Kalkine has a fully transformed New Avatar.

Company Overview: CML Group Limited is an Australia-based company, which provides financial management and payroll services. The Company's finance and pay-roll solutions include cashflow finance, migration, contract management, on-hire services and recruitment. The Company's segments include finance and other services. Its finance segment refers to invoice finance or receivables finance which provides an advance payment of approximately 80% of a client's invoice to help their business overcome the cash pressure of delivering goods or services in advance of payment from the customer (30 to 60 days). Its finance facility also offers credit control and free trade credit insurance which protects businesses from the burdens of client insolvency control. The other services segment includes employment solutions, such as labor sourcing and project management. Its payroll and other services division includes labor sourcing through recruitment agency panel management, project management and a migration practice.

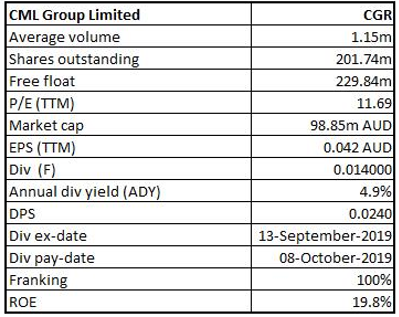

CGR Details

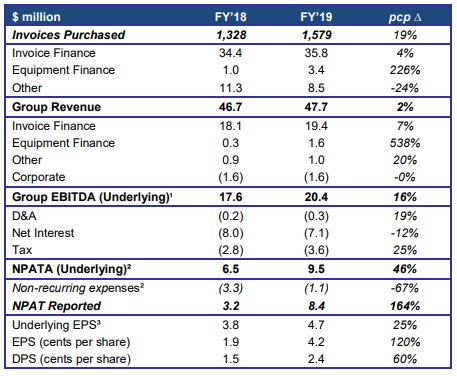

Remarkable Growth in Earnings during FY19: CML Group Limited (ASX: CGR) is in the business of financial management and payroll services. The services of the company include equipment finance, debtor finance and trade finance. The market capitalisation of the company stood at ~A$98.85 million as on 29th November 2019. Over the period covering 2015 to 2019, total revenue of the company has grown with a CAGR (compounded annual growth rate) of 19.61%. Group’s total revenue improved from $23.29 Mn in FY15 to $47.67 Mn in FY19. The bottom-line CAGR over the said period was reported at 371.47%, with FY15 and FY19 profit amounting to $0.017 million and $8.40 million, respectively. The highest growth in profit was reported in FY19, at 163.7% on Y-o-Y basis. During the year ended June 2019, the company witnessed a rise of 2% in revenue to $47.7 million in FY19 as compared to $46.7 million in FY18. Invoice Finance witnessed volumes funded increase by 19%, that, in addition to the operational efficiencies as well as a material reduction in the funding costs, resulted in a rise of 46% in NPATA.

During the year, the company has successfully diversified its product offerings, which include commencement of invoice discounting, targeting a larger customer base, and expanding CML’s addressable market. There are expectations that a rise in the product offering, coupled with an increase in addressable market might help the company in strengthening its revenues base. Moreover, Equipment Finance continues to generate growth, and the company is being able to secure new customer wins and increased customer retention. The company experienced a material reduction in funding costs, which is allowing the company to compete on similar terms with leading non-bank competitors. The company has continued to witness a robust performance in core factoring business, which supported the strong results of the financial year 2019 and facilitating the investment into business expansion initiatives. It can be said that these deployments might result in improving the performance of overall company moving forward and can also help in further strengthening the key financial numbers. The final dividend of the company stood at 1.4 cents per share (fully franked) and, therefore, the full-year dividend comes out to be 2.4 cents per share, reflecting a rise of 60% on the previous corresponding period.

CML Group Limited is confident of continued earnings growth via growth in loan book and improvements in the margin. Moreover, its diversified product offering, increase in the addressable market, decent capabilities to garner revenues and deployments towards business expansion initiatives are expected to act as tailwinds for long-term growth. The focus towards delivering returns to its shareholders (as evidenced by a rise in dividends and decent RoE position) might attract the market players’ attention.

