Company Overview: Collection House Limited is a receivables management company. The principal activities of the Company include the provision of debt collection services and receivables management throughout Australasia, and the purchase of debt. The Company's segments include Collection Services, Purchased Debt Ledgers and All other segments. The Collection Services segment includes the earning of commissions on the collection of debts for clients. The Purchased Debt Ledgers segment includes the collection of debts from client ledgers acquired by the Company and its subsidiaries. The Company's services include debt purchasing, collection services, hardship services, legal and insolvency services, and credit management training. Its subsidiaries include CLH Legal Group Pty Ltd, which offers debt recovery, and litigation and insolvency solutions and services; Collective Learning and Development Pty Ltd, a training provider, and Midstate CreditCollect Pty Ltd, a boutique collection agency.

.png)

CLH Details

Revenue Rose 12%, and Consolidated NPAT Rose 8% in pcp: Collection House Limited (ASX: CLH) is primarily engaged in the provision of the debt collection services and purchase of the consumer debt. As on September 2, 2019, the market capitalisation of Collection House Limited stood at ~A$169.22 million. The company has two reportable segments, i.e., Purchase Debt Ledgers (PDLs), and Collection Services, which contributed around 58.1% and 41.9% revenue in total revenue respectively, in FY19. Recently, the company has released its financial results for the year ended June 30, 2019. As per the release, the company’s total revenue amounted to $161.1 million, which reflects a rise of 12% on the previous corresponding period and its consolidated net profit after tax (or NPAT) rose by 18% to $30.7 million. Resultantly, EPS stood at 22.3 cents per share in FY19, exhibiting a rise of 16% on a Y-o-Y basis. Based on the performance in FY19, the Board of Directors declared a fully franked second-half dividend of 4.1 cents per share, which will be paid on 25 October 2019 with record date of 3 October 2019. Moreover, the dividend reinvestment plan (DRP) is in place, providing the shareholders with a discount rate of 5%. The total dividend for FY19 stood at 8.2 cps (fully franked), which is 5.1% higher than the prior year total dividend payment of 7.8 cents per share.

There are expectations that the company is well-placed to deliver an improved FY20 result via substantially higher cash and accounting earnings from its enlarged portfolio of PDL assets. With respect to the capital management, the company’s total assets as at June 30, 2019, amounted to $471 million, which implies a rise of 27% on the prior year. The company’s net gearing at year-end stood at 48%. It has been generating robust operational cash flow, a significant portion of which is being reinvested into the asset base. The company is working within its facilities and gearing framework, and the expected step-up in Cash Collections in FY20 will provide adequate funding to remain active in the market for PDL books. The company stated that, during FY19, it has formalised the strategies for better supporting the employees and the customers, reducing its environmental impact and creating more meaningful engagement with the wider community initiatives.

There are expectations that the company’s decent liquidity levels, fundamentals and respectable operational capabilities might act as tailwinds for the overall growth of the company. The company has been generating robust operational cash flow, which might support its growth moving forward.

.png)

Balance Sheet and Capital Management (Source: Company Reports)

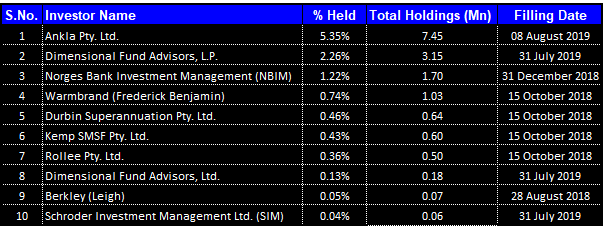

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Collection House Limited:

Top 10 Shareholders (Source: Thomson Reuters)

