Company Overview: Collins Foods Limited is engaged in the operation, management and administration of restaurants. The Company operates in three segments: KFC Restaurants, Sizzler Restaurants and Shared Services. The Company's restaurants comprise approximately three restaurant brands, including KFC Restaurants, Sizzler Restaurants and Snag Stand joint venture outlets. The Company operates approximately 180 KFC restaurants in Queensland, northern New South Wales, Western Australia and Northern Territory. It owns and operates over 20 Sizzler restaurants in Australia. Snag Stand operates approximately five corporate-owned outlets and a franchised outlet. The KFC brand is owned by Yum!. The Company operates in Australia and Asia.

.png)

CKF Details

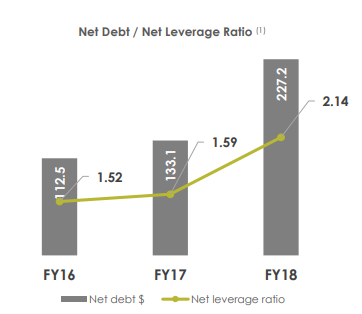

Expansion of Footprint to Support Long-term Growth: Collins Foods Limited (ASX: CKF) happens to be an Australian listed public company which is engaged in the operation of food service retail outlets. CKF is a small-cap company with the market capitalization of around $770.14 Mn as on 25 February 2019. During FY18, the company had wrapped up the acquisitions of KFC in Australia and Europe which resulted in the expansion of footprint in the high potential growth markets. The continuation of organic growth is due to the focus on driving operational efficiencies. Resultantly, the company posted revenues amounting to $770.9 million in FY18, implying the rise of 21.7% on a Y-o-Y basis. Underlying EBITDA stood at $94.5 Mn in FY18, showing a decent growth of 16.4% over the prior year. This was mainly supported by the cost control methodologies and the focus towards continued operational efficiency improvements. Amidst all this, the company had managed to deploy efforts towards growth. We expect that the company’s increased footprints and the focus towards managing the costs efficiently would support its key margins and that its strategy might act as the long-term growth catalyst. Moreover, the company continues to maintain its focus towards maintaining a robust balance sheet. There has been a rise in the level of gearing in FY 2018 because they have made the acquisitions to support overall growth in the long run. The company’s net debt encountered $94.1 million rise in FY 2018 on the YoY basis due to the acquisition of 16 KHC Netherlands restaurants as well as 28 KFC restaurants in Australia. At the end of FY 2018, the company’s net leverage ratio was 2.14x. However, there are expectations that its net leverage ratio would be below 2x moving forward. We expect that the company’s expanded footprint and the focus on continuing the track record of successfully integrating acquisitions along with driving the operational excellence throughout the business might act as a catalyst for the company and support to improve top-line growth in the upcoming periods.

.png)

Underlying EBITDA, Underlying NPAT, and Net Debt/Net Leverage ratio (Source: Company Reports)

