Company Overview - Cover-More Group Limited is an integrated travel insurance and medical assistance provider. The Company operates in Australia and Asia. The Company operates in two business lines: travel insurance and medical assistance. Key activities in travel insurance include developing and pricing travel insurance products, managing the sales strategy (through travel agents and online channels, both intermediary and direct), and receiving and managing claims. Key activities in medical assistance include managing travel related medical claims and managing client employee related mental and health issues. In Australia, New Zealand and the United Kingdom, Cover-More travel insurance is underwritten by Munich Re Group. Travel medical assistance operates under the CustomerCare brand, providing 24/7 emergency medical assistance for travelers that have taken out travel insurance.

Analysis – CVO is an almost pure play travel service company given it is the largest Travel Insurance Company in Australia yet it outsources claims risk to insurance underwriters. We believe the company is in a sound position to leverage off the strong international Holiday thematic that has been the dominant feature of the Australian travel landscape over the last ten years. We view the medium term outlook for International Holiday Travel as sound driven by a combination of low airfares, a favorable currency, increasing capacity from low cost airlines and solid domestic economy.

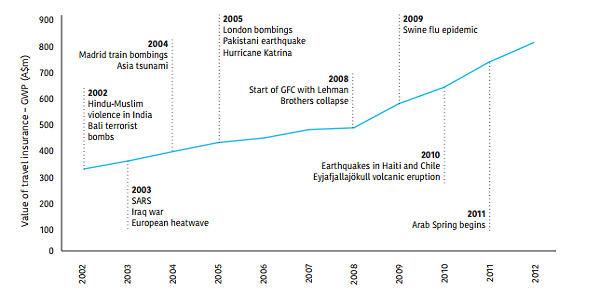

Long term growth in the Australian travel insurance market (Source - Company Reports)

Long term growth in the Australian travel insurance market (Source - Company Reports)

CVO has a long history in the Travel Insurance segment having commenced operations in 1991 before growing to become Australia’s largest player with an estimated market share of around 40%. The company’s initial focus was on distribution through travel agents based on a cornerstone joint venture with Flight Centre that has in place for some 23 years and is due to expire in 2019. In recent years the focus has turned to expanding distribution beyond the traditional base both domestically and internationally.

Outbound travel volumes in core cover more markets (Source - Company Reports)

Outbound travel volumes in core cover more markets (Source - Company Reports)

The company does not participate in claims risk as this outsourced to third party insurers. This means CVO is effectively a travel service company whose earnings are largely a function of International Holiday Travel out of Australia by domestic households. Over the last ten years we have seen very strong growth in this variable driven a combination of lower airfares, a favorable currency, increasing capacity from low cost airlines and solid domestic GDP/household growth. We expect the demand for International Holiday Travel to remain sound despite short term volatility in household consumption expenditure which we view as transitory.

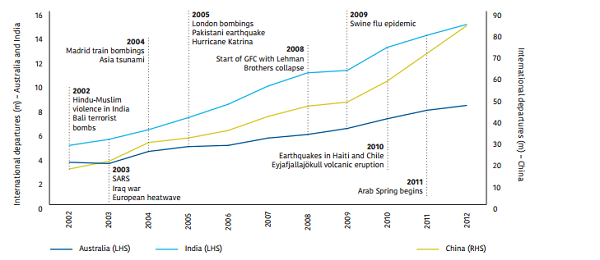

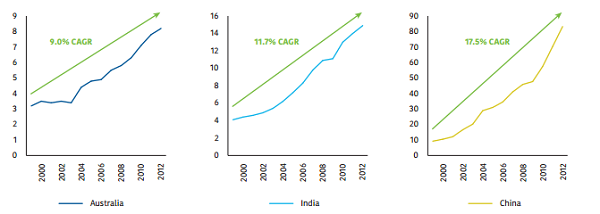

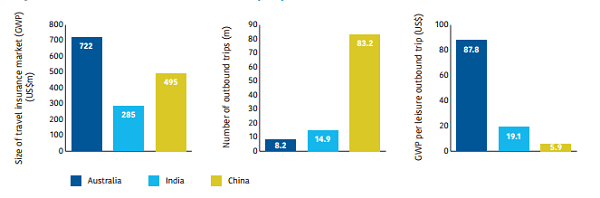

Growth in outbound travellers from Australia, India and China (Source - Company Reporwts)

Growth in outbound travellers from Australia, India and China (Source - Company Reporwts)

In recent years the company has successfully extended distribution of its products through the execution of third party agreements with a range of suppliers including: Medibank, Australia Post, Malaysia Airlines, Air New Zealand and a number of Australian Automobile Clubs. This initiative has all been assisted by the development of the impulse e-commerce which assists distribution partners maximize travel insurance sales to clients. At the same time company is in early stage of developing core travel insurance capabilities in India, China and Malaysia with material upside potential given thee the underdeveloped nature of these markets.

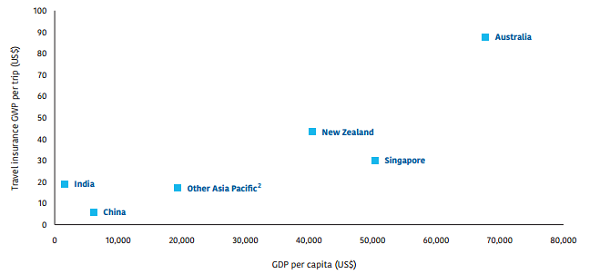

GDP Per Capita VS GWP per foreign trip (Source - Company Reports)

GDP Per Capita VS GWP per foreign trip (Source - Company Reports)

We consider CVO is well positioned to deliver strong earnings growth over the medium term. The investment appeal of the company is further enhanced by the fact that it is a capital light business (capital expenditure of around $6m per annum) with negative working capital requirements given cash is received before payment to suppliers.

