Kalkine has a fully transformed New Avatar.

Company Overview: Compumedics Limited (ASX: CMP) is involved in the R&D, manufacture, and distribution of medical equipment. CMP operates its business in the USA, Asia Pacific, Australia, and Europe and sells products relating to sleep diagnostic systems, clinical EEG systems, brain monitoring systems, supplies and technical service and support. The company is also engaged in examining neurological syndromes containing long-term epilepsy monitoring (LTEM). Compumedics Limited is the number one technological leader in Australia, Japan, China, and the USA. The company was incorporated in 1987 and was listed on ASX on 21 December 2000.

.png)

CMP Details

.PNG)

CMP Rides on Product Roll-Out & Higher Investments: Compumedics Limited (ASX: CMP) is involved in the development, production, manufacturing, and marketing of medical devices used for the analysis of brain and sleep disorders, and to investigate ultrasonic blood-flow applications. CMP delivered robust underlying financial and operational performance in FY19. The company remains focused on generating profits from its blue-chip client-based core business, along with maintaining sustained strong investment in research and development. The ongoing immense investment in the core business growth, along with commercial activation of next-generation growth platforms, resulted in sound profitability across its business. Compumedics Limited is focused on operational programs designed to drive improved efficiencies, capable of enhancing sales margins and product quality. In FY19, revenue of the company stood at $41.5 million, increasing 12% year over year. Reported EBITDA for the year stood at $5.9 million, up by 40% year over year. EBITDA growth was due to higher revenue base and ongoing operational efficiency. In FY19, net profit after tax (NPAT) stood at $4 million, up 43% year over year.

In a recent update, the company stated that it might face some short-term unfavourable impacts on the business due to COVID-19 control actions. However, it is taking the necessary measures to develop the required contingency plans to manage the impact of the crisis. The company also updated that it has sufficient inventory levels to meet the expected demand. While the company has withdrawn the guidance for FY20, it continues to pursue additional MEG (Magnetoencephalography) system sales after obtaining the FDA clearance for the Orion MEG system in February 2020.

Over the time span of 4 years covering FY15-FY19, the company saw a compound annual growth rate of 5.5% in revenue. Over the above stated period, the company’s earnings per share performance also increased, depicting a strong financial model, driven by growth in the group’s key markets around the world and the partial invoicing of the MEG sale. The company expects higher earnings per share in the coming period. Further, steady growth from China in sleep diagnostics with a greater emphasis on the neurodiagnostic monitoring market will aid the company’s organic growth and value realization.

.png)

Growth in Basic Earnings Per Share (Source: Company Reports)

Going forward, the company expects key growth opportunities to deliver an increase in revenues and earnings. It remains on track for the installation of the dual-helmet Dewar at Barrow Neurological Institute (BNI) in Phoenix along with numerous field trials of the Somfit technology. These activities will seek strategic alliances and partnerships, which are likely to gain momentum.

1HFY20 Key Highlights: During the six months ended 31 December 2019, the company reported revenue amounting to $18.3 million, as compared to $18.7 million in the prior corresponding period. This was mainly due to the lesser sales booking in the US. The company was engaged in investing in new products for the core business and took orders worth $18 million in 1HFY20. Asia-based sales, mainly out of China, continued to grow and was 7% higher for shipped and invoiced revenues on a year over year basis. EBITDA for the period stood at $1.2 million, down from $1.5 million, because of the shortfall in sales in the US. Net profit after tax (NPAT) stood at $0.2 million.

.png)

1HFY20 Financial Highlights (Source: Company Reports)

Key Growth Core Strategies: During 1H20, the company witnessed robust growth in its key Asian markets and in Europe through its Germany-based business, DWL. The company continues to invest significantly in new products for the core business as well as pursue MEG and Somfit opportunities. During the period, the company made shipments of neurological devices to new Japanese distributor, Fukuda Denshi. It has also come up with growth initiatives in eHealth and has expanded the NeXus 360 platform in Australia and the USA. The company also reported continuous success across the core and the new breakout businesses’ financial, commercial activation, technological and regulatory functions, which positions the company to garner additional revenue going forward. Further, the company received approval from the FDA for the clearance of the Orion MEG system. This, in turn, will aid CMP to pursue near-term sales opportunities for clinical as well as research applications of the MEG system.