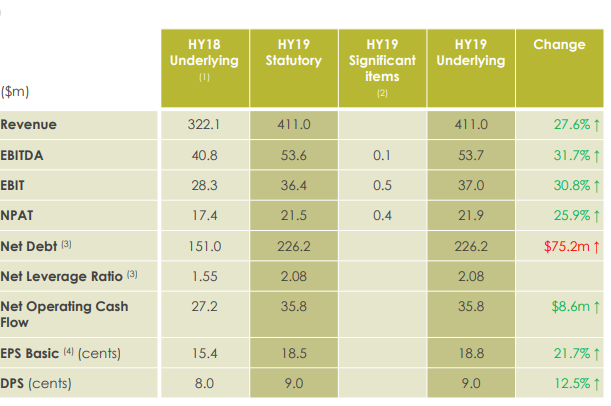

Robust 1H FY19 Performance: Collins Foods had noted that its results for KFC Australia business had demonstrated robust results. Its same store sales growth has demonstrated improvement throughout the states, especially in Western Australia, and they have wrapped up the acquisition of last 3 remaining stores from Yum! which has strengthened CKF’s position as largest KFC franchisee in Australia with 228 stores. The company has also managed to enter into Development Agreement to establish 50 Taco Bell restaurants in the time frame of the next three calendar years. The company’s revenues witnessed a rise of 27.6% and stood at $411.0 million while statutory EBITDA amounted to $53.6 million implying 42.9% rise YoY and the underlying EBITDA rose 31.7% YoY to $53.7 million. The company’s net margin, in 1HFY19, stood at 5.2% at the end of October 2018 which implies the rise of 1.2% reflecting its capability to turn its top line into the bottom line. Also, the company’s operating margin has demonstrated YoY improvement of 1.5% and stood at 8.9% at the end of October 2018. The company’s return on equity (or ROE) encountered the YoY rise of 2% and stood at 6.4% which reflects the company’s focus towards delivering returns to shareholders. We expect that the company would be able to sustain decent margins moving forward on the back of increasing footprints which could drive revenue growth. Also, the respectable levels of CKF’s ROE might look attractive to market players. In HY 2019, the company had also announced a fully franked interim dividend of 9.0 cents per ordinary share which reflects the rise of 12.5% as compared to 1H FY18.

1HFY19 Key Metrics (Source: Company Reports)

Rise in KFC Australia’s EBITDA Margins: The national footprint of Collins Foods of 228 KFC restaurants had posted robust results in HY 2019 and its EBITDA rose 23.5% YoY and stood at $56.1 million. The EBITDA margins rose to 17%, while in HY 2018, it was 16.8% with the rise aided by the focus towards operational efficiencies as well as margin management throughout the network. The same store sales growth for the stores which are in Western Australia happens to be in positive territory which has been further solidifying the improvement in the margins. Further, the key personnel of KFC Australia had stated that focus towards maintaining the earnings margin while working towards driving the incremental sales via operational improvements, digital and delivery initiatives as well as the consistency of customer experience, have significantly aided KFC Australia operations. The deployments towards KFC digital have been helping in witnessing growth in App sales as well as e-commerce and digital marketing initiatives expansion. The focus on expanding the delivery footprint might act as the catalyst for long-term growth potential.

KFC Australia (Source: Company Reports)

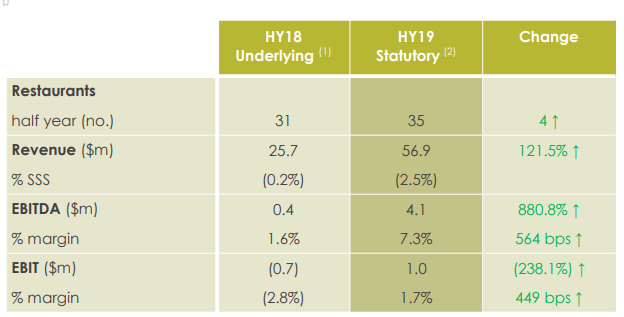

How KFC Europe Performed in HY 2019: Despite being in the early stages, KFC Europe operation’s, which covers 17 restaurants in Germany as well as 18 restaurants in the Netherlands, the revenues witnessed the rise of 121.5% and stood at $56.9 million which demonstrates full half-year earnings from the Netherlands. KFC happens to be underpenetrated in the Netherlands and Germany which provides an opportunity to support the long-term growth for the company’s KFC Europe business. In HY 2019, the company managed to build and opened two restaurants in Germany. There are expectations that further four restaurants would be opened throughout the Netherlands and Germany in 2H FY19.

In 1H FY19, the focus was towards increasing the presence in the market as well as brand awareness and driving the transaction growth with the help of value promotions. The sales did witness some negative impacts, from June to August, because of unusually hot weather which substantially weighed over the customer traffic. We expect that the focus towards driving transaction growth via value as well as innovation would support KFC Europe and might also support in driving the revenues. Market penetration and a rise in frequency visits might act as a tailwind for long-term growth.