FY19 Results Summary (Source: Company Reports)

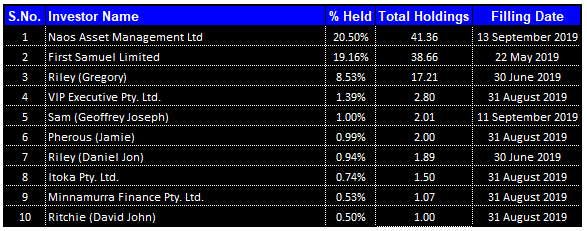

Top 10 Shareholders: The following picture provides an overview of the top 10 shareholders in CML Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

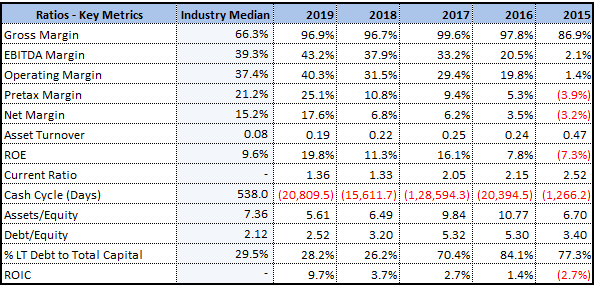

Decent Position in Key Metrics: Gross margin, EBITDA margin, and operating margin of the company stood at 96.9%, 43.2% and 40.3% in FY19 as compared to the industry median of 66.3%, 39.3% and 37.4%, respectively. Net margin of the company stood at 17.6% in FY19 against the industry median of 15.2%. This reflects that the company possesses better capabilities to convert its top-line into the bottom-line as compared to the broader industry.

Current ratio of the company stood at 1.36x in FY 2019, reflecting an improvement from FY 2018 figure of 1.33x. This implies that the company has improved its position to address its short-term obligations. Additionally, the decent standing from the liquidity standpoint provides headroom to the company to make deployments towards strategic business activities. Return on equity of the company stood at 19.8% in FY19 in comparison to the industry median of 9.6%, indicating the better returns provided to shareholders. There are expectations that decent liquidity standing and respectable RoE might help in gaining traction.

Key Metrics (Source: Thomson Reuters)

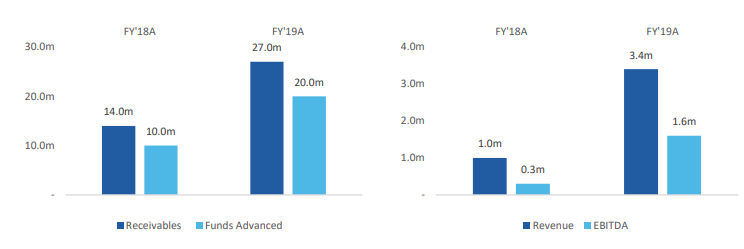

Equipment Finance Division Drives Overall Performance: The company launched equipment finance division in July 2017, and this division has made continuous progress ahead of expectations. Equipment financing division delivered $27 million of receivables on $20 million of funds advanced, helping the division in generating $3.4 million of revenue and $1.6 million in EBITDA in FY 2019. The division has settled more than 250 transactions and proven to be highly complementary to the core Invoice Finance products, with consistent cross-selling opportunities generated, underpinning strong ongoing client retention. Since the division has made continuous progress surpassing the expectations and has also settled a decent number of transactions, it can be said the division might help in the overall growth of the company.

The company would continue to drive growth in Equipment Finance volumes, as the division builds history and scale while maintaining its focus on developing a high-quality loan book. It looks like the development of high-quality loan book might support the performance of the overall division moving forward. The growth is expected to come from existing Equipment Finance team as well as funding structure, with increased profitability delivered from the rise in volumes. The company would seek to transition current debenture funding to the lower-cost warehouse funding structure over the medium term.

Key Metrics Equipment Finance (Source: Company Reports)

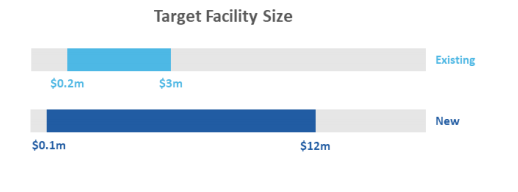

Invoice Financing: During FY 2019, the company made an investment in the development of new product and technology, allowing the company to expand its addressable market to service around 40% of the Invoice Finance market (this reflects 4 times larger than current core factoring market) and diversify its product offering. CGR has traditionally focussed on clients requiring a facility size to $3,000,000 from $150,000, with 95% of clients historically falling within this range. With the expansion into Discounting, the company is currently capable of targeting clients with facilities as large as $12,000,000.

