Company Overview: Contact Energy Limited (ASX: CEN) is a diversified and integrated energy company which focuses on the generation of electricity and sale of electricity & gas in New Zealand. The company is led by an experienced team, committed to customers, communities, and shareholders. Notably, at the end of FY19, the company has 889 employees, 4 thermal stations, 2 hydro stations and net assets amounting to $2.8 billion. CEN leverages its relationships, networks, partnerships and culture in order to create brand value and deliver on its strategy.

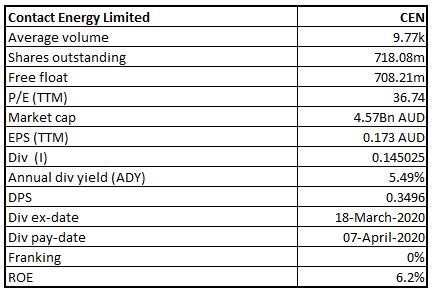

CEN Details

Long-term Growth Story Intact: Contact Energy Limited (ASX: CEN) is a diversified and integrated energy company which focuses on the generation of electricity and the sale of electricity & gas in New Zealand. In FY19, the company successfully executed transformation programme, which included sector leading reductions to operating and capital expenditure, deepening of relationship with the customers and simplification of the portfolio of assets. Statutory profit for the year ended June 30, 2019 stood at $345 Mn which is $213 Mn higher than the prior corresponding period after realising a gain on the sale of Rockgas Limited and AGS facility amounting to $170 million. EBITDAF from continuing operations rose $56 million or 12%, and the figure stood at $505 million because of robust operational performance in the wholesale business. During the same period, operating free cash flow increased by 13% to $341 million due to higher operating earnings, lower stay in business capital expenditure and interest costs which were partially offset by higher cash tax.

The company’s portfolio of long-life renewable generation assets has been providing the Board confidence to distribute the ordinary dividends that target a pay-out ratio of 100% of expected operating free cash flow. For FY19, the company managed to declare dividends amounting to 39 cents per share as compared to 32 cents per share declared in FY18. The company’s customer business continues to reduce the cost to serve while improving the experience of the customer. Contact’s Wholesale business has been working with the business customers, partners as well as suppliers to decarbonise NZ’s energy sector. The volatile wholesale market conditions driven by a shortage of gas reflect the value of flexible and diverse generation assets, robust risk management, continuous improvement programme and access to stored gas. Considering the focus on transformation programme to reduce controllable costs, seek opportunities to capture value from scale efficiencies through brownfield geothermal development, and decent dividend-related parameters, we have valued the stock by using a relative valuation method, i.e., Price to cash flow multiple and arrived at a target price of lower double-digit growth (in % terms)..png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Contact Energy Limited:.png)

Top 10 Shareholders (Source: Thomson Reuters)

Overview of Key Margins: The company’s gross margin stood at 28.5% in 1H FY20, which is marginally higher than 2H FY19 figure of 28.1%. Notably, its EBITDA margin stood at 19.9% as compared to 2H FY19 figure of 19.6%. CEN’s percentage long-term debt to total capital stood at 23% which implies a fall from 2H FY19 figure of 25% and, therefore, it can be said that the company reduced its exposure towards long-term debt. Therefore, it can be said that the company can focus more on its long-term growth objectives..png)

Key Metrics (Source: Thomson Reuters)

Monthly Operating Report for January 2020: The company has released its monthly operating report for the month of January 2020, and its customer business recorded mass market electricity and gas sales of 297 GWh as compared to January 2019 figure of 281 GWh. However, for the same month, mass market electricity and gas netback stood at $88.97/MWh, while in January 2019 it was $92.25/MWh. With respect to wholesale business, it was mentioned that contracted wholesale electricity sales, which includes that sold to customer business, stood at 579 GWh..png)

Wholesale Market (Source: Company Reports)

Analysing 1H FY20 Performance of CEN: The company reported statutory profit for six months ended December 31, 2019, amounting to $59 million, which was $217 million lower as compared to prior corresponding period that included Rockgas profit of $10 million and $172 million gain on sale of Rockgas and Ahuroa gas storage. During the same period, the company’s EBITDAF from continuing operations fell by $57 million, or 21%, and the figure stood at $221 million because of rising thermal generation costs, lower sales to commercial and industrial customers as well as robust financial performance under unique wholesale market conditions in the previous period. However, operational improvements along with portfolio changes led to a further reduction in other operating costs of $8 million, a fall of 7% on a year ago. EBITDAF in Wholesale business fell $39 million to $204 million on the YoY basis, as production from the hydro generation declined by 8%. Also, thermal generation costs rose by 10%, because of gas, carbon and gas storage facility costs.

