Kalkine has a fully transformed New Avatar.

Company Overview: Contact Energy Limited is an energy generator and digital retailer, which is engaged in providing electricity, natural gas and liquefied petroleum gas (LPG), and broadband services. It generates electricity through hydro, geothermal and thermal sources. The Company operates through two segments: Generation segment and Customer segment. The Generation segment is engaged in the business of selling electricity to the wholesale electricity market and to the Customer segment. The Customer segment delivers, services and distributes energy to customers. It sells electricity, gas and LPG products and services to residential, small business, commercial and industrial customers. The Company's stations include Ahuroa and Stratford in Taranaki; Ohaaki, Poihipi and Te Rapa in Waikato, Te Huka and Te Mihi in Taupo Wairakei in Taupo, and Whirinaki in Hawke’s Bay. It is also involved in the development of geothermal energy projects.

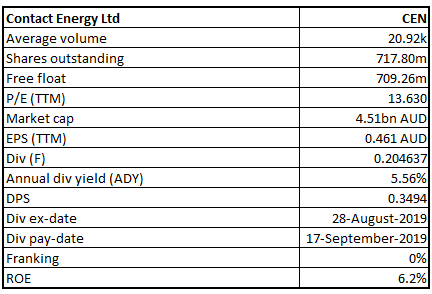

CEN Details

Decent Performance in FY19: Contact Energy Limited (ASX: CEN) is a mid-cap energy company with the market capitalisation of ~$4.51 Bn as of 21 November 2019. It is one of the New Zealand’s biggest electricity generators and digital retailers of natural gas and electricity. The company reported a decent set of numbers for the period ended June 30, 2019 (FY19), wherein revenue increased by 14.3% to $2,460.0 million as compared to the prior year. Statutory profit of the company stood at $345 million, which is $213 million higher than prior corresponding period after realising the gain on sale of Rockgas and AGS of $170 million. The company’s EBITDAF from continuing operations rose $56 million, or 12%, and the figure stood at $505 million because of robust operational performance in Wholesale business. It was further added that operational improvements led to a further reduction in other operating costs of $11 million, which were 5% down on prior comparative period. The company’s operating free cash flow rose to $341 million, reflecting an increase of 13% on a YoY basis on the combination of higher operating earnings, lower stay in business capex as well as interest costs, which were partially offset by the higher cash tax. The company’s top line has witnessed a CAGR growth of 4.38% in the time span of between FY16- FY19 and, therefore, it can be said that CEN is possessing decent capabilities to garner revenues. However, between FY15- FY19, the company’s bottom line has encountered a CAGR growth of 26.91%.

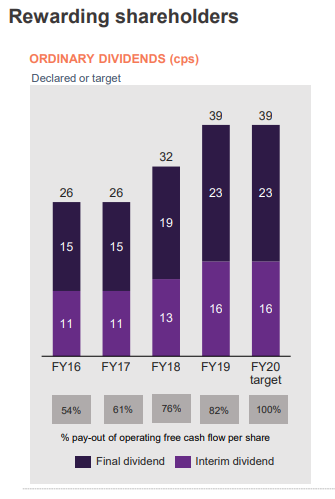

The company’s portfolio of long-life renewable generation assets has been providing Board with confidence to shell out ordinary dividends which target the pay-out ratio of 100% of expected operating free cash flow. For FY19, this equated to 39 cents per share, which implies a rise as compared to 32 cents per share, which were declared in FY18. Thus, the company has been rewarding its shareholders with an increase in dividends. The company added that robust financial performance as well as optimisation of portfolio resulted in higher dividends. It was mentioned that the company’s Wholesale business has been working with business customers, partners, and suppliers to decarbonise New Zealand’s energy sector. The volatile wholesale market conditions because of a shortage of gas have shown the value of flexible as well as diverse generation assets, robust risk management, continuous improvement programme and an access to the stored gas.

Considering the maintenance of financial discipline, enhanced customer advocacy and focus of the company towards rewarding shareholders, the company might gain traction among the market participants. The stabilised position of CEN’s balance sheet, decent liquidity levels, focus on reducing operating costs, operational and capital efficiency, and focus on disposing of non-core activities are expected to act as tailwinds.

