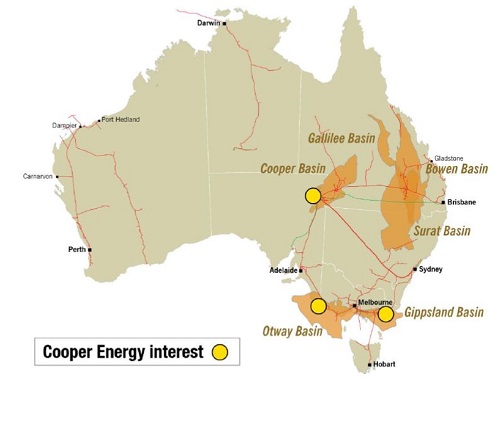

Company Overview - Cooper Energy is an ASX-listed exploration and production company that produces approximately 500,000 barrels of oil per annum and conducts exploration for oil and gas in a portfolio comprising prospective acreage in the Cooper, Otway and Gippsland basins Australia, South Sumatra, Indonesia and the Gulf of Hammamet, Tunisia.

Analysis – COE has delivered a record 1HFY2014 with NPAT of $13.6m up 198% on FY 13. Sales revenue was up 58% to $37m, driven by increased oil production of 0.3mmbbls and higher realised oil price of A$126.5/bbls. Increased production also lowered unit costs. The company finished the period in a strong financial position with cash and investments of $65.7m. FY14 guidance remains at the upper end of 0.54 – 0.58 mmbbls in line with our forecast of 0.58mmbbls. The company finished the period in a strong financial position with cash and investments of $65.7m after $32m in exploration and development expenditure. CAPEX guidance for FY2014 of $64m will see a further $18m in exploration and $10m in development expenditure in the 2H FY2014.

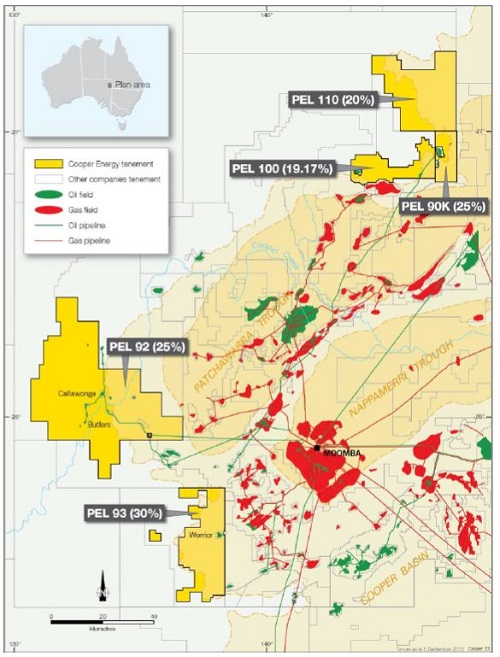

COE’s result was driven by sustained rates from PEL 92 on the back of 4 successful development wells, sustained output from the Worrior oil field and increased production in Indonesia. Worrior – 8 was a highlight confirming a new discovery in the Patchawarra which will be further appraised by the Worrior – 10 well. Following completion of a 3D survey in PEL 92 a 3 well exploration campaign is scheduled for the June Quarter. The wells will provide key catalysts testing upside from modern technology and the long term potential of the permit.

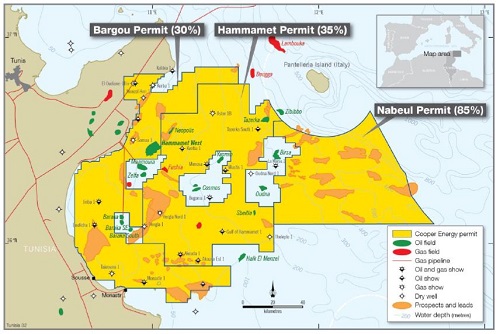

COE is set to commence exit from Tunisia. During the period the Bargou JV suspended operations at the Hammamet West – 3 side track and planning continues for a second side track as early as 2H CY 2014. An independent resource assessment of the discovery is expected to be completed shortly which will see the booking of a contingent resource and also facilitates the commencement of a formal divestment process of the Tunisian portfolio. COE will run this process in parallel with planning for the well and intends to divest either prior to or following the result. Success at Hammamet West in 2H 2014 and a timely exit from Tunisia has the potential to firm up significant value and focus attention on a strengthening domestic oil and gas growth.

