Company Overview: Contact Energy Limited (ASX: CEN) is a New Zealand-based energy company which owns and operates long-life renewable generation assets. The company serves electricity, natural gas and LPG products to its customers. The company owns and operates 11 power stations and produces 83% of its electricity from renewable hydro and geothermal stations. As a retailer, the company sells products and services to thousands of individuals and businesses to meet their energy needs. CEN also trades a range of financial products to manage its risk and create value.

.png)

CEN Details

.png)

Improvement in Bottom-line: Contact Energy Limited (ASX: CEN) is a New Zealand-based energy company with a diverse mix of assets which helps it to maintain a reliable, affordable and environmentally sustainable electricity supply in the country. The company owns and operates low-cost, long-life renewable generation assets and is developing its consented geothermal development options. The company currently has a robust balance sheet with significant capacity to fund further renewable generation projects. CEN is focused on optimising its Customer and Wholesale businesses to deliver strong cash flows while continuing to investigate ways to optimise its portfolio of assets. Over the past few years, the company has witnessed significant improvement in its bottom line with net income increasing at a CAGR of 26.91% from FY15-FY19.

The company’s focus on continuous improvement has resulted in improved operational performance metrics. Moving forward, CEN intends to progress on its Decarbonisation strategy, as per which, it intends to develop options to enable the economic substitution of thermal generation with renewals and it also wants to partner with customers on mutually beneficial decarbonisation opportunities..png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

FY19 Performance Highlights: During FY19, the company delivered a solid financial result, improved capital efficiency, and deployed good risk management practices. Over the period, the company completed the sale of the Rockgas LPG business and Ahuroa Gas Storage (AGS) and received net cash proceeds of NZD 390 million.

For FY19, the company reported EBITDAF from continuing operations of NZD 505 million, up 12% on last year, driven by comparatively stronger hydro generation. Further, the company reported Underlying profit from continuing operations of NZD 166 million, up 51% on last year. During FY19, the company witnessed a 6% reduction in total ongoing cash operating costs and capital spend.

Over the year, the company’s wholesale business successfully managed periods of low hydro inflows and constrained gas supply, and reported EBITDAF of NZD 464 million, up NZD 67 million from NZD 397 million in FY18. Operating earnings (EBITDAF) in the company’s Customer business was NZD 67 million, down NZD 9 million from FY18, as continuing competitive pressures limited Contact’s ability to recover higher costs for electricity and distribution networks through customer price changes.

The company’s strong financial performance and optimisation of the portfolio, allowed it to increase its total dividend by 22% to NZ 39 cents per share, representing 82% pay-out of operating free cash flow per share. .png)

FY19 Results (Source: Company Reports)

H1FY20 Performance Highlights: For the first half of FY20, the company reported operating earnings (EBITDAF) of NZD 221 million, down by 21% on the previous corresponding period (pcp), due to rising thermal generation costs, lower sales to commercial and industrial customers and strong financial performance under unique wholesale market conditions in the prior period. Further, the company reported profit of NZD 59 million, down 40% on pcp.

During the period, the Average electricity tariffs for customers were lower than last year, despite increases in wholesale electricity costs. Operating free cash flow for 1H20 was NZD 120 million, down 39% on pcp, due to a combination of lower operating earnings (EBITDAF), partially offset by lower stay in business capital expenditure and interest costs.

EBITDAF in the Wholesale business reduced by NZD 39 million to NZD 204 million year-on-year, as production from hydro generation was down by 8%. Despite strong operational performance on many metrics and underlying efficiency improvements of 6%, EBITDAF in the Customer business was down NZD 18 million year-on-year to NZD 30 million, as rising input costs for electricity, gas, carbon and distribution networks were not recovered.

The company declared an interim ordinary dividend of NZ 16 cents per share, in line with the dividend paid in the pcp. .png)

H1FY20 Results (Source: Company Reports)

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms around 21.33% of the total shareholding.

.png)

Top 10 Shareholders (Source: Refinitiv, Thomson Reuters)