Results for the core Diagnostic Medical Devices: The business includes the technology and products sold worldwide for the diagnosis and monitoring of sleep disorders and neurological illnesses. During 1H20, Revenue from Medical Diagnostic Devices stood at $18.3 million. EBITDA in 1HFY20 came in at $2 million, as compared to $2.8 million in FY18. NPAT for the period stood at $1 million, as compared to $2.1 million in the prior corresponding period.

.png)

Divisional Highlights (Source: Company Reports)

Balance Sheet & Cash Flow Highlight: CMP ended the period with cash and cash equivalents of $3.3 million. The company’s total borrowings at the end of 1HFY20 came in at $1.8 million, marginally up from $1.6 million as at 30 June 2019. Operating cash flows for 1HFY20 were in line with the previous year and stood at $2 million. Net cash outflow from investing activities amounted to $3.2 million in 1HFY20 as compared to an outflow of $1.4 million in 1HFY19.

.png)

Cash Flow Details (Source: Company Reports)

The company is taking initiatives to roll-out new product platform to significantly expand its addressable market. It remains on track to develop its neuro-diagnostic business in the US and China, as well as other key markets across the globe. The company’s OktiTM product is a market-leading solution for ambulatory, long term, high density, and research applications. It is a new generation of premium neuro and sleep diagnostic remote or ambulatory portable monitoring. The company also plans to launch two new major product platforms in the coming 12 months for home sleep-testing for the sleep market.

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together forms the total shareholding of around 71.53%. Burton (David) holds the maximum shares in the company with the percentage holding of 55.34%. Teijin Pharma Limited is the second-largest shareholder, with a holding of 4.68%.

.png)

Top Ten Shareholders (Source: Refinitiv, Thomson Reuters)

Key Metrics: In 1HFY20, the company had a gross margin and EBITDA margin of 54% and 8.8%, respectively. In the same time span, debt-to-equity multiple of the company stood at 0.14x, lower than the industry median of 0.19x, demonstrating a stable financial position in comparison to its peers.

.png)

Key Metrics (Source: Refinitiv, Thomson Reuters)

Outlook: Following each of the challenging periods, the company has navigated its way and came through as a stronger business. Based on the company’s existing distribution network along with the outstanding ongoing performance from the DWL® ultrasonic Doppler blood flow division, the company will further strengthen growth. CMP remains on track to develop its technologies around the 3D Transcranial Colour Doppler (3D TCCD)/Duplex imaging. With the above scenario in place, the company has entered this unprecedented period with a relatively strong and sound business base and is likely to retain its existing customer base. It expects to maintain dominant growth momentum in the long-term.

.png)

Key Valuation Metrics (Source: Refinitiv, Thomson Reuters)

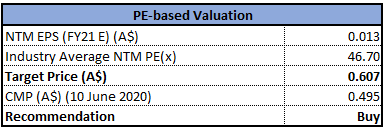

Valuation Methodology: Price to Earnings Multiple Based Relative Valuation (Illustrative)

Price to Earnings Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company is currently trading below the average of its 52-week low and high trading range of $0.25 - $0.96, respectively. The stock has a market cap of ~$87.7 million. The stock of CMP gave a negative return of ~39.63% in the last six months and a negative return of ~10% in the one-month period. While the company has revoked its financial outlook due to coronavirus impact, it is actively pursuing certain business activities and is preparing to gain momentum despite the gloom in the global markets. We have valued the stock using a P/E based illustrative relative valuation method and arrived at a target price with an upside of lower double-digit (in percentage terms). Considering the current trading levels, resilient business model and decent growth opportunities, we recommend a “Buy” rating on the stock at the current market price of $0.495 on 10 June 2020.

%20(002).png)

CMP Daily Technical Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...