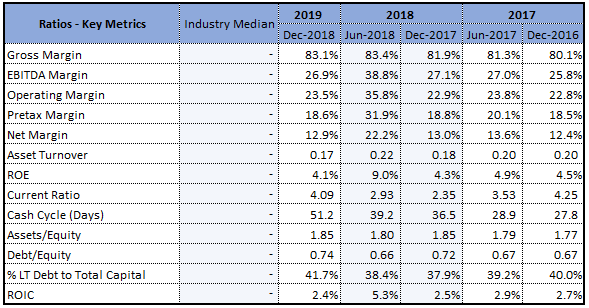

Overview of CLH’s Key Margins: The operating margin of Collection House Limited stood at 23.5% in 1H FY19, which implies a marginal rise of 0.6% on YoY basis and, thus, it looks like that the company’s operational capabilities have been improved. However, the company’s net margin stood at 12.9% in 1H FY19. Its current ratio stood at 4.09x in 1H FY19, which reflects a significant rise of 74.2% on YoY basis and, therefore, it looks like that the company would be able to meet its short-term debt obligations. Additionally, it can be said that the company’s liquidity capabilities have been improved, which provides it with sufficient headroom to make deployments towards strategic business activities. These deployments might prove beneficial for the overall company and could help it in achieving long-term growth objectives moving forward. Recently, the company has reaffirmed the strategy of becoming an industry leader in the development and implementation of technology solutions which has the potential to improve the customer, employee and client experience, and also support to generate operating efficiencies in years to come. The company continues to deploy each year towards the improvement to market-leading collection and customer management platform named C5. It was stated that, during FY19, 8% of the collections were generated from CLH’s online portal.

Key Metrics (Source: Thomson Reuters)

Key Personnel Changes: Collection House Limited has recently made an announcement that its CFO and Company Secretary named Kristine May has tendered her resignation, effective 30 June 2019. In the release, it was also mentioned that Ms May has been with CLH for 17 years in the range of roles, most recently as the company’s Chief Financial Officer and Company Secretary. The company also announced the appointment of Doug McAlpine as Chief Financial Officer (CFO) and interim Company Secretary from 1 July 2019.

Purchased Debt Ledger Segment’s Revenue Rose 25%: The company stated that the purchase debt ledger segment posted a revenue amounting to $93.7 million, which is up 25% as compared to FY18. This includes $9.8 million pre-tax profit from the Portfolio Enhancement Programme (PEP) transaction with Balbec. The transaction liberated capital from the mature payment arrangements, lessening the requirement for additional debt capital to finance investments in new PDL acquisitions to drive growth as well as improved financial returns.

Short Term External Factors Affected Collection Services Segment: The company stated that the Collection Services Segment has posted the revenues amounting to $67.6 million, which reflects a fall of 2% on the prior year. It was added that the shortfall was because of the short-term external factors, i.e., timing of the federal election and the Financial Services Royal Commission, which impacted the client activity.

The company added that, as this was anticipated to be the short-term trading downturn, collection resources were maintained during the year. The management of the company considers this a reasonable result during the period of significant market disruption for its clients. Since the year-end, there has been a return to the normal activity, with the first 2 months of FY20 already back to the FY18 levels of revenue and profitability.

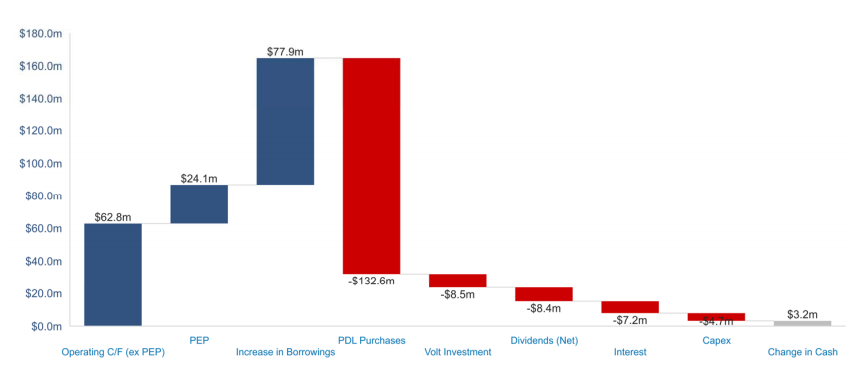

A Quick Look on Cashflow Management: In FY19, the company has invested $132.6 million in PDLs and $8.5 million in Volt Bank shares and distributed $8.4 million in the form of dividends (Net of DRP) to the shareholders. This was financed with net $77.9 million in new debt, due to an improvement in operating cash flow and portfolio enhancement programme (or PEP). There are expectations that the result of the portfolio investments would be producing a step-change in the cash flow in FY20.

