Kalkine has a fully transformed New Avatar.

.PNG)

The Australian Bureau of Statistics lately released the inflation data, stating a rise in consumer prices for the three months ended March 2020, that pushed annual price rises to a five and a half year high. The increase in inflation may seem to be a direct impact of the economic turmoil due to COVID-19, however, the less talked about incidents prior to COVID-19 have played an equal role in shaping the index. Drought and unprecedented bushfires also damaged the business activities and have certainly affected consumer behaviour and demand/supply patterns in the first quarter.

Food and beverage prices have shown significant sensitivity to drought and went up by 3.2% over the twelve months to March 2020. This was majorly a result of panic buying in the month of March, due to the drought effects. Moreover, prices were partially affected by COVID-19 which led to the purchase of selected items due to a chain of restrictions imposed. Also, rapid bushfires led to supply shortages due to transport disruptions, that formed another factor impacting food prices. Among food and beverages, the sharpest rise in the March quarter, was seen by the bag of vegetables, that form a staple for consumers. Other than vegetables, prices also increased across other categories, including fruits, beef, lamb, bread, meat, seafood, milk and cereals. On the contrary, fuel prices, domestic and international holiday travel, etc, have slumped drastically, due to a massive fall in demand. While the rise in food prices has majorly been a result of panic buying, which has lightened up with time, the factors impacting the above-mentioned groups may have a prolonged impact on Australia's inflation data.

A Look at CPI Data: For the March quarter, the headline CPI for Australia increased by 0.3% in original terms and 0.4% in seasonally adjusted terms, representing a rise to over 5-year high due to the collective impact of drought, bushfires, and COVID-19. Over the 12 months to 31st March 2020, inflation rose 2.2%, as compared to a rise of 1.8% over the 12 months to the December 2019 quarter.

As per the data provided by the Australian Bureau of Statistics (ABS), the most significant rises during the month were seen across four categories including, vegetables, tobacco, secondary education and pharmaceuticals. The percentage rise across these categories stood at 9.1%, 2%, 3.4% and 5.1%, respectively.

On the other hand, the most significant fall was witnessed by the automotive fuel, domestic holiday travel and accommodation and international holiday travel and accommodation categories, with a percentage decline of 6%, 3.1% and 3%, respectively..png)

CPI Data (Source: Australian Bureau of Statistics)

What to Expect: The above results, however, do not provide a clear picture of the current events impacting the prices, which may reflect in the CPI for the coming quarter. As panic buying subsides and COVID-19 related economic impacts begin to take control of the situation, Australia may witness a shift to deflation. Prices for many categories have fallen to multi-decade lows and the economy has seen numerous challenges beyond March due to COVID-19. Performance of businesses has been significantly impacted, which will further impact the availability of good and services in the market. Moreover, the impact of recent market challenges with respect to the plunge in oil prices, changes in consumer spending, and stimulus packages to revive the economy, is yet to be seen completely in the data.

Due to a highly unpredictable scenario, it is difficult to identify a single segment that will come out clean as the storm settles. COVID-19 has impacted every section of the society and has dented their financial health in one way or the other. The corporate community has been struggling with various operational and financial challenges, which have given rise to an unprecedented approach to ensure business continuity. While the negative impacts of the outbreak cannot be fully controlled at the company level, the businesses which have acted proactively to mitigate the risks are expected to recover faster in comparison to other similar players. Considering the above factors, let us now have a look at four stocks that have demonstrated a resilient performance during the ongoing uncertainties through several initiatives for guarding the business against the adverse impacts of COVID-19, along with continued efforts to ensure long-term economic success.

1. Tassal Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 775.83 Million, Annual Dividend Yield: 4.85%)

Successfully Executing Operational Strategy: Tassal Group Limited (ASX: TGR) is a seafood processing company, involved in the production and sale of premium salmon, prawn and seafood products for both the Australian domestic and export markets. In the first half of FY20, the company reported revenue of $274.49 million and operating NPAT of $30.64 million. During the half year period, the company successfully executed its operational strategy to keep salmon in the water to grow both biomass and size and support long-term growth in earnings and returns. Further, the company also executed a specific strategy to harvest and sell less salmon to deliver strong harvest biomass, sales and earnings growth from 2H20 for FY20 and FY21. Over the period, the company saw continued growth in salmon operating EBITDA $/kg due to cost efficiencies and further optimisation of sales mix. For H1FY20, the company reported operating cashflow of $41.0 million, in line with the company’s expectations.