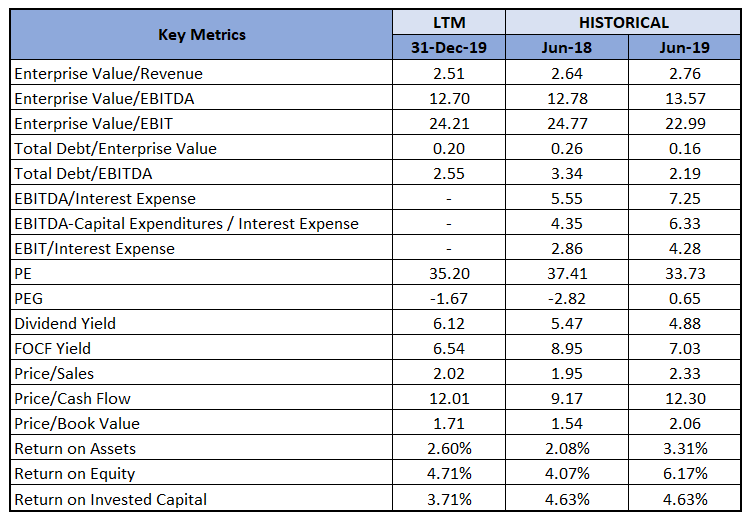

A Quick look at Key Ratios: For H1FY20, the company reported a gross margin of 28.5% and a net margin of 5.3%. The company’s asset turnover ratio stands at 0.22x, higher than the industry median of 0.08x. The company has an asset/equity ratio of 1.81x, lower than the industry median of 1.95x. Further, the company’s debt to equity ratio stands at 0.43x, slightly lower than the industry median of 0.46x. .png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Track Record of Paying Dividend: The company’s distribution policy provides clarity to investors and drives a strong capital discipline. Its strong balance sheet, high quality renewable generation assets and lean, low cost operations allowed it to pay total dividend of NZ 39 cents per share in FY19, 7 cents per share higher than FY18. For the first half of FY20, the company declared an interim dividend of NZ 16 cents per share, representing a pay-out of 95% of 1H20 operating free cash flow per share. For the full year 2020, the company expects to pay a total dividend of NZ 39 cents per share. From 2016 to 2019, the company’s dividends have grown at a CAGR of 14.47%. .png)

Dividend History (Source: Company Reports)

April 2020 Update: For the month of April 2020, the company’s customer business recorded Mass market electricity and gas sales of 300 GWh and Mass market electricity and gas netback of NZD 95.66/MWh. Further, the company’s Wholesale business recorded Contracted Wholesale electricity sales, including that sold to the Customer business, of 548 GWh and Electricity and steam net revenue of NZD 79.81/MW. During the month, the New Zealand electricity demand was down 13.7%, if compared to April 2019. It is to be noted that COVID-19 L4 and L3 lockdown were in place throughout April 2020. The cumulative 12 months demand for May 2019 to April 2020 was at 41,297 GWh, down by 0.5%, if compared to pcp..png)

National Demand Trend (Source: Company Reports)

Classified as Essential Business: As per new Covid-19 rules, the company was classified as an essential business. Therefore, the company was able to deliver its services, despite Covid-19 restrictions.

What to Expect: The company is currently executing various mitigation options to help move renewable electricity generation in the lower South Island north through the national transmission network and it is also working with commercial and industrial customers to deliver reductions to their carbon footprints by connecting them with low-carbon, reliable electricity.

Moving forward, the company is focused on delivering on its transformation programme to reduce controllable costs, and capture value from scale efficiencies through geothermal development and leveraging its customer systems and lean operating mode.

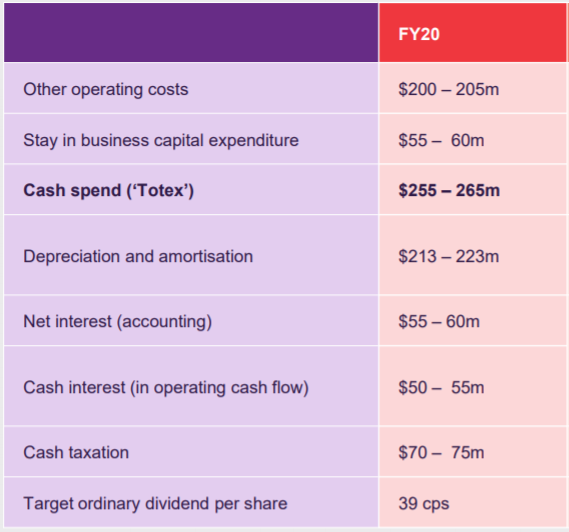

In FY20, the company expects cash spend to be in between NZD 255- 265 million. Further, it targets to pay a total dividend of NZ 39 cents per share in FY20.

FY20 Guidance (Source: Company Reports)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

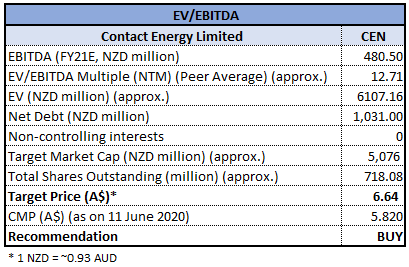

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: Over the past six months, the stock of CEN has corrected by 13.92% and is inclined towards its 52 weeks low price of $4.32, offering a decent opportunity for accumulation. The stock is trading at a P/E multiple of 34.6x with an annual dividend yield of 5.88%. We have valued the stock using EV/EBITDA multiple based illustrative relative valuation method and have arrived at a target price with low double-digit upside (in % terms). For the purpose, we have taken peers like AusNet Services Ltd (ASX: AST), Mercury NZ Ltd (ASX: MCY), Infratil Ltd (ASX: IFT) and Genesis Energy Ltd (ASX: GNE). Considering the company’s decent financial performance over the last few years, its track record of rewarding shareholders through dividends, and current trading levels, we give a “Buy” recommendation on the stock at the current market price of $5.820, down by 3% on 11 June 2020.

CEN Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...