Kalkine has a fully transformed New Avatar.

.PNG)

After the fallout of coronavirus that has casted a pall on global economies, Australia sees a ray of hope in accelerated expansion and exploration in the mining industry, rising mineral demand and a healing Australian dollar. The country’s iron ore miners are set to benefit from Brazil’s ailing exports. Due to the rising coronavirus infections and suspension of operations at Vale SA, a mining giant in Brazil, the country will not be able to keep up with the iron ore demand across the world. In such a scenario, Australia is expected to become a rescuer on the face of the growing demand for iron ore. After iron ore, coal was the second-largest exported mineral in FY19 on the back of high-quality coal produced by Australian miners. Coal miners in Australia have undertaken development projects, which will benefit the country’s trade in the long-term. Some of the commodity prices are favouring the mining industry such as iron ore, coal, etc. The price of iron ore has increased to ~US$105 per tonne, up 1.2% on 15th June 2020. In addition to iron ore and coal, gold prices in Australia have also seen a rise, majorly due to the accelerated exploration activities and increased investor confidence during the crisis.

As per the information published on media platform, Australia is planning to spend around $1.5 billion on infrastructure and fast-track approval for projects to promote quick recovery. This came in addition to the expenditure of $3.8 billion on infrastructure, as announced by the government earlier. This additional spending is expected to include the expansion of copper production at BHP Group’s Olympic Dam. The decision raises the optimism around the acceleration of recovery as the mining industry has been at the forefront of protecting Australia during a period of crisis. Moreover, it supports the recent communication by the Minerals Council of Australia regarding reforms in the mining industry to boost economic growth.

The Minerals Council of Australia suggested that the Australian Government should consider certain reforms in the mining space, to accelerate its contribution to economic recovery. The MCA suggested a range of policy and regulatory options, including lower taxes, faster project approvals, modern skills and flexible workplaces, to the government, and believes that the sector can be a significant player in lifting the economy if the above factors are taken care of. Unlike other mining nations, Australian minerals companies have been essential service providers and have continued to operate with minimum disruptions during the coronavirus pandemic. The country has a potential mining investment pipeline of up to $100 billion, covering projects in coal, iron ore, base metal, critical mineral and gold.

The council stated that the growing economies of highly populated nations such as India and Southeast Asia will support higher demand for industrial metals such as steel, copper and aluminium as they recover and continue to grow with their expanding housing, infrastructure and manufacturing needs. Thus, the country will see increased resources demand from developing economies. Recently, Australia and India have signed a preliminary pact for the supply of minerals to the latter, to enhance bilateral trade.

Rise in Iron Ore Prices: According to the latest export data published by the Australian Bureau of Statistics, Australian exports remained strong during April 2020, largely due to the ongoing demand for Australian resource commodities, particularly Iron ore, from major trading partners across Asia. Due to increased demand from China and major supply disruptions in Brazil, a rival to Australia’s iron ore exports, iron ore prices in Australia have seen a significant rise. Iron ore constitutes a major portion of Australia’s exports and a rise in prices eventually increases the demand for the Australian dollar. As a result, the Australian dollar recently saw a big jump in value against the US dollar.

Competitive Advantage in Coal Exports: In addition to iron ore, coal has formed a large portion of dry bulk trade by Australia and has seen demand from different geographies, including China, Japan, India, South Korea, Taiwan, etc. In 2020, China and Japan imported a large amount of Australian coal. Amid the recent tensions emerging due to trade disputes between Australia and China, it is uncertain whether the country is willing to remain a key importer of Australian coal. However, we cannot deny the fact that Australia’s capability to produce high-quality coal at low costs has helped it gain a competitive advantage over others. Henceforth, while Australia works to mend its relationship with China, there is a potential to shine in other key markets like Japan in the long term.

Gold Miners Progressing on Exploration Programs: Australian gold prices have also seen a recovery lately, as companies began to progress on their exploration programs. Several gold players have begun drilling activities to expand their resources and increase the business potential. During the pandemic, gold miners have continued their operations without major disruptions and have ensured health & safety at the sites.

In light of the above factors, we can say that miners in Australia can play a significant role in economic recovery. Moreover, if the government continues to provide its support for approval of projects, the gain of Australian mining companies will eventually convert into an economic driver. Let us have a look at 4 stocks that seem to be in good shape and are aligned with developments happening in the broader industry.

1. Iluka Resources Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 3.7 Billion, Annual Dividend Yield: 1.48%)

FY19 EBITDA Up 3% on PCP: Iluka Resources Limited (ASX: ILU) is an international mineral sands company with projects in Australia, Sierra Leone and Sri Lanka. The company holds over 60 years of experience in the mineral sands industry and it currently enjoys a globally integrated marketing and distribution network. For the financial year 2019, the company reported an underlying group EBITDA of $616 million, up 3% on the previous year. Further, the company reported an underlying net profit after tax of $279 million. For the full year, the company declared total dividends of 13 cents per share, representing 40% of free cash flow. As on 31 December 2019, the company had a net cash position of $43 million and free cash flow of $140 million. For the first quarter of 2020, the company reported Zircon/Rutile/Synthetic Rutile (Z/R/SR) production of 153 thousand tonnes, down 16% from December’19 quarter.

