Company Overview - Coca-Cola Amatil Limited (CCA) with its subsidiaries is engaged in the manufacture, distribution and marketing of carbonated soft drinks, still and mineral waters, fruit juices, coffee and other alcohol-free beverages. CCA operates in four business segments: The Australia, New Zealand and Fiji, and Indonesia and PNG segments. CCA is also engaged in the processing and marketing of fruits, vegetables and other food products, and the manufacture and distribution of alcohol ready-to-drink products, and the distribution of premium spirits and beer brands. The Company’s principal operations are in Australia, New Zealand, Fiji, Indonesia and Papua New Guinea (PNG).

Analysis – Coca – Cola amatil appears to be at the cross roads currently. Between 2001 and 2010 it generated an Earning Per Share (EPS) Compound annual Growth Rate of 11.2% as it innovated, took market share and lifted prices. Since 2012, EPS has declined 25% as consumers have consumed less carbonated soft drinks (CSD), the supermarkets have exerted pressure and its Indonesian business has suffered from macroeconomic headwinds. Earlier in 2014, CEO Terry Davis stood down from the position he held since 2001. Alison Watkins former CEO of Graincorp, has taken over the CEO role and will provide a critical strategic review in August.

CCL Brands (Source - Company Reports)

CCL Brands (Source - Company Reports)

While Amatil is still a high quality business, it faces a number of challenges we believe will be addressed but this will take time. The past 18 months have been characterized by a lack of product innovation and lower category growth, causing volume declines that have led to fixed – cost deleverage. The new managing director announced a strategic review in April 2014 to address the issues facing the company. In our view production and distribution can be rationalized to reconfigure the network and achieve material cost savings, some of which is likely to be reinvested in product development and marketing.

CCL EPS + DPS (Source - Company Reports)

CCL EPS + DPS (Source - Company Reports)

The coke brand is powerful in Australia, enabling amatil to generate excess returns over the long term despite a difficult competitive environment and unfavorable forces such as powerful customers like (Woolworths, Coles and global convenience chains), input costs that are outside its control and a shift towards healthier beverages in which Amatil has fewer competitive advantages. In our view, a number of Amatil’s issues are structural, such as a more health conscious society compounded by a frugal customer and rejuvenated competitor in Pepsi. With volumes in core categories declining it remains to be seen whether growth in other categories where Amatil has less brand equity such as water can offset this.

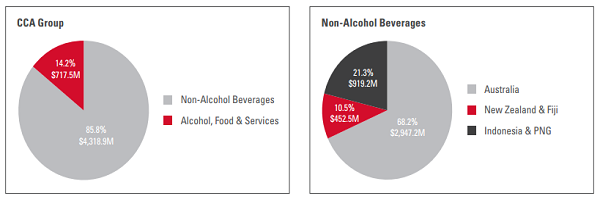

CCL Segments (Source - Company Reports)

CCL Segments (Source - Company Reports)

Declining volumes are also reversing Amatil’s network advantage, as its fixed cost distribution network is suffering from operating deleverage. A further pitfall of declining volumes is the pressure it puts on Amatil’s relationship with The Coca Cola Company or TCCC, which earns revenue by charging bottlers for concentrate. TCCC can either directly recover lost volume through increasing concentrate prices or indirectly by pulling back advertising spend (TCCC and bottlers jointly market products). We believe the latter is occurring. We also examined Amatil’s Indonesian segment, which has been volatile recently. We believe that Indonesia is being impacted by one off events and will recover with its growth story intact. Volume growth is expected to be 10% in 2014 and has been more than 10% for several years.

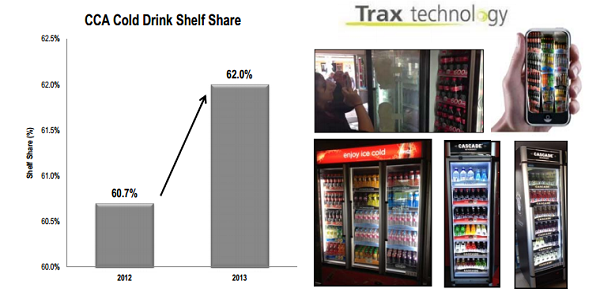

CCL Cold Drink Shelf Share (Source - Company Reports)

CCL Cold Drink Shelf Share (Source - Company Reports)

CCL is a highly efficient and profitable bottler following years of capital investment, in our view. Whereas many manufacturers have opted to underinvest in their operations and have preferred to run the business for cash, CCL on the other hand spent, which led to a number of improvements including: 1) a 15% reduction in average bottle weights 2) Shifting 80% of the ANZ business to self-manufactured PET. 3) Automating warehousing, reducing truck loading times from 25 to 7 mins. 4) Reducing peak season out of stocks from 12% to 2%. In 2013 CCL cut back on capex, presumably as it no longer delivered an acceptable return – an indication in our view that the business was already efficient.

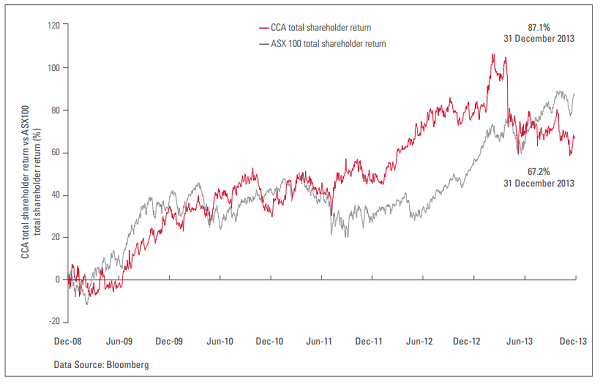

CCL Total Shareholder Return (Source - Company Reports)

CCL Total Shareholder Return (Source - Company Reports)

We believe CCL’s capex initiatives such as Project Zero drove the 500 basis points reduction in the cost to sales ration since 2004. On nearly any metric CCL is an efficient bottler. CCL’s core Australian business generates in US terms US$700,000 in sales for every employee which is in line or higher than its developed market peers. Profitability both on a margin and per employee basis is also high for CCL compared with other Coke bottlers.

CCL Daily Chart (Source - Thomson Reuters)

CCL Daily Chart (Source - Thomson Reuters)

A core problem for CCL has been reduced demand for its flagship Coke branded products. One way to deal with this problem is to acquire in faster growing categories. While earnings have been pressured in recent years CCL’s balance sheet looks solid which could enable it to acquire. Generally acquiring brands would be highly synergistic as they would enable CCL to improve the utilization of its distribution network (trucks and point of sale fridges) and production facilities. The coca – cola Company would need to be consulted on any deal presumably to ensure that the brand purchased didn’t cannibalize an existing supplied product.

Large independent customers (above a single store) value the service provided by CCL and re prepared to pay a premium for it. This again demonstrates defensive ness to other suppliers and channels. This is a capability CCL can leverage. Independent Customers (Single store operators) purchasing from supermarkets by nature do not adequately value the service offering provided by CCL. These are price sensitive customers to be treated as such. Reflecting this change we see an opportunity for CCL to push more single store operators to the low cost tele sell or online service models. Meanwhile we believe stickiness of demand for the 600ml Buddy and a reformatted price architecture should assist in customer retention. We see opportunity for significant field force cost savings which can be redirected to fund price reductions. CCL is currently rolling out field force IT solutions to begin streamlining its route service offer.

New CEO Alison Watkins flagged a material review of fixed costs and productivity, which we believe should result in manufacturing footprint consolidation, field force restructuring and head office consolidation. We put a BUY recommendation on the stock at the current price of $9.38.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...