1HFY19 KFC Europe Financial Metric (Source: Company Reports)

Plans to open 10 Taco Bell Restaurants: Collins Foods managed to open second Taco Bell restaurant in Robina (Queensland) on November 3, 2018. The top management is positive about the future prospects about Taco Bell and as it prepares for the robust expansion. In HY 2019, the company had entered the Development Agreement with the Taco Bell to build 50 restaurants in the time frame of next three calendar years which would be covering three states (i.e. Queensland, Victoria as well as Western Australia) and the financing would be done from internally generated cash flows. In the calendar year 2019, there are plans to open up 10 Taco Bell restaurants.

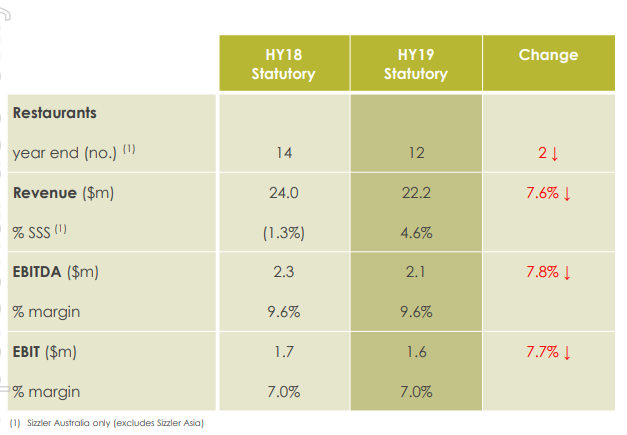

Growth Witnessed in Sizzler Asia: The Sizzler revenue witnessed a decline of 7.6% on the YoY basis in HY 2019 to $22.2 million due to two fewer restaurants as compared to a prior half year. However, the earnings in Sizzler Asia offset the decline in Sizzler Australia sales. The royalty revenue from Sizzler Asia had witnessed a rise of 19% as compared to the prior half year. At the end of HY 2019, 73 Sizzler Asia restaurants were operating.

1H FY19 Financial Metrics of Sizzler Asia (Source: Company Reports)

Drivers for Future: Collins Foods has been maintaining its focus towards the growth strategy of KFC Australia business and it plans to drive sales by the improvement in the speed of service as well as delivering a consistent customer experience. There are expectations that the company would be building and opening a total of 8 KFC restaurants in Australia by the end of the financial year. Moreover, the company also plans to expand the size of the home delivery footprint over time with the help of multiple aggregators. With respect to Europe, the company stated that focus would be towards improving the margins as well as optimizing back-office support centre to deliver the cost synergies and efficiencies.

Overall, there are expectations that Collins Foods witness decent growth moving forward which would be backed by robust operational results which were witnessed in KFC Australia operations, the opportunities which might arise for KFC Europe as well as new growth pillar which is being represented by Taco Bell. Also, the company happens to be in a strong position to capture the growth opportunities because of the robust balance sheet as well as increasing operating cash flows.

Stock Recommendation: On the daily chart of Collins Foods Limited, Moving Average Convergence Divergence or MACD has been applied and default values were used for the purposes. After careful observation, it was noticed that the MACD line has crossed the signal line and had moved in the upward direction after crossover which demonstrates the bullishness. As a result, there are expectations that the company’s stock price would witness a rise moving forward.

Moreover, the company is expected to be aided by the focus towards increasing the footprints and towards the cost optimization strategy. Also, the company might be supported by its strengthened position with respect to KFC franchisee in Australia. Moreover, the company is also targeting to reduce its net leverage ratio to a level which would be below 2x. The company’s management is of the view that its robust operating cash flow would reduce the gearing level over time. Given the backdrop of aforesaid facts and decent fundamentals, we have a “Buy” recommendation on the stock at the current market price of A$6.710 per share (up 1.513% on 25 February 2019).

.png)

CKF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...