Outlook: Although the long-term impacts of COVID-19 on consumer behaviour are still unknown, early indications are showing some trends which are positive to Tassal. Going forward, the company’s delivery of its salmon growth strategy, combined with its strategic investment in prawns, is expected to deliver long-term growth in earnings and returns in FY20 and beyond. In the Salmon business, the company is focused on capitalizing on the greater biomass and size in 1H20, through delivering increasing harvest and sales in 2H20 and FY21. Overall, market dynamics for salmon remain positive.

Although the Consumer confidence index is currently at an all-time low level, the consumers continue to seek healthy and sustainable proteins as part of their diet. Salmon and Prawns fulfill the needs of consumers as healthy and sustainable proteins, offering Tassal Group an opportunity to increase seafood’s percentage share of plate..png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.png)

A-VIX vs TGR (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: TGR is currently well placed to drive consumption per capita of salmon and prawns. In the last six months, the stock of TGR has declined by 11.03% on ASX and is trading below the average of its 52 weeks low and high level of $2.770 - $5.250. In the chart above, we see a steep fall in the stock price as the markets became a victim to coronavirus led tensions. After the steepest fall in the last six months, the stock has demonstrated a V-shape recovery and now seems to be on a stable ground. In the long-term, the stock will be further supported by the company’s investments for the growth of salmon and prawns. Moreover, near-term benefits will be derived out of positive consumer behaviour amid COVID-19, as consumers purchase what they trust. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price of lower double-digit (in percentage terms). Considering the company’s decent performance in H1FY20, its expected performance in H2FY20 and beyond, market dynamics for salmon and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $3.750, up by 1.078% on 4th May 2020.

2. G8 Education Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 642.22 Million, Annual Dividend Yield: 12.43% (price correction led increase)

GEM Rides on Acquisition Synergies and Higher Occupancy: G8 Education Limited (ASX: GEM) operates early education centres. The company is gaining momentum on a continued basis and has found support for its FY19 results on the back of drivers such as stimulating demand, acquisition activity and improved financial performance. In FY19, the company completed the acquisition of 15 centres, divested 25 centres and closed 16 underperforming centres. Its revenue for the period increased ~ 7.5% year over year to $922.2 million and witnessed an organic earnings growth of 3% after investment in quality. This was driven by occupancy, fee growth and acquisitions. GEM has a strong balance sheet with lower costs and longer tenor in debt structure.

Outlook: The company is prioritizing to drive growth in its network of early learning centres through acquisition opportunities and greenfield development. The company will focus on driving cost competences to support EBIT acceleration. Due to the COVID-19 pandemic, the company is currently providing free childcare for all the enrolled families, effective from April 6, 2020. As per the CPI data provided by the Australian Bureau of Statistics (ABS), the secondary education category, witnessed a rise of 3.4%. The company will continue to drive sustainable growth with an increased focus on centre refurbishment program, ensuring the safety of children in its care, families and team members, enhance learning environments and executing its latest people management platform. Such programs are aimed at driving occupancy in current centres along with positioning GEM as the employer of choice in the education sector..png)

Valuation Methodology: EV/Sales Multiple Based Relative Valuation (Illustrative).png)

EV/Sales Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

.png)