.png)

Key Financial Metrics (Source: Company Reports, Thomson Reuters)

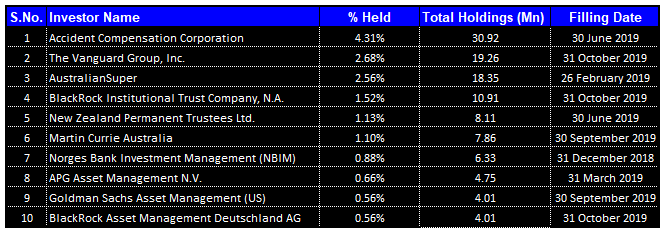

Top 10 Shareholders: The following image provides a broader overview of the top 10 shareholders in Contact Energy Limited:

Top 10 Shareholders (Source: Thomson Reuters)

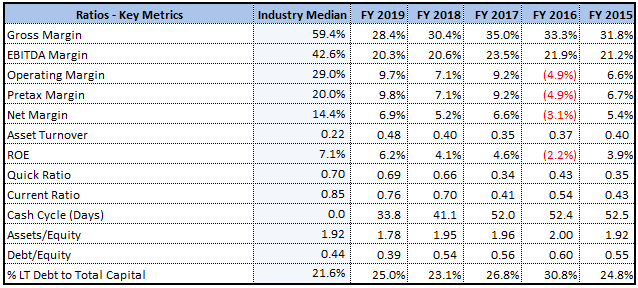

Improvement in Net Margins: The company’s net margin stood at 6.9% in FY19, which is higher than FY18 figure of 5.2% and, thus, it can be said that CEN has improved its capabilities to convert the top-line into the bottom-line. Additionally, CEN’s operating margin stood at 9.7% in FY19 as compared to 7.1% in FY18. CEN’s RoE stood at 6.2% in FY19, which is higher than FY18 figure of 4.1% and, therefore, it can be said that CEN has been providing decent returns to its shareholders and it has a focus on improving shareholder value.

Current ratio of CEN stood at 0.76x in FY19, which is higher than FY18 figure of 0.70x, and, therefore, it can be said that the company’s capabilities to meet its short-term obligations have improved. Moreover, decent liquidity levels reflect that CEN could make deployments towards strategic activities that could help in achieving long-term growth. CEN’s Debt/Equity ratio stood at 0.39x, which is lower than FY18 figure of 0.54x, thus, it can be said that the company has been deleveraging its balance sheet. Generally, lower debt on the balance sheet reflects stability, and this might help a particular company to focus on long-term strategic growth objectives.

Key Ratios (Source: Thomson Reuters)

Appointment of New Chief People Officer: Contact Energy Limited has made an announcement that the search for a new Chief People Officer has been concluded with an appointment of Jan Bibby. Jan was General Manager, Human Resources at Vodafone New Zealand before heading to the UK as group Head of Organisation Effectiveness for Africa, Middle East and the Asia Pacific.

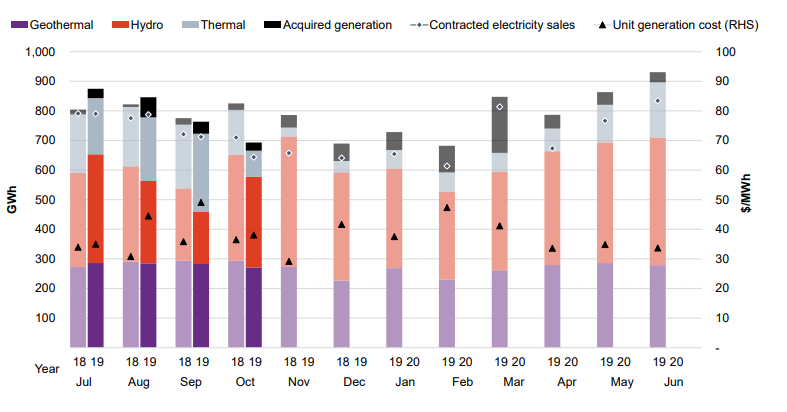

Overview of October 2019 Month: In October 2019, the Customer business recorded mass market electricity and gas sales of 379 GWh and mass market electricity and gas netback of $87.32/MWh. With respect to Wholesale business, it was mentioned that contracted Wholesale electricity sales, which includes that sold to Customer business, stood at 644 GWh and electricity and steam net revenue amounted to $73.02/MWh. The following picture provides an overview of Wholesale business performance:

Wholesale Business Performance (Source: Company Reports)

Well-Positioned to Meet Electricity Demand: The Wholesale business of Contact Energy Limited has been working with business customers, partners as well as suppliers to decarbonise New Zealand’s energy sector. The volatile wholesale market conditions because of the shortage of gas have shown the value of flexible as well as diverse generation assets, robust risk management, continuous improvement programme, and access to the stored gas. The generation EBITDAF rose $67 million, and the figure stood at $464 million in 12 months to June 30, 2019, as compared to the same period of the previous year, as the production from hydro generation rose 22%, or 752GWh post a dry FY18 in Contact’s Clutha catchment. Additionally, Contact Energy Limited supported the market by accessing gas stored in AGS (Ahuroa Gas Storage) and offering additional thermal generation above the contracted sales in order to meet wholesale spot demand.