Outlook: The company is currently focussed on the demerger of its royalty business. The company is targeting the demerger documentation to be finalised and distributed to shareholders as soon as practicable following the completion of the Half Year Accounts. Due to the uncertainty in relation to the impacts and duration of the pandemic, the company has withdrawn its FY20 guidance. Till now, the company has maintained operational continuity across its sites and supply chains.

The company earns its revenue by selling its mineral sands to customers based in the Americas, Europe, China, the rest of Asia, and other countries under a range of commercial terms. In FY19, the company’s total revenue from operations stood at $1,193.1 million, all of which came from the sale of goods to different countries. China is currently the biggest customer of the company. During the year, the company sold $404.1 million worth of mineral sands products to China. In the rest of Asia, the company’s sales stood at $200.9 million. In Europe, the company sold products worth $400.1 million in 2019. While the recent trade tensions with China can be a potential risk for the business, exposure to different markets indicates that the developments with respect to the export of minerals and growth in the company’s sales may go hand in hand. .png)

Valuation Methodology : EV/EBITDA Multiple Based Relative Valuation (Illustrative)

.png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs ILU (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: In the last six months, the stock has corrected by 6.01% on ASX, but has increased by 22.69% over the past three months. Despite a rapid fallout in the market due to COVID-19, the stock price has shown remarkable recovery, especially in the month of May, reflecting a resilient business position, underpinned by strong financial, operational and market fundamentals. Although the company has withdrawn its guidance for FY20 due to COVID-19 pandemic, it must be noted that in the past the company has demonstrated flexibility to adjust its operational settings in line with market conditions as required. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $8.55, down 2.397% on 15th June 2020.

2. Whitehaven Coal Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.69 Billion, Annual Dividend Yield: 8.79%)

FY20 Guidance Maintained: Whitehaven Coal Limited (ASX: WHC) is a leading Australian producer of premium-quality coal products which are used to fuel high efficiency, low emission electricity generation; to make steel and in other smelting applications. For the first half of FY20, the company reported EBITDA of $177.3 million, down from $550.8 million reported in H1FY19, reflecting a decrease in global COAL Newcastle Index prices and ROM production. For the half year period, the company reported net profit after tax of $27.4 million and cash generated from operations stood at $122.3 million. For the March quarter, the company reported managed ROM coal production of 4.9Mt, up 8% on the pcp. Further, the company reported saleable coal production of 4.1Mt and total coal sales of 4.5Mt.

Outlook: The growing economies of Asia and their evolving environmental regulations are providing the opportunity for Whitehaven to diversify and increase margins for securing sustainable returns for all Whitehaven stakeholders. Amid Covid-19 pandemic, the company is working largely as normal with no material impact on production. Further, the company has maintained its FY20 guidance, as per which, it expects Managed ROM Coal Production in FY20 to be in the range of 20.0Mt – 22.0Mt and Unit cost (excluding royalties) to be in between 73 – 75$/t. The company has been progressing on three key development projects, including Narrabri Underground Mine Stage 3 Extension Project, Vickery Extension Project and Winchester South Metallurgical Coal Project, which are expected to expand managed ROM production in the next 10 years.

During the last financial year, the company exported over 21.6 million tonnes of high-quality thermal and metallurgical coal. Japan, the company’s key export market, achieved the highest average efficiency rate of 42% and least pollutants for coal-fired generation in the world. In FY19, the company sold $1,255 million worth of products to Japan. The company also exports its products to Taiwan, Korea, India, China, Malaysia and many more countries, providing a diverse presence for its operations. However, the company also highlighted the risk factors, stating that India has recently closed several ports which are expected to impact shipments of Australian metallurgical coal in the June quarter. Other key metallurgical markets in North East Asia have recently announced steel production cuts, which is expected to reduce coal demand in the June quarter..png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative).png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs WHC (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained positive returns of 5.1% in the last three months and is currently trading near its 52-week low level of $1.375. After the COVID-19 led shockwaves disturbed the market, the company’s stock witnessed a massive fall. However, in recent weeks, it has been on stable grounds with the market volatility index. With uninterrupted operations across its sites, the company is currently progressing to achieve its FY20 guidance. However, it is to be noted that the company’s future financial performance is subjected to future coal prices. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $1.575, down 4.545% on 15th June 2020.

3. Resolute Mining Limited (Recommendation: Buy, Potential Upside: Low Double-Digit)

(M-cap: A$ 1.14 Billion, Annual Dividend Yield: NA)

Updated 2020 Production Guidance: Resolute Mining Limited (ASX: RSG) is a gold production company engaged in the exploration, development and operation of gold mines in Africa and Australia. The company recently completed the Equity Raising of ~$195 million which comprised a two-tranche placement and share purchase plan. During the quarter ended 31st March 2020, the company delivered a solid production result and completed Ravenswood sale, with total proceeds realisable of up to $300 million. Gold sales for the quarter stood at 102,008 ounces at an average realised gold price of US$1,407 per ounce.