A-VIX vs GEM (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: As per ASX, the stock of GEM, is trading close to its 52-week low level of $0.437, proffering a decent opportunity for accumulation. The stock of the company corrected by 63.38% over a period of 6 months. Notably, the stock has gained 12.05% in the past one-month period. The market’s reaction to highly volatile conditions due to COVID-19 outbreak, led the stock price to tumble due to heightened legal and regulatory issues. However, recovery in the price has been decent afterward, underpinned by various business initiatives to mitigate the near-term financial impact of COVID-19. While the sector witnessed reduced occupancy rates due to COVID-19, the Early Childhood Education and Care Relief Package announced by the government is anticipated to increase sector occupancy levels by reducing parent fees to nil during the package period. Moreover, the company’s highly qualified Centre based teams, along with pre-COVID-19 operational and growth initiatives, will support recovery in occupancy and earnings. We have valued the stock using EV/Sales multiple based illustrative relative valuation method and arrived at a target price with low double-digit upside in percentage terms. Considering the company’s decent performance in FY19, recent cost reduction initiatives, acquisition synergies, higher occupancies, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $0.835, down by 3.468% on 4th May 2020.

3. Freedom Foods Group Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.2 Billion, Annual Dividend Yield: 1.26%)

Decent Growth in Key Branded Categories and Channels: Freedom Foods Group Limited (ASX: FNP) is a nutritious food & beverages company, specialised primarily in soy, rice milks and breakfast drinks. In the first half of FY20, the company saw growth in key branded categories and channels. For the period, the company reported net sales of $277.1 million, up 32.6% on pcp. Further, the company recorded a statutory net profit of $5.4 million in H1FY20, up 45.6% on pcp. During the half-year, the company witnessed exceptional growth in SE Asia region with sales revenues growth of 58%. For Dairy & Nutritionals products, the company witnessed a net sales growth of 45% and for Plant Based products, net sales grew by 39.2%.

Outlook: Amid the COVID-19 pandemic, the company is witnessing strong demand for its key products including UHT dairy and plant beverages and cereals & snacks. During the period, the company has successfully secured distribution including national ranging with McDonalds for the MILKLAB brand and further ranging with other speciality food chains & quick service restaurants. In order to ensure a strong position to continue on a positive trajectory towards building a major global food and beverage business, the company is currently reshaping its operational footprint which will ensure a strong platform for growth in sales and profitability over the medium term. The company is experiencing increasing demand in key channels and markets, which raises the optimism regarding the opportunities ahead as market uncertainties reduce.

Despite the challenges put forward by COVID-19, the food and beverages sector has been at a safer position with respect to continuity of operations, on account of being an essential service for the community. Prices across the segment continued to rise due to panic buying and increased demand, which pushed the inflation rate for the segment to a higher level. On a company level, FNP’s key brands and market position provide decent prospects for growth in the post COVID-19 period and over the medium term..png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative).png)

EV/EBITDA Multiple Based Approach (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.png)

A-VIX vs FNP (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: FNP continues to move on a positive trajectory to become a major global food and beverage business in key markets and channels in Australia, China and South East Asia. In the chart above, we can see that the stock price has also witnessed sharp spike with the rise in market volatility. So far, the price has been supported by increased demand for products and diversified capabilities of the business. Moreover, with sufficient liquidity and financial flexibility to deal with the current uncertain environment, the company seems well-positioned for further growth. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). For the purpose, we have taken peers like Synlait Milk Ltd (ASX: SM1), Blackmores Ltd (ASX: BKL) and Costa Group Holdings Ltd (ASX: CGC). Considering the company’s decent performance in H1FY20, its current liquidity position, and increasing demand for its key products, we give a “Buy” recommendation on the stock at the current market price of $4.280, down by 1.609% on 4 May 2020.

4. Coca-Cola Amatil Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 5.87 Billion, Annual Dividend Yield: 5.8%)

Well-Positioned to Capture Growth: Coca-Cola Amatil Limited (ASX: CCL) is engaged in the manufacturing, distribution and marketing of beverages. During the year ended 31st December 2019, the company reported an increase of 6.7% in group revenue to $5,070.6 million and witnessed a significant growth of 34.2% in statutory NPAT to $374.4 million. The company strengthened its focus on customers and simplified its operating model. The benefits of changes in operating model are evident in the strong financial results. These results also reflect successful outcomes from strategic initiatives in territories, strong in-market execution and targeted investment in the Australian and Indonesian businesses.