The company’s key personnel has stated that New Zealand has been undergoing the transformation from reliance on fossil fuels to renewable electricity. The company is well-positioned when it comes to meet the expected growth with respect to electricity demand, which would be resulting in meaningful reductions to nation’s carbon emissions by developing the largescale consented geothermal development options, which are being backed by geothermal capability and robust balance sheet.

Targeting 100% Dividend Payout: The company stated that asset sales significantly improved strength of the company’s balance sheet and positions it well for future investment. Considering the continued confidence in the business’s ability to generate cash flow, the Board of the company has changed its distribution policy so that it can target the payout of 100% of the anticipated operating free cash flow. As a result, the Board of CEN has declared a final dividend for FY19 amounting to 23 cents per share, which is up 21% on a YoY basis, and the company is targeting full-year FY20 dividend amounting to 39 cents per share, which is in line with FY19.

The company added that robust financial performance as well as optimisation of portfolio resulted in increased dividends. It was added that robust balance sheet, high quality renewable generation assets as well as lean, low cost operations have allowed increasing dividends to the shareholders, and the FY19 ordinary dividend rose to 39 cents per share, which is 7 cents per share higher than FY18.

Distributions (Source: Company Reports)

What to Expect from CEN Moving Forward: After lowering cost of geothermal since the last build, the company has been taking the next step towards developing geothermal power station project that it has consented at Tauhara by committing to drilling the series of 4 appraisal wells. The company’s commitment to reducing the carbon emissions has not been limited to supply-side, and it is actively partnering with the Commercial and Industrial customers via investment in Simply Energy which happens to be an innovative energy solutions company that utilises demand-side management tools in order to assist the customers to switch to electricity from current energy sources, help them in becoming more energy efficient, reducing their costs and cutting their carbon emissions.

The key personnel of CEN has stated that the company remains focussed towards delivering on the transformation programme in order to reduce the controllable costs, as well as seek opportunities to capture value from the scale efficiencies via brownfield geothermal development and by utilising the customer systems and lean operating model to improve the returns.

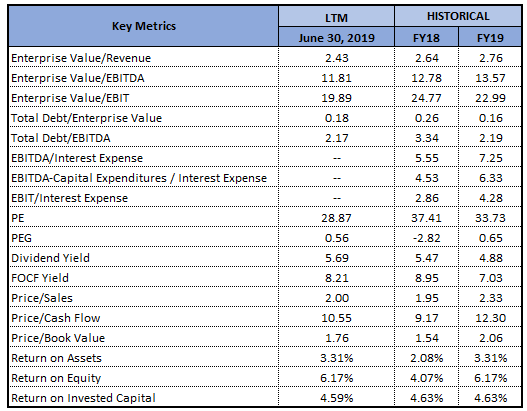

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

Method 1: EV/Sales Multiple Approach

.png)

EV/Sales Multiple Approach (Source: Thomson Reuters), *1 NZD equals 0.94 AUD

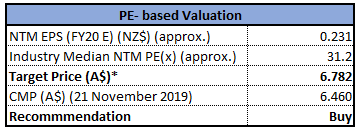

Method 2: PE- based Valuation

PE- based Valuation (Source: Thomson Reuters), *1 NZD equals 0.94 AUD

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM: Next Twelve Months

Stock Recommendation: In the span of one year, the stock price of CEN has witnessed a rise of 17.37% in the span of previous one year while, on YTD basis, it rose 14.03%. The delivery of operational efficiencies, quality of the generation assets as well as balance sheet strength were improved by completion of 2 major transactions in the year. These transactions were wrapping of sale of Ahuroa Gas Storage as well as sale of Rockgas LPG. It was added that both of these transactions give significant flexibility for the business. The company has been focusing on operational improvement, which could help it in achieving decent growth moving forward. Based on the foregoing, we have valued the stock, using two relative valuation methods, i.e., EV/Sales multiple, price to earnings multiple, and arrived at a target price of high single-digit to low double-digit growth (in % term). Hence, we give a “Buy” rating on the stock at the current market price of $6.460 (up 2.866% on 21 November 2019).

CEN Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...