Kalkine has a fully transformed New Avatar.

Company Overview: Compumedics Limited is engaged in the research, development, manufacture and distribution of medical equipment. The Company's segments include USA, Australia and Asia Pacific, and Europe. The USA business includes the United States, Canada and Latin America. The Australia and Asia Pacific segment includes all countries in the Asia Pacific region. The Europe segment includes all countries in the European region, and all Middle Eastern countries. It sells all of its product offerings, including sleep diagnostic systems, clinical electroencephalogram (EEG) systems, brain monitoring systems, ultra sonic blood-flow systems, supplies and technical service and support. The USA business also includes that sleep diagnostic services business. Its product, Somfit, is a fitness tracker. The Somfit tracks the user's sleep, collecting medical grade data to provide true sleep insights. The Company also focuses on the development of neurodiagnostic, Neuroscan research and consumable businesses.

.png)

CMP Details

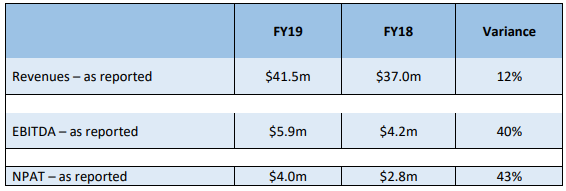

Robust Sales in China, Germany-based DWL and the USA: Compumedics Limited (ASX: CMP) is engaged in the development, production, manufacturing, and marketing of medical devices utilized for analysis of brain and sleep disorders, and to examine ultrasonic blood-flow applications. The company is also involved in monitoring neurological syndromes containing long-term epilepsy monitoring (LTEM). Compumedics Limited is the number one technological leader in Australia, Japan, China, and the USA. The company was incorporated in 1987 and was listed on ASX on 21 December 2000. For the year ended 30 June 2019, the company reported revenue of $41.5 million, up around 12% year over year. Reported EBITDA for the year stood at $5.9 million, up around 40% year over year. Revenue increased on the back of growth across key international markets along with accelerated partial booking of the first MEG sale.EBIT for the year came in at $5.4 million, up from $3.7 million reported in FY18. In FY19, net profit after tax (NPAT) came in at $4 million as compared to $2.8 million reported in FY18 and represented an increase of 43% year over year. Earnings per share for the period was 2.3 cents, up from 1.6 cents in FY18, primarily due to higher sales in China, Germany-based DWL and the USA, all delivering year over year growth.

For FY20, the company expects revenue from the core business to be in the range of $42 million to $44 million, while EBITDA is expected between $6.5 million and $7.5 million. The company expects H1FY20 results to be released on 25 February 2020. The company expects unaudited H1FY20 revenue at $17.7 million, as compared to $18.7m in H1FY19. The Company is also progressing towards the FDA proposal for the existing MEG device installed at BNI.

The company witnessed a compound annual growth rate of 5.5% in revenue over the period covering FY15-FY19. Over the above stated period, the company reported continuous success across the core and the new breakout businesses’ financial, commercial activation, technological and regulatory functions, which position the company to garner additional revenue going forward. The business strengthened as the company is witnessing growth across the USA based business, the new German market, and constant evolution in France. Further, steady growth from China in sleep diagnostics with a greater emphasis on the neurodiagnostic monitoring market will aid the company’s organic growth and value realisation.

.png)

Growing Revenues in Core Business (Source: Company Reports)

FY19 Performance Driven by Robust Sales in China, Germany-based DWL and the USA: During the period, revenue came in at $41.5 million, increasing 12% year over year. Reported EBITDA for the year stood at $5.9 million, soaring 40% year over year. EBITDA growth was due to higher revenue base and ongoing operational efficiency. In FY19, net profit after tax (NPAT) stood at $4 million, up from $2.8 million reported in FY18, representing an increase of 43% year over year.

