Kalkine has a fully transformed New Avatar.

Company Overview: Cleanaway Waste Management Limited, formerly Transpacific Industries Group Ltd., is a waste management company. The Company's segments include Solids and Liquids & Industrial Services. Its principal activities include offering commercial and industrial, municipal and residential collection services for all types of solid waste streams, including general waste, recyclables, and medical and washroom services; ownership and management of waste transfer stations, resource recovery and recycling facilities, secure product destruction, quarantine treatment operations and landfills; sale of recovered paper, cardboard, metals and plastics to the domestic and international marketplace; collection, treatment, processing and recycling of liquid and hazardous waste, including industrial waste, grease trap waste and used mineral and cooking oils, and providing industrial solutions, including industrial cleaning, site remediation, sludge management, parts washing and emergency response services.

.png)

CWY Details

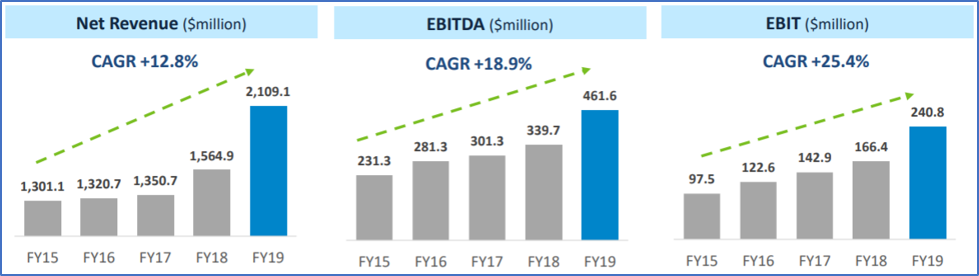

Significant Increase in EBIT and NPAT: Cleanaway Waste Management Limited (ASX: CWY) is a waste management company which operates as a national network of a unique collection, processing, treatment and landfill assets. As on 10 February 2020, the market capitalisation of the company stood at ~$4.01 billion. In the recently held Annual General Meeting, the top management stated that the company made positive progress and posted significant improvements in the financial results in FY19. During FY19, the group’s net revenue witnessed an increase of 35% and stood at $2.1 billion. On an underlying basis, earnings before interest and tax (EBIT) increased by 44.7% to $240.8 million, and net profit after tax (NPAT) grew by 42.8% to $139 million. These results have been driven by the organic growth in revenue, earnings and margins, in addition to the synergies from the acquisition of Toxfree. Growth was further enhanced by the full ramp-up of significant contracts. The decent financial performance of the company enabled the Board to increase the total fully franked dividend by 42% to 3.55 cents per share as compared to 2.5 cents per share in FY18. This brought the full-year dividend payout ratio to 51%, in line with the Board’s target range of 50% to 75% of underlying earnings per share. The company also reported a robust balance sheet with net debt amounting to $658.5 million, representing a net debt to EBITDA ratio of 1.4 times. This ratio indicates that the company is capable of growing continuously and is in a good position to benefit from any opportunities that may arise in the future. In the same time span, cash from operating activities went up by 58.6% to $350.8 million, and free cash flow witnessed an increase of 76.4% to $206.4 million. Over the span of 4 years from FY15 to FY19, the company saw a CAGR of 12.8% in revenue and a CAGR of 27% in net profit after tax.

The company has strengthened its network of prized infrastructure assets and has termed its strategy ‘Footprint 2025’. This will optimise the waste value chain from collection to disposal, with particular focus on resource recovery. The company has upgraded to a contaminated soil treatment facility in Sydney, which is the only facility capable of processing asbestos-contaminated soils. It has planned additional developments for FY20, especially around downstream resource recovery, the Health sector and Energy from Waste.

The company has placed its focus on increasing both pricing and market share, which can be seen in revenue growth during FY19. Cleanaway Waste Management Limited has expanded its service levels over the past years and has several initiatives in progress to serve a large network of commercial and industrial customers based on their waste management needs. The company has a positive outlook for the future years and expects to report better earnings in all the segments, including Solid Waste Services, Industrial Waste Services and Liquid Waste & Health Services.