In the second half of the financial year 2019, the company on-boarded its first group of Invoice Discounting clients, providing a relatively immaterial contribution to FY19 Invoices Funded. The company further stated that the investment made in this product has decreased the total earnings of the division. However, these costs have now been absorbed and, on an underlying basis, the business has continued to foster the growth.

Target Facility Size (Source: Company Reports)

Merger to Create a Leading Financial Services Group: Consolidated Operations Group Limited (COG) and CML Group Limited, through a release, announced that they have entered into a Scheme Implementation Agreement. The companies have agreed to a proposed merger for establishing a leading financial services group, which would be having a focus on servicing SME businesses in Australia. The merger would be implemented through a scheme of arrangement with CML shareholders, with the new merged group listed on ASX, initially under COG, with the new name for a merged group to be agreed between the parties.

The shareholders of CML would be having the option to elect to receive 100% of the Scheme consideration in COG shares or to receive a mixture of cash and COG shares. The Scheme consideration includes, (1) scrip consideration of 5.4 COG shares for every 1 CML share held, or (2) cash and scrip consideration of 2.7 COG shares plus A$0.24 for every 1 CML share held (up to the total capped cash amount of A$20 Mn). Scheme meeting of shareholders is planned for January 2020.

Key Update Related to Trade Finance Loan Book & Compliance as at 31 October 2019: In accordance with the Corporate Bond Issue Information Memorandums, which was released earlier on May 18, 2015, the company advised the market players that, as at 31st October 2019, CGR was compliant with all financial covenants contained within the Memorandums. Additionally, at the end of October 2019, the company had trade finance loan book financed by corporate bonds of more than $53.7 million, of which CML supplied actual funding amounting to $24.3 million. It reflects a loan to value ratio of 45.3%.

What to Expect: CML Group Limited is currently well-positioned to continue to build market share and facilitate growth in business volumes in FY20 post investment in HR, technology, new product development and process improvements. The company will increase its investment in client acquisition in FY20, considering the demonstrated month-on-month improvement in new business volumes. Thereare expectations that the company would increase deployment towards sales and marketing.

The company is expecting to achieve increased business volumes in FY20 via (1) Gaining critical mass in the new Invoice Discounting product, with employment of key senior executives as well as current momentum of Invoice Discounting pointing to a contribution of more than 15% to total Invoice Finance volumes in FY20, (2) Continued expansion of core Invoice Factoring product, with an increased addressable market and substantially automated processes. Also, the scaling of Equipment Finance division, with cross-selling from Invoice Finance clients will also help the company to achieve increased business volumes in FY20.

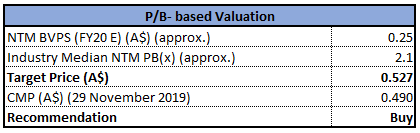

Valuation Methodology: P/BV based approach

P/B- based approach (Source: Thomson Reuters), *NTM: Next Twelve Months

Note: All forecasted figures and peers have been taken from Thomson Reuters

Stock Recommendation: The stock of CGR has witnessed an increase of 5.38% in the time span of the previous one month, while in the past three months, it rose 15.29%. Currently, the stock is trading slightly below the average of 52-week high and low of $0.400 and $0.595. The company has recently wrapped up the acquisition of Classic Finance Group, which was a strategic acquisition having an objective of reinforcing its footprint in Equipment Finance and Confidential Invoice Discounting. The company has acquired a stronger platform for growth, new distribution channels and additional expertise, by bolstering two critical areas such as Equipment Finance and Confidential Invoice Discounting. The acquisition and the existing finance sources also provide in excess of $100m of headroom for further growth of CML Group’s portfolio.

In addition, if the merger between Consolidated Operations Group Limited (COG) and CML Group Limited is successful, Consolidated Operations Group Limited would provide the merged group with a new, strong and a proven distribution channel.COG has approximately 17% of Australia’s broker-sourced asset finance market and provides a large distribution channel for CGR’s Equipment Finance, Factoring and Invoice Discounting products. Considering the decent RoE, favorable expectations about the merger between COG and CML Group Limited and expected synergies related to the acquisition of Classic Finance Group, there are expectations that CGR might achieve respectable growth moving forward. Based on the foregoing, we have valued the stock using a relative valuation method, i.e., P/BV multiple, and arrived at a target price that offers an upsie of high single-digit growth (in percentage terms). Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.490.

CGR Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...