Kalkine has a fully transformed New Avatar.

Company Overview: Collection House Limited is a receivables management company. The principal activities of the Company include the provision of debt collection services and receivables management throughout Australasia, and the purchase of debt. The Company's segments include Collection Services, Purchased Debt Ledgers and All other segments. The Collection Services segment includes the earning of commissions on the collection of debts for clients. The Purchased Debt Ledgers segment includes the collection of debts from client ledgers acquired by the Company and its subsidiaries. The Company's services include debt purchasing, collection services, hardship services, legal and insolvency services, and credit management training. Its subsidiaries include CLH Legal Group Pty Ltd, which offers debt recovery, and litigation and insolvency solutions and services; Collective Learning and Development Pty Ltd, a training provider, and Midstate CreditCollect Pty Ltd, a boutique collection agency.

.png)

CLH Details

Consistent Results and Decent Increase in EBIT: Collection House Limited (ASX: CLH) is Australia’s leading end-to-end receivables management company which provides debt collection services and is also engaged in the purchase of consumer debt. The company has two reportable segments: Purchased Debt Ledgers (PDL) and Collection Services. As on 20 January 2020, the market capitalization of the company stood at ~$154.01 million. The top management in its recent Annual General Meeting stated that revenue of the company witnessed an increase of 12% on FY18 and stood at $161.1 million. This was mainly due to the second transaction with Balbec Capital LP (“Balbec”), PDL growth and a positive revenue recognition change under AASB 9. In the same time period, earnings before interest & tax (EBIT) was lifted by performance and the lower amortisation charge incurred under AASB 9 and went up by 18% from $43.4 million to $51.3 million. The decent financial performance enabled the company to achieve its profit target with an 8% increase in Net Profit After Tax to $22 million. Collection House Limited delivered a solid result in the 2019 financial year with each segment of its business playing its part. The company exceeded its 19.2 – 19.5 cents earnings per share guidance and delivered an EPS of 20.5 cents per share. This was achieved through the tailwind of improved profit recognition under the new accounting standards and a stronger second half, which contributed almost 60% of the full year result. During the past year, the company also made strategic acquisitions of New Zealand-based Receivables Management (NZ) Ltd (RML), and the PDL book and selected assets of ACM Group in Sydney. The company paid a final dividend of 4.1 cents per share, taking the full year fully franked dividends to 8.2 cents per share in FY19, representing an improvement of 5% from 7.8 cents per share in FY18. Over a period of 4 years from FY15 to FY19, the company witnessed a CAGR of 6.34% in revenue and a CAGR of 5.39% in gross profit.

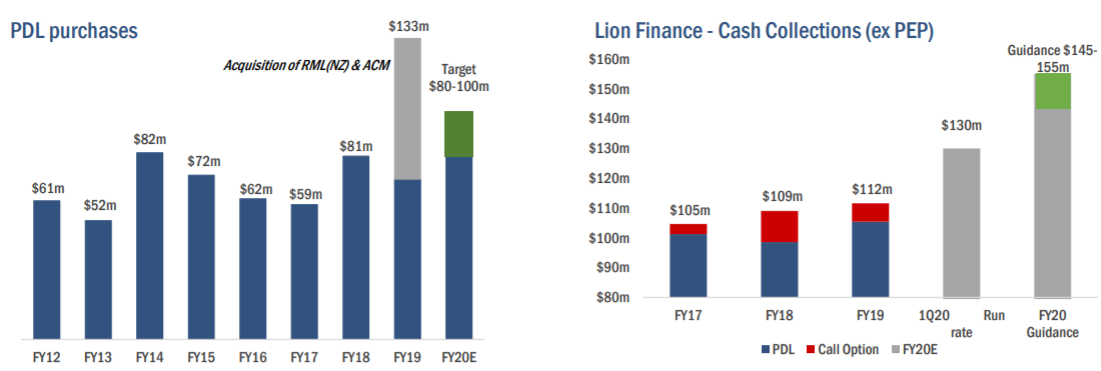

Given these positive developments, the company achieved a record level of PDL purchasing of $133 million in FY19, up by 63% on the previous year. The company expects a positive outlook for the coming year owing to growth in market share in Australia and New Zealand through the acquisition of debt portfolios. On the PDL supply side, things look very healthy for the year ahead, especially in the context of estimated market growth, conservative implementation of AASB 9, and developments in the sector potentially heading to a reduced pool of trusted buyers for PDLs. .png)