Managing the Cashflow (Source: Company Reports)

Higher Dividend Yield of CLH as Compared to Industry: The Board of the company declared a fully franked dividend amounting to 4.1 cents per share. The record date for the dividend would be October 3, 2019, and the payment date would be October 25, 2019. In conjunction with 1H FY19 dividend of 4.1 cents per share, the total dividends for the financial year stood at 8.2 cents per share. Also, it was mentioned that the DRP would be active at the discount rate of 5%. At CMP of $1.215, the company has a decent annual dividend yield of 6.58%, which is higher than the industry median of 3.7% and, thus, it can be said that the dividend-seeking investors might be interested in the stock.

Dividends (Source: Company Reports)

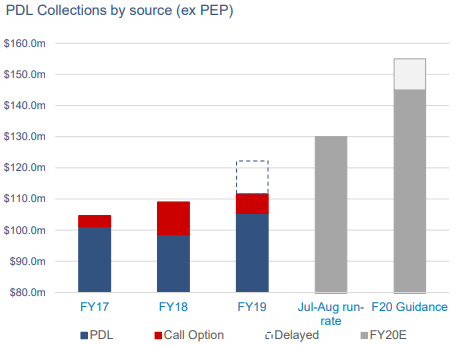

What to Expect from CLH Moving Forward: The Company’s growth strategy focuses on the following key elements such as (1) continuing to invest in its existing business, (2) continuing to expand in the new business segments within collection services, and (3) creating and building a complementary business model adjacencies. The company has provided PDL Cash Collections guidance for FY20, and it was mentioned that a strong upturn since year-end had been witnessed and the collections are targeted in the range of $145-155 million (ex PEP). FY20 Cash Collection guidance equates to 30-39% growth on FY19.

PDL Segment – Positive Trends (Source: Company Reports)

With respect to PDL Purchasing outlook, the company stated that the market has been offering ample opportunity to deploy the capital in Australia and New Zealand and the supply and demand mechanics are favourable. The PDL Purchase guidance happens to be in the range of $80–100 million. The company’s cash receipts have witnessed a CAGR growth of 4.25% in the time frame of FY15- FY19 and, thus, it can be said that CLH has decent capabilities to build cash levels. Between the same time frame, the company’s cash from operating activities have witnessed a CAGR growth of 2.82% and, therefore, it looks like that CLH is having respectable operational capabilities. There are expectations that its operational capabilities, as well as capabilities to build cash levels, might help the overall company moving forward.

Valuation Methodologies:

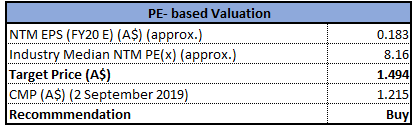

Method 1: PE- Based Valuation

PE- Based Valuation (Source: Thomson Reuters), NTM: Next Twelve Months

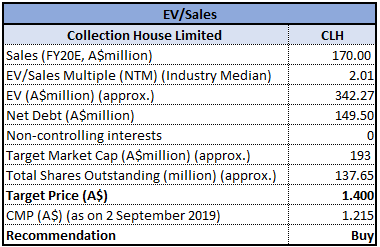

Method 2: EV/Sales Valuation Multiple

EV/Sales Valuation Multiple (Source: Thomson Reuters), NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: The stock of Collection House Limited has witnessed a fall of 2.41% in the span of previous three months, while in the time span of past six months, the stock has fallen 9.33%. Currently, the stock is trading slightly below the average of 52 weeks high and low levels of $1.640 and $1.070, respectively, proffering a decent opportunity for accumulation. Moreover, the company has been generating robust operational cash flow, and the significant portion is being reinvested into the asset base. The company is possessing decent capabilities to generate revenues, which is evident from its CAGR growth of 6.34% in its top-line between the time span of FY15- FY19. Based on the foregoing, we have valued the stock using two relative valuation methods, Price to Earnings multiple and EV/Sales multiple and have arrived at the target price upside of lower double-digit growth (in percentage term). Hence, considering the aforesaid facts and current trading levels, we give a “Buy” recommendation on the stock at the current market price of A$1.215 per share.

.png)

CLH Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...