As per the key personnel of CEN, NZ was undergoing “a transformation” from reliance on fossil fuels to renewable electricity. This transformational shift weighed on Contact’s near-term profitability because of the increase in thermal costs, but over the long term, the company is well-placed to connect the customers with renewable energy. The company anticipates to drive reductions in costs and deliver robust returns to the shareholders at the same time it develops the large-scale consented geothermal development at Tauhara. This would help in the reduction of the nation’s carbon emissions.

CEN Secures Agreement with Gas Producer: Contact Energy Limited inked an agreement with OMV New Zealand to secure 37 petajoules (or PJ) of gas to be delivered from 2021 to 2025. OMV also notified CEN that it would supply at least 6.3PJ of Contact’s 10PJ entitlement from Maui in 2021. Additionally, CEN entered into an additional new 3.6PJ gas agreement with an undisclosed third party for the delivery in the year 2020.

Increased Dividends Declared in FY19: In FY19, the company declared dividend amounting to 39 cents per share as compared to FY18 figure of 32 cents per share. For 1H FY20, the company declared interim dividend amounting to 16 cents per share which are imputed to 63% or 10 cents per share for the qualifying shareholders. It reflects the pay-out of 95% of 1H FY20, operating free cash flow per share. Notably, the NZD/AUD exchange rate used for payment of Australian dollar dividends is expected to be set on March 30, 2020..png)

Ordinary Dividends (Source: Company Reports)

Between FY16- FY19, the company’s dividends have increased from 26 cps to 39 cps and, therefore, it can be said that CEN is capable to delivering decent returns to its shareholders in different market conditions. Thus, CEN might attract the attention of dividend-seeking investors moving forward. For FY20, the company is targeting ordinary dividend amounting to 39 cents per share which would be the same as compared to FY19.

What to Expect From CEN: For the near-term, Contact Energy Limited is expected to focus on managing the wholesale market volatility and deliver the value. The company’s focus towards delivering value largely revolves around deployments towards digital and data in order to further reduce costs and develop new and innovative propositions. However, it also revolves around continued focus towards controllable cost reduction. For the medium term, the priorities include capturing scale efficiencies and decarbonisation..png)

Outlook (Source: Company Reports)

CEN is expected to post other operating costs in the range of $200 million – $205 million and depreciation and amortisation of between $213 million – $223 million. As mentioned earlier, it is targeting ordinary dividend per share of 39 cps. .png)

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology: Price to Cash Flow Based Relative Valuation.png)

Price to Cash Flow Based Relative Valuation (Source: Thomson Reuters), *1 NZD = ~0.95 AUD as on 05 March 2020

Stock Recommendation: Between FY16- FY19, the company has witnessed a CAGR of 4.38% in its total revenues and, therefore, it can be said that CEN is possessing decent capabilities to garner revenues which could further strengthen its financial footing. The company’s key personnel have stated that CEN is focussed on delivering on the transformation programme in order to reduce controllable costs, and capture value from scale efficiencies with the help of geothermal development and leveraging the customer systems and lean operating model. The company’s policy is to shell out ordinary dividends targeting the pay-out ratio of 100% of operating free cash flow which is adjusted for the anticipated medium-term stay-in-business capital expenditure, mean hydrology along with consideration of sustainable financial structure that includes targeting of the long-term credit rating of BBB. Considering the focus on transformation programme to reduce controllable costs, seek opportunities to capture value from scale efficiencies through brownfield geothermal development, and decent dividend-related parameters, we have valued the stock by using a relative valuation method, i.e., Price to cash flow multiple and arrived at a target price of lower double-digit growth (in % terms). For the said purpose, we have considered Mercury NZ Ltd (ASX: MCY), Spark Infrastructure Group (ASX: SKI) and Meridian Energy Ltd (ASX: MEZ), as peers. Thus, we give a “Buy” rating on the stock at the current market price of $6.330 per share, down by 0.628% on 5th March 2020.

CEN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...