FY19 Results (Source: Company Reports)

Key Growth Core Strategies Aided Revenues: Growth across key markets and the additional partial booking of the first MEG sale, aided profitability in FY19. Moreover, the company is actively pursuing new MEG sales. Furthermore, an increase in sales from the Asian market and the DWL business in Germany, the USA, and other regions were key positives. The company has also come up with growth initiatives in eHealth. It has expanded the NeXus 360 installation base with more than 30 sites and over 210 beds in Australia and the USA. The NeXus 360 platform provided revenue of $600K in FY19. Total signed contract value recorded annual subscription fees of more than $1 million. The number of patients recorded on the NeXus 360 platform is more than 45,000, helping them with both sleep and neurodiagnostic applications.

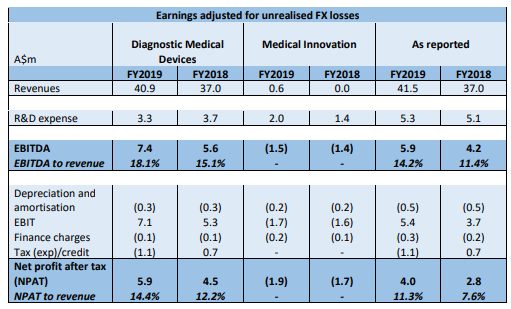

Results for the core Diagnostic Medical Devices: The business includes the technology and products sold worldwide for the diagnosis and monitoring of sleep disorders and neurological illnesses. Revenue from Diagnostic Medical Devices in FY19 came in at $40.9 million. Sales orders in FY19 came in at $40.5 million, which excluded MEG sales. NPAT for the period stood at $5.9 million, up from $4.5 million in FY18. EBITDA in FY19 came in at $7.4 million, up from $5.6 million in FY18.

Divisional Highlights (Source: Company Reports)

Balance Sheet Position: At the end of the year, the company reported cash and cash equivalents of $4.59 million. The company’s total borrowings at the end of the year came in at $1.59 million, down from $1.89 million as at 30 June 2018. Overall, the company has depicted significant leverage improvement since FY15, on account of the capital recycling program. Notably, the company has a net debt to equity ratio of -11% in FY19.

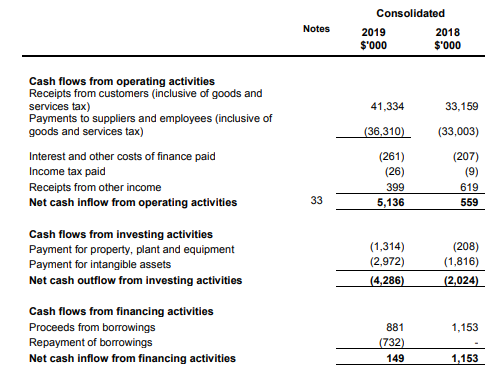

Cash Flow Position: Operating cash inflow in FY19 came in at $5.136 million as compared to $559K in FY18. Net cash outflow from investing activities amounted to $4.286 million in FY19 as compared to $2.024 million in FY18. Net cash provided by financing activities stood at $149K in FY19 as compared to an inflow of $1.153 million in the previous year.

Cash Flow Details (Source: Company Reports)

In FY19, core Asia business, and China in specific, witnessed robust growth of 26% in revenue on a year over year basis. Core DWL business witnessed an increase of 17% in revenues and US business rose approximately 16% on a year over year basis. In FY19, the company undertook initiatives for the first phase of the MEG sale to Barrow Neurological Institute in Phoenix, Arizona, USA. The company has also planned for the second and final phase at the beginning of 2HFY20. The company’s Somfit device (consumer application) product development considerably improved in FY19. The company plans to roll out OktiTM this year, a new generation of premium neuro and sleep diagnostic remote or ambulatory portable monitoring. The Company remains on track to develop its technologies around the 3D Transcranial Colour Doppler (3D TCCD)/Duplex imaging, to leverage commercial opportunities. With the above scenario in place, the company is confident about retaining its existing customer base and expects to maintain dominant growth momentum in FY20.