COE equalized interests with Beach Energy (BPT) across the onshore Otway project with COE now holding a 30% interest across PEL 494 and 495 and recently spudded the Jolly-1 well to be followed by Bungaloo-1 in the March quarter. While a farm in to Bass Strait Oil Company’s (BAS) Gippsland Basin acreage was not approved, COE now holds 22.9% of BAS. Corporate highlights during the 1H included BPT increasing its stake in COE to 18.41%. While BPT declares its interest to be strategic, a full acquisition of COE makes sense increasing its interest in high margin Western Flank Oil production and in the Otway basin - assets it already owns and understands.

Cooper Basin Acreage (Source – Company Reports)

Cooper basin production and drilling were the key highlights of the result. Increased production output from PEL 92 was driven by a successful 4 well development campaign which included wells at Butlers and Callawonga. In PEL 93 production testing of the Worrior-8 well was a key highlight, intersecting oil in the McKinlay and Namur formations and discovering a new oil pool in the Patchawarra formation. A production test of the Patchawarra was aimed at testing whether sufficient gas was present for fuel usage at the field. However a significant oil leg also appears to have been discovered with a production test yielding a stabilized flow rate of 0.7mmscf/d and 670bopd.

Cooper Energy Portfolio (Source – Company Reports)

During the period COE and BPT executed a series of asset transactions to equalize and simplify interests across the onshore Otway play. COE acquired a 30% interests in PEL 494 from BPT and divested a 35% stake in PEL 495 to BPT bringing its interest in the key SA areas of the Penola Trough to 30%. While Otway is at an early stage of appraisal the asset is highly prospective and consistent with COE’s east coast gas focus strategically located adjacent to infrastructure to leverage off any success. In the Gippsland basin a farm in agreement to earn a 25.8% interests in VIC/P41 and 50% in VIC/P68 from BAS was not approved by BAS shareholders at its AGM and will therefore not proceed. However a revote would likely approve the deal following the exit of a large shareholder in BAS and COE recently increased its stake in BAS to 22.9% providing indirect leverage to this exploration footprint.

Tunisian Portfolio (Source – Company Reports)

During the 1H FY14 concluded operations at the Hammamet West-3 (Tunisia)discovery where elevated gas readings , oil samples in the cuttings at surface and significant losses to the formation provided encouragement that the well had encountered a highly fractured, porous and oil bearing reservoir. A number of attempts to production test the well were largely unsuccessful due to blockages. A JV decision was made to drill a second side track to the well which was then suspended due to the fact that the current rig on the site could not be contracted on acceptable terms for the duration of the planned activities. Planning continues to drill the second side track to the HW-3 well in 2H 2014 subject to the contracting of a suitable rig and government approvals. During the period COE commissioned an independent assessment of resources estimates for the discovery with the report expected to be completed imminently. The report will firm up and narrow resource estimates and is expected to include an updated Contingent Resource estimate. This will in turn allow for the commencement of the COE’s formal Tunisian divestment process which will run concurrently with drilling planning.

COE Daily Chart (Source – Thomson Reuters)

COE remains in a strong position with $65.7m in cash and liquid investments and its base business delivering cash flow and production growth. The company has assembled a diverse exploration portfolio with short to long term opportunities such as its early stage Otway acreage and its northern Cooper position which will likely attract more interest through 2H 2014 towards drilling in 2015. Upcoming drilling in the cooper basin will provide key catalysts testing the prospectively and hence the longer term sustainability of production from its acreage. We will be putting a BUY on the stock at the current price of $0.56.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Please wait processing your request...

Please wait processing your request...