FY19 Financial Performance (Source: Company Reports)

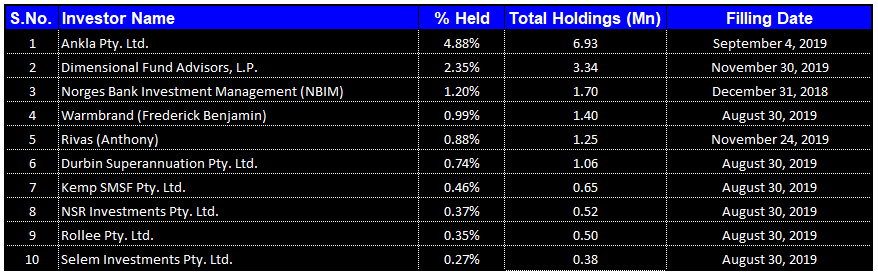

Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Collection House Limited. Ankla Pty. Ltd. is the largest shareholder with a percentage holding of 4.88%.

Top 10 Shareholders (Source: Thomson Reuters)

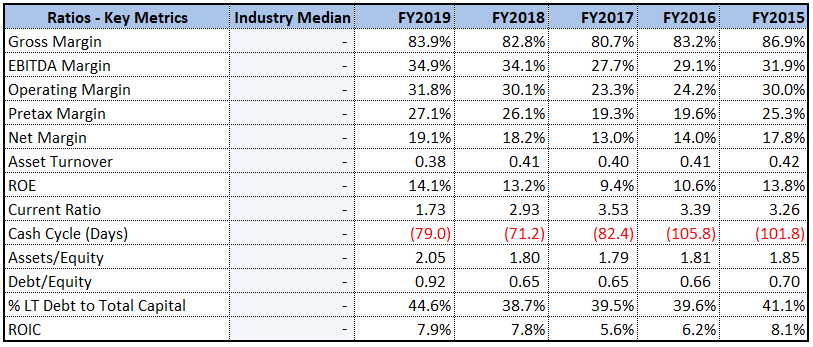

Increasing Returns to Shareholders: Over the span of 2 years, gross margin of the company increased to 83.9% in FY19 from 80.7% in FY17. This indicates a healthy financial condition of the company and implies that the company can make reasonable profits on sales as long as it keeps its overhead costs in control. In the same time span, EBITDA margin of the company witnessed an improvement and stood at 34.9% in FY19, up from 27.7% in FY17. This implies that the company now has smaller operating expenses in relation to its revenue which will help boost its profits. The company has also seen an increase in its net margin, from 13% in FY17 to 19.1% in FY19. During FY19, Return on Equity stood at 14.1%, up from 9.4% in FY17. This indicates that the company is well deploying the capital of its shareholders and is capable of generating profits internally.

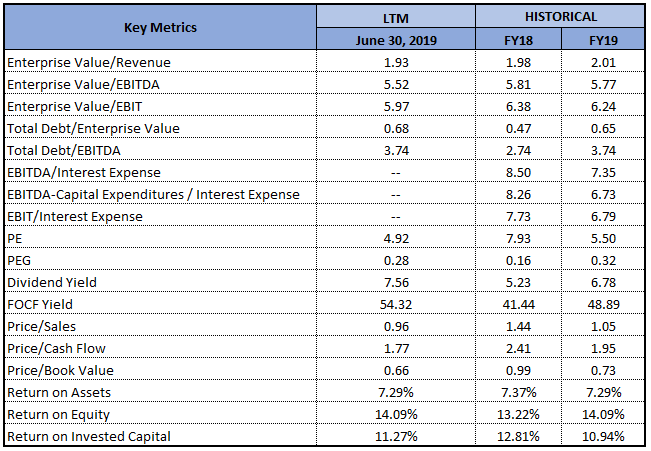

Key Metrics (Source: Thomson Reuters)

Portfolio Enhancement Programme - 3rd Balbec Transaction: The company has completed the third transaction under its partnership with Balbec Capital LP and its local related entity, InSolve Capital Australia Pty Ltd. Under this transaction, CLH will receive $10 million up front unencumbered cash in exchange for the assignment of five years’ cash flows from a segment of the Company’s Arrangement book with a face value of $24.8 million. Collection House Limited will continue to manage the portfolio on behalf of Balbec and will receive a monthly servicing fee through its Collection Services division. This transaction is expected to result in an accounting profit of $4.1 million after tax. In another release, the company stated that Doug McAlpine will take on the role of CEO, as Anthony Rivas, Managing Director and Chief Executive Officer has tendered his resignation, with effect from 24 November 2019.