Outlook: After the completion of sale of Ravenswood, the company updated the 2020 production guidance to 430,000 ounces at an AISC of US$980/oz. The cost guidance takes into account the production costs incurred at Ravenswood and any potential increase in corporate costs due to COVID-19. The company possesses sufficient financial flexibility to capitalise on future growth opportunities and deliver on its strategy of being a multi-mine, African focused gold producer.

In 2019, the company generated all its sales in West Africa, with 75% of the sales revenue coming from Mali and the remaining 25% from Senegal. The company has continued to operate with minimum disruption and is accelerating is exploration programs at these sites. In the March quarter report, the company reported significant high-grade oxide gold intersections from the ongoing exploration drilling programs at Syama satellite deposits, providing encouragement for the potential to extend the life of Syama’s oxide operation. Moreover, the company’s exploration programs at Mali are progressing without any disruption from COVID-19 related factors. Despite the above developments, the COVID-19 pandemic has posed unique risks and challenges to global mining companies operating in Africa and the company has maintained operational flexibility through significant ore stockpiles at all its operating mines, high local employment and sufficient staffing arrangements for unhindered operations..png)

Valuation Methodology: EV/EBITDA Multiple Based Relative Valuation (Illustrative).png)

EV/EBITDA Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

.png)

A-VIX vs RSG (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained positive returns of 8.95% in the last one month and is currently trading below the average of its 52-week trading range of $0.605 - $2.12. During the March quarter, the company simplified its capital structure, reduced its borrowing costs and improved financial flexibility through capital raising. The strength of the company’s business and its capability to defend itself against the broader market, is demonstrated by the latest trend in the stock price relative to the market volatility index, as depicted in the chart above. At current trading levels, the stock seems attractive taking into consideration the company’s performance and outlook. We have valued the stock using the EV/EBITDA multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside (in percentage terms). Hence, we give a “Buy” recommendation on the stock at the current market price of $0.995, down 3.865% on 15th June 2020.

(4) BHP Group Limited (Recommendation: Hold, Potential Upside: Low Double-Digit)

(M-cap: A$ 106.02 Billion, Annual Dividend Yield: 5.92%)

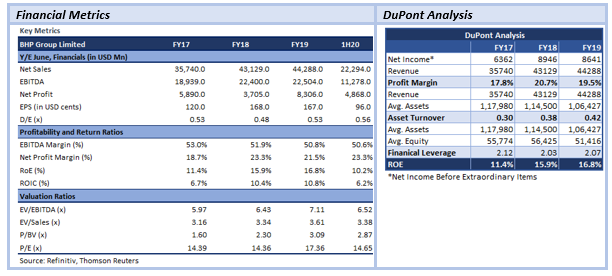

Strengthened Demand in China: BHP Group Limited (ASX: BHP) is among the world’s top producers of major commodities, including iron ore, metallurgical coal and copper. During the nine months ended 31st March 2020, the company achieved record production at Western Australia Iron Ore (WAIO) and Caval Ridge. Iron ore production for the period increased by 3% on pcp to 181Mt. Copper production also increased by 5% to 1,310kt.

Outlook: The company witnessed strengthened demand in China, but has a weak outlook for other major economies, including the US, Europe and India. Until the time the COVID-19 situation pacifies and demand begins to recover in these areas, the business seems resilient to generate decent cash flow and continue to operate with a strong financial position. At the end of March 2020, the company had six major projects under development in petroleum, copper, iron ore and potash, with a combined budget of US$11.4 billion over the life of the projects. The projects in petroleum and iron ore are tracking as per plan and are subject to potential impacts from COVID-19. For FY20, the company expects petroleum production to be around the lower end of the range of 110 MMboe – 116 MMboe. Iron ore production is expected between 242Mt – 253Mt.

As per the annual report for 2019, China is the consumer of around half of the company’s commodities. Other customers included the United States, Japan, Europe and India. Out of the total revenue of US$44,288 million in FY19, the company generated US$24,274 million from China, followed by US$4,193 million from Japan. Thus, we can say that the company has a role in shaping the recent export numbers for iron ore. The company’s sales and purchases, however, remain subject to exchange rate transaction risk on foreign currency.

Valuation Methodology:P/CF Multiple Based Relative Valuation (Illustrative)

.png)

P/CF Multiple Based Relative Valuation (Source: Refinitiv, Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, NTM-Next Twelve Months

A-VIX vs BHP (Source: Refinitiv, Thomson Reuters)

Stock Recommendation: The stock of the company gained positive returns of 17.15% in the last one month and is currently trading above the average of its 52-week trading range of $24.050 - $42.330 The company has a strong financial position, underpinned by its low-cost operations and a resilient business to generate solid cash flow. After a slump in the stock price due to COVID-19 outbreak, the stock has demonstrated the strength of the business through a quick recovery. We have valued the stock using the P/CF multiple based illustrative relative valuation method and arrived at a target price with a low double-digit upside in percentage terms. Hence, we give a “Hold” recommendation on the stock at the current market price of $35.25, down 2.056% on 15th June 2020.

.PNG)

Comparative Price Chart (Source: Refinitiv, Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...