicates that the costs of the company are stable, and it is capable of converting its revenue into profits. During 1H20, return on equity of the company was 8.2%. In the same time span, current ratio of the company stood at 6.64x, up from 5.56x in 1H19. This indicates that the company is liquid enough to pay off its current liabilities using its current assets. During 1H20, Assets/Equity ratio of the company went down to 1.67x from 1.96x in 1H19. In the same time span, Debt/Equity ratio of the company was 0.53x, as compared to 0.78x in 1H19. The decline in Assets/Equity ratio and Debt/Equity ratio indicates that the business is financed with a more significant proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Refinitiv, Thomson Reuters)

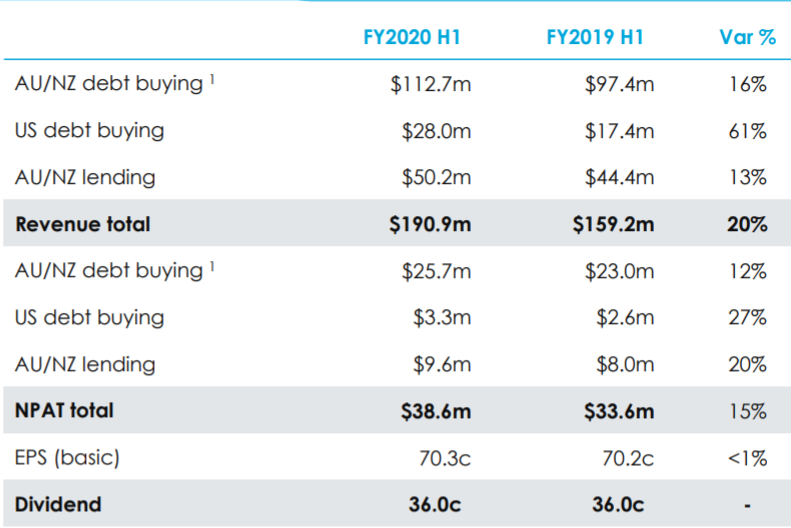

Strong Start to FY20: During 1H20, the company has delivered sustained growth and returns with an increase of 13% in the consumer loan book to $230 million. CCP reported remarkable growth metrics in the US debt buying with an increase of 55% in investment, growth of 75% in headcount, rise of 57% in collections, and commencement of a second collections facility with a seating capacity of 270. During 1H20, revenue of the company witnessed an increase of 20% to $190.9 million, up from $159.2 million in 1H19. In the same time span, NPAT of the company went up by 15% to $38.6 million from $33.6 million in 1H19. The combination of solid operations with decent management of the company, places CCP in a very powerful proposition. During the half-year, the Australian/New Zealand debt buying segment produced record collections and NPAT, with strong results from the existing business complemented by the performance of the acquired Baycorp assets.

1H20 Financial and Operational Highlights (Source: Company Reports)

Completion of $120 million placement: The company has recently completed the fully underwritten Institutional Placement wherein it issued 9,600,000 new shares for an offer price of $12.50 per share. The proceeds will strengthen the balance sheet of the company and will enable CCP to pursue debt purchasing opportunities as economic uncertainty endures.

Key Risk from COVID-19: Credit Corp Group Limited has observed a high degree of uncertainty in the financial markets in response to COVID-19. The company may have to limit its debt buying and agency tender contract re-negotiations in response to the uncertain economic outlook. The rising unemployment might result in reduced collections and may increase consumer loan book negligence. However, the company operates in highly regulated industries and is subject to extensive laws and regulations and is managing risk by placing a strong emphasis on its regulatory compliance.

Future Expectations and Growth Opportunities: The acquisitions and business segments have performed strongly over the first half and are on track for further growth opportunities. The sustainable advantage is being reflected in the company’s financial and operational performance and thus has built a positive outlook on rigorous adherence to its values. The company’s expansion strategy and its disciplined adherence to its return criteria demonstrated the benefits of its strength and resulted in further growth. The company is pursuing a diversified expansion strategy by operating across a range of markets and hence is able to invest for sustained growth.

CCP is establishing measures, setting targets, and putting in place plans and actions to ensure that expectations are achieved regardless of external influences from any uncertainty like COVID-19. The initial impacts of the virus have, however, been cushioned by the government and the business was operational throughout the closures.

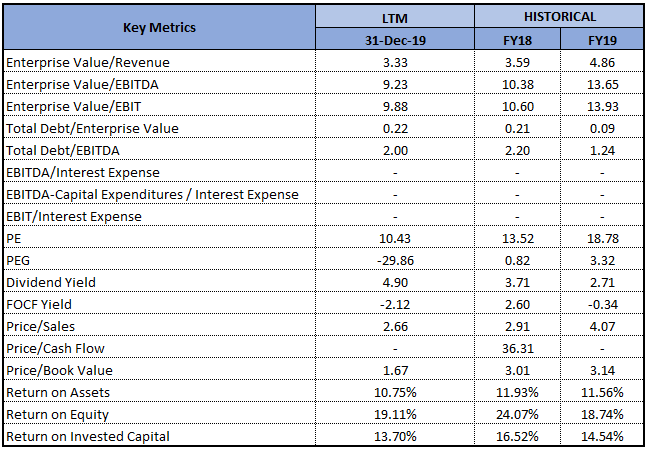

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

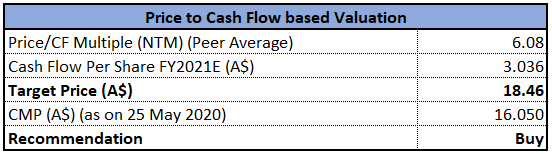

Valuation Methodology: Price to Cash Flow Multiple Based Relative Valuation Approach (Illustrative)

Price to Cash Flow Multiple Based Relative Valuation Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: The stock is currently trading below the average of 52-week low and high of $6.010 and $37.990, respectively, proffering a decent opportunity for the investors for accumulation. The company has entered an uncertain period with a strong balance sheet, and the additional capital raising allowed the company to manage through a significant downturn without putting its businesses into a run-off for a prolonged period. Credit Corp Group Limited is well-positioned to continue to perform strongly in the future and is witnessing signs of stress in competitors which appears to create opportunities for additional investment. Considering the attractive trading levels, decent financial and operational performance, company’s expansion strategy, and positive long-term outlook, we have valued the stock using the price to cash flow multiple based relative valuation approach and have arrived at a target upside of lower double-digit (in percentage terms). Hence, considering the aforesaid parameters and current trading levels, we recommend a ‘Buy’ rating on the stock at the current market price of $16.05, up by 9.184% on 25 May 2020.

.png)

CCP Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...