Record Year for PDL Purchases: During FY19, the company witnessed an increase of 12% in Cash Collections from Purchase Debt Ledgers to $122 million along with $24 million from the Portfolio Enhancement Programme (PEP). The Purchase Debt Ledger segment reported an increase in revenue by 25% on FY18 to $93.7 million, whereas Collection Services revenue came in at $67.6 million, down by 2% on the prior year. This was mainly due to short term external factors which impacted client activity. Overall, trading conditions for both the Collection Services and PDL segments were tough. The company’s financial services sector clients, from whom the Group purchases or manages debt, had to deal with a rapidly changing regulatory environment and general disruption leading into the federal election.

PDL purchases and Cash Collections (Source: Company Reports)

Strong Growth in Balance Sheet: At the end of FY19, net gearing stood at ~48%, which will support PDL segment’s growth and acquisitions. The group had senior debt facilities of $225 million plus an overdraft of $12.5 million. The Company has developed a new capital management plan to support future growth and acquisitions. It is in the process of building a commercial relationship with Australian neo-bank Volt and has invested $8.5 million. Over a period of 4 years from FY15 to FY19, the company witnessed a CAGR of 10.49% in total assets. Due to the forecasted improvement in cash collections, the company expects to be able to fund FY20 PDL growth without further debt draw down. The company is gradually moving towards a less capital intensive and more innovative capital structure, with stable cash flows being moved off balance sheet and recycled into higher yielding portfolios.

What to Expect from CLH: The company expects an encouraging outlook owing to the increase in market share in Australia and New Zealand. The company has provided FY20 Cash Collections guidance for the PDL segment and expects it to be in between $145 million and $155 million, equating to 30% - 39% of growth in FY19. PDL purchases for the year are expected in the range of $80 million to $100 million. CLH’s partnership with Balbec is also expected to generate additional profits. The company also anticipates positive contribution from its alliance with Volt and remains confident for its improved performance in FY20. Collection House Limited is strategizing its growth by continued investment in its existing business and by creating complementary business model adjacencies. The company has provided its profit guidance for FY20 and expects Statutory EPS in the range of 23 cents per share to 24 cents per share. EPS guidance equates to growth of up to 14%, and growth of up to 8%, excluding PEP, on FY19 statutory results. The company has also acquired assets from ACM Group Limited for $40.3 million and is eyeing $75 million in expected future recoveries. This is expected to contribute $5.5 million EBIT in FY20. Furthermore, new client acquisitions will help the company to further diversify risk through growth outside of the banking sector.

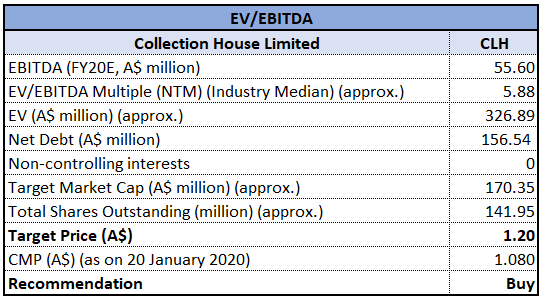

Valuation Methodology: EV/EBITDA Multiple Approach

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: As per ASX, the stock of CLH gave a return of 3.33% in the past one month and is trading close to its 52-weeks’ low level of $1.030. This offers a decent opportunity for the shareholders to enter the market and benefit from accumulation. The company has a well-defined structure for future growth and is enjoying strong business relationships with major Australian and international banks, financial institutions, large corporations, local Councils, public utilities, SMEs and Government agencies. Considering the customer centric approach of the business, improving margins, trading levels and positive outlook, we have valued the stock using EV/EBITDA based relative valuation approach and have arrived at a target price of lower double-digit growth (in percentage terms). For the said purposes, we have considered Money3 Corp Ltd (ASX: MNY), Pioneer Credit Ltd (ASX: PNC) and Consolidated Operations Group Ltd (ASX: COG) as peer group. Hence, we recommend a “Buy” rating on the stock at the current market price of $1.080, down by 0.461% on January 20, 2020.

CLH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...