Outlook: The company has introduced new product innovations and its progress is evident in its ability to win market share, deliver new business growth and receive strong customer recognition. CCL possesses a strong balance sheet, ensuring that it is well-positioned to navigate the global pandemic. The company is likely to retain a conservative balance sheet and is expected to deliver a strong return on capital employed.

As per the latest CPI data for the March quarter, the food and non-alcoholic beverages segment have seen a rise of 1.9% Q-o-Q and 3.2% over the 12 months period. This came on the back of rising prices across the segment due to multiple factors, including drought, bushfires and the most recent outbreak of COVID-19. With the continuously evolving beverage market and strong demand across the segment, the company seems well placed to make way for further growth through its unique capabilities..png)

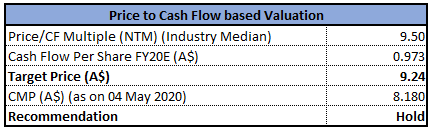

Valuation Methodology: Price to Cash Flow Multiple Based Valuation (Illustrative)

Price to Cash Flow based Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

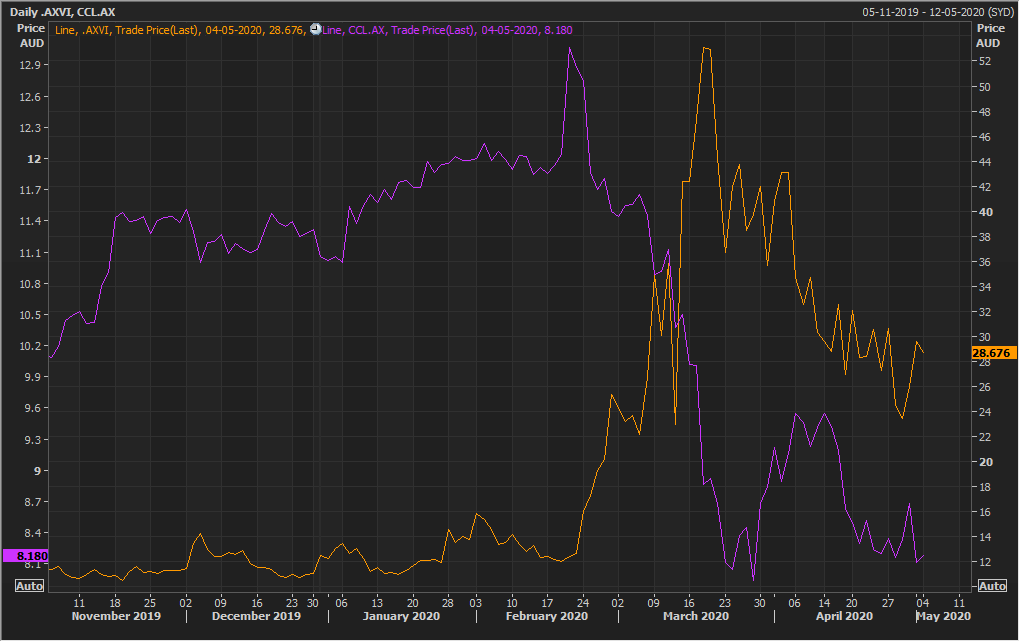

A-VIX vs CCL (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: CCL is a strong organization with a proven ability to adapt and capitalize on opportunities to further grow its portfolio of brands and businesses. The company has entered new geographies and seeks to maximize long-term sustainable returns for its shareholders. The stock is trading close to its 52-weeks’ low level of $7.77. While the stock price tumbled in response to the outbreak of coronavirus and subsequent unrest in the market, recovery in the near term will be supported by the strong foundations laid in FY19. With robust market dynamics for beverages and continued efforts by the management to drive innovation and growth, the company is expected to maintain a resilient position throughout the current economic downturn. Therefore, the uncertainty surrounding the fallout of COVID-19 might pose some near-term challenges, but the stock has decent potential in the long run. Considering the trading levels, financial strength and decent growth catalysts, we have valued the stock using price to cash flow multiple based relative valuation and have arrived at an indicative target price with an upside of lower double-digit (in percentage terms). Hence, we give a ‘Hold’ rating on the stock at the current market price of $8.18, up 0.863% on 4th May 2020.

.JPG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...