Travel volumes and Insurance market (Source - Company Reports)

Travel volumes and Insurance market (Source - Company Reports)

CVO derives an estimated 84% of its earnings from the sale of Travel Insurance and associated Travel Medical Assistance products. Further we note that Australia/NZ remains the dominant geographical market given it represents around 86% of group earnings. A key aspect of the CVO business model is the fact that the company does not participate in claims risk. In Australia/NZ and the UK, the claims risk for CVO’s travel insurance policies is borne by Munich Re, in Malaysia by eTIQa and in china by CCIC. In India CVO distributes travel insurance policies and the underwriting risk in respect of these products is borne by National Insurance. In our view CVO should be considered a travel services provider not an insurance company that offers travel related products.

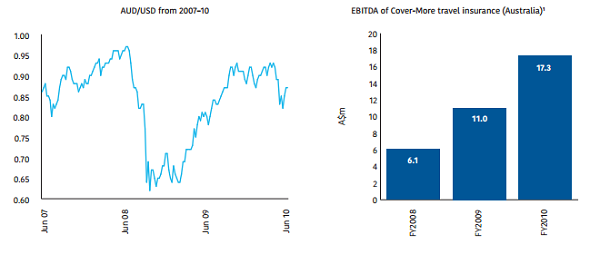

Effect of GFC and foreign exchange volatility on Cover More Profitability (Source - Company Reports)

Effect of GFC and foreign exchange volatility on Cover More Profitability (Source - Company Reports)

The demand for travel insurance was primarily driven by outbound travel (as opposed to domestic travel) as individuals typically have domestic health and general insurance cover for domestic travel. Growth in the travel insurance market is therefore function of the percentage of travelers who elect to take up insurance and outbound travel volumes. We understand that the percentage penetration of Travel Insurance taken up is around 70% and that this variable has broadly remain unchanged for some time. This suggests to us the, most important driver of CVO’s earnings is therefore the level of international travel out of Australia by domestic residents or outbound tourism consumption.

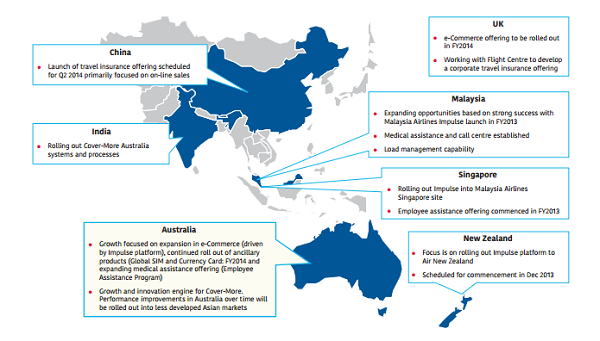

Cover More Growth Opportunities (Source - Company Reports)

Cover More Growth Opportunities (Source - Company Reports)

Analysis suggests that there has been very strong growth in outbound tourism consumption over the last ten years at the expense of domestic tourism. This growth is largely a function of exceptional growth in short term international departures out of Australia by domestic residents particularly for holiday purposes. We not this segment is the most relevant for CVO as short term international holiday travelers are the key target market.

CVO Daily Chart (Source - Thomson Reuters)

CVO Daily Chart (Source - Thomson Reuters)

We believe the strong growth in outbound travel is primarily a function of four key factors which have all been positive contributors to the quantum of growth: 1) Evidence suggest that there has been a material reduction in long haul international airfares over the last ten years. In broad terms this is largely a function of increasing competition in the global airline segment and we expect this trend to continue. 2) Australian economy has been one of the standout performers among the developed economies over the last ten years and this has undoubtedly contributed to increased level of international travel. 3) In general terms a higher domestic currency increases the incentive to travel internationally. 4) We also note an increase in offshore airlines now flying to Australia compared to levels ten years ago.

CVO is the largest player in the $800m Travel Insurance market in Australia with a 40% market share. The business currently distributes its products through multiple channels including travel agents, intermediary partners and online through its own website. The flight Centre relationship is particularly significant give it has been in existence since 1991 and contributes around 25% of group EBITDA. We view this arrangement as a major positive for the company given the fact that FLT remains the largest travel agent in Australia with a dominant brand and enviable market position. We also note the nature of the arrangement with FLT is a joint venture style agreement which ensures strong alignment of interests and an increasing likelihood the deal will be extended.

CVO reiterated its guidance of +$50.1m EBITDA for FY14 in June. As per the reiteration 2H14 EBITDA is close to $26m Vs $27m budgeted. CVO launched travel insurance sales in China via a foundation partnership with one of China’s leading online travel agents, Qunar. Recently Qunar’s online traffic exceeded Ctrip (largest by revenue) which recently recorded 197m monthly average visits. China is the third largest travel insurance market in APAC behind Japan and Australia, growing at more than 25%. To put into perspective, Chinese travel insurance gross written premium is expected to exceed Australia by 2016 reaching US$1 billion from US$0.5 billion in 2012.

CVO benefits from steady grown in outbound leisure travel by Australians and leveraged to the travel propensity of a growing middle class in Asia. CVO’s competitive advantages lie in its specialty focus, scalable platform and capital light business model (claims risk outsourced) to deliver mutually beneficial outcomes with its product distribution partners. We put a BUY recommendation on the stock at the current price of $1.77.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.

Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).

The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.

Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.

The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...