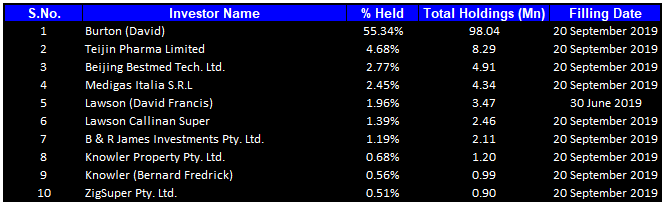

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 71.53% of the total shareholding. Burton (David) is the entity holding maximum shares in the company at 55.34%. Teijin Pharma Limited is the second-largest shareholder, with a holding of 4.68%.

Top Ten Shareholders (Source: Thomson Reuters)

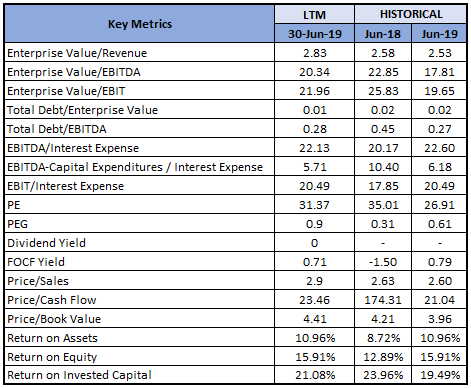

Key Metrics: In FY19, the company had a gross margin and EBITDA margin of 59.7% and 14.2%, which was higher than the margins of FY18, representing decent fundamentals. The company had negligible debt during the year with a debt-to-equity multiple of 0.06x, as compared to the industry median of 0.28x, demonstrating a better financial position in comparison to peers. Net margin of the company was reported at 9.7%, depicting an improvement on the prior corresponding period margin of 7.5%.

Key Metrics (Source: Thomson Reuters)

Outlook: On 13th January 2019, the company stated that on the back of certain delayed sales orders being accepted in the US, revenue for the first half of FY20 is expected to be roughly $17.7 million, as compared to $18.7 million in 1HFY19. Growth in revenue is expected in Asia, the Middle East, and DWL businesses. For FY20, the company expects revenue from the core business in the range of $42 million to $44 million, while EBITDA is expected between $6.5 million and $7.5 million. The company expects the Somfit device to be used by the Melbourne-based rugby team for the second season in elite sports application mode. Based on the company’s existent distribution network along with the outstanding ongoing performance from the DWL® ultrasonic Doppler blood flow division, the company will further strengthen growth, going forward.

Key Valuation Metrics (Source: Thomson Reuters)

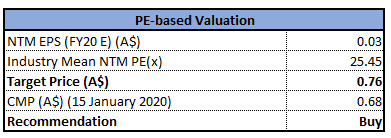

Valuation Methodology: Price to Earnings Multiple Approach

Price to Earnings Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

Stock Recommendation: The stock of the company generated positive returns of ~94.4% over a period of one year. In FY19, the company delivered a stellar result, driven by higher sales in China, Germany-based DWL and the USA. In FY19, the company planned to advance the first MEG sale to Barrow Neurological Institute (BNI), along with the second and final phase of the installation of the MEG system in the days ahead, which will eventually contribute to the long-term growth of the company. From the analysis standpoint, the company has recorded revenue CAGR of 5.5% over the last four years. Considering the above factors, we have valued the stock using a relative valuation method, i.e., Price to Earnings multiple, and for the purpose, we have taken the peer group Somnomed Ltd (ASX: SOM), Probiotec Ltd (ASX: PBP) and Universal Biosensors Inc (ASX: UBI). As a result, we have arrived at a target price depicting an upside of lower double-digit (in % terms). Hence, we recommend a “Buy” rating on the stock at the current market price of $0.680, down 2.857% on 15 January 2020.

.png)

CMP Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...