FY19 Financial Performance (Source: Company Reports)

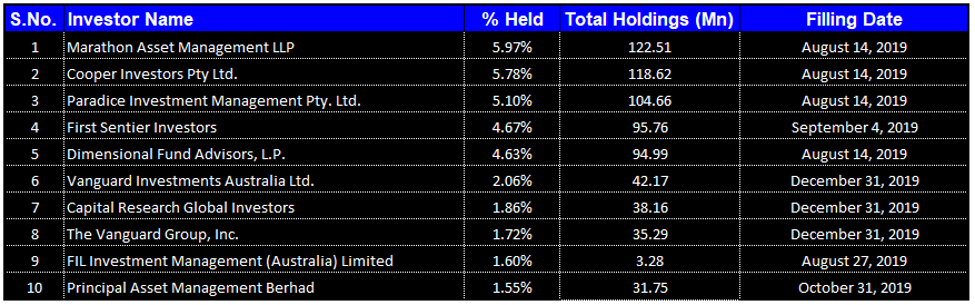

Details of Top 10 Shareholders: The following table provides an overview of the top 10 shareholders of Cleanaway Waste Management Limited. Marathon Asset Management LLP is the largest shareholder in the company, with a percentage holding of 5.97%.

Top 10 Shareholders (Source: Thomson Reuters)

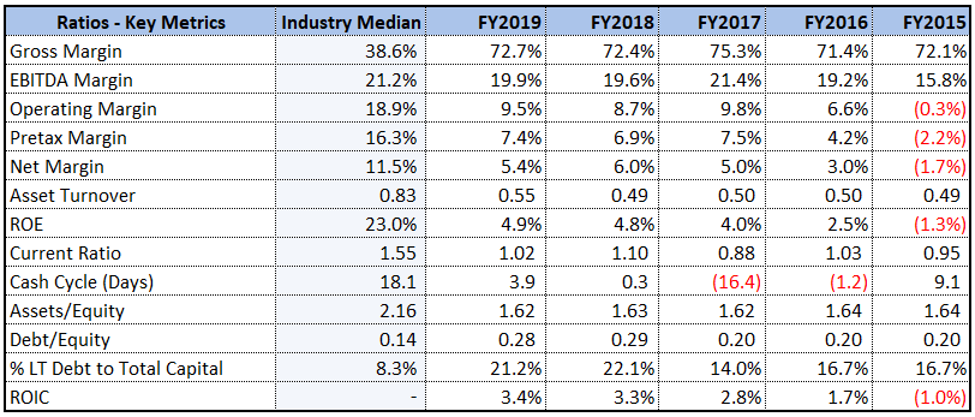

Increasing Profitability and Good Financial Health: During FY19, gross margin of the company stood at 72.7%, higher than the industry median of 38.6%. This indicates that the company is managing its costs well and is capable of converting its revenue into gross profit. Over the span of 4 years from FY15 to FY19, EBITDA margin of the company witnessed an improvement and stood at 19.9% in FY19, implying more profitable operations and indicates good financial health of the company. In the same time span, net margin of the company stood at 5.4%. During FY19, Return on Equity was in line with the previous year and stood at 4.9%. In the same time period, Asset/Equity ratio of the company was 1.62x, lower than the industry median of 2.16x. This indicates that the business is financed with a larger proportion of investor funding and a small amount of debt, resulting in a financially stable balance sheet.

Key Margins (Source: Thomson Reuters)

Completion of Acquisition of SKM Recycling Assets: The company has recently announced that it completed the acquisition of the assets of the SKM Recycling Group for approximately $66 million. The sale proceeds will be utilised to repay the company’s senior secured debt, accrued interest and costs associated with the receivership. This acquisition will provide CWY with a network of five recycling sites, which includes three material recovery facilities, a transfer station in Victoria and a material recovery facility in Tasmania. The company has recently announced that its Materials Recycling Facility in Western Australia caught fire but was brought under control. The company said it would rebuild the site and begin recovering the losses caused due to the incident. The company also informed that the fire will not have a material impact on its underlying EBITDA for H1FY20 or FY20 as a whole.

Launches Plan for Energy-From-Waste Project: The company has recently announced its plan to develop energy from the waste project in Western Sydney, which will utilise the European technology and will convert waste from households and local businesses into electricity. This project is expected to convert electricity for approximately 65,000 Western Sydney homes. The company has also formed a joint venture with Macquarie Capital’s Green Investment Group to develop the energy from waste project. This project will be another milestone for the company’s Footprint 2025 strategy.

Synergies from Toxfree Acquisition: The Toxfree integration remains on track and will provide scale to split businesses by segment to allow greater market focus. The integration of Toxfree is managed through six major categories- 1.) Segment & Business Unit Alignment to Operating Model, 2.) Organisation Design by Segments and Strategic Business Units, 3.) Go to Market Harmonisation, 4.) Property and Infrastructure Footprint, 5.) Group Procurement and 6.) Company Wide Processes and Systems. The acquisition has proven to be highly complementary to Cleanaway and has strengthened its services across the country. The company expects to achieve $35 million in total synergies by June 2020.

Toxfree Synergies (Source: Company Reports)

Growth Opportunities and Future Expectations: CWY will continue to pursue its strategy, which is aimed at improving the profitability, ROCE (Return on Capital Employed), and market position in the upcoming years. The company remains confident with respect to all the three segments- Solid Waste Services, Industrial Waste Services and Liquid Waste & Health Services. It also expects that the first half earnings of FY20 will be in line with the prior corresponding period, owing to decrease in the economic activity, lower commodity prices as compared to the first half of FY19 and a reduction in local Queensland volumes after the introduction of the landfill levy. CWY anticipates that the pricing initiatives and cost reductions which have already been implemented will result in stronger earnings in the second half. The company also gave guidance for FY20 cash capital expenditure and expects it to be approximately 10% of net revenue.

The company is prioritizing to improve driver attentiveness and expects to maintain growth momentum in all of its businesses, especially customer service, while wrapping up the Toxfree integration. The company is working on its Footprint 2025 strategy and expects improved performance despite the outlook for general economic activity in Australia. The company will also formalise the alignment of its mission of sustainable future through its operations to ESG standards. Excluding the positive impact of $35 to $45 million on EBITDA from AASB 16, the company expects FY20 EBITDA to slightly decrease in comparison to FY19.

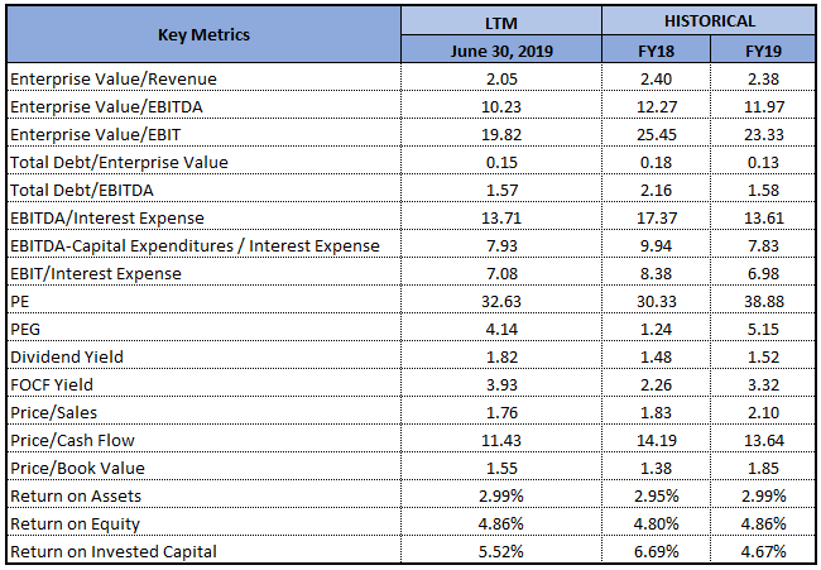

Key Valuation Metrics (Source: Thomson Reuters)

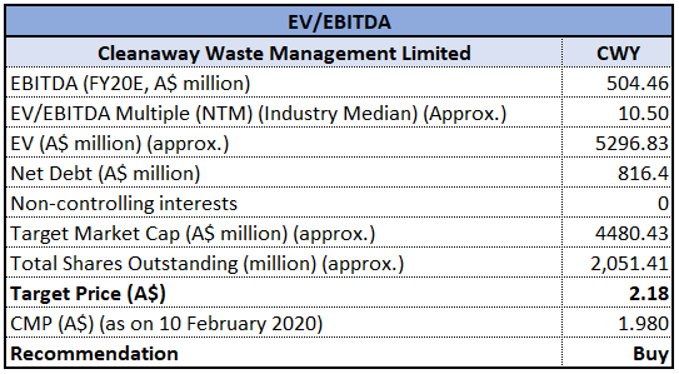

Valuation Methodology: EV/EBITDA based Multiple

EV/EBITDA Multiple Approach (Source: Thomson Reuters)

Note: All the forecasted figures are taken from Thomson Reuters, NTM: Next Twelve Months.

Stock Recommendation: As per ASX, the stock of CWY gave a return of 7.12% in the past three months and is trading below the average of its 52-weeks trading range of $1.625 - $2.525. This offers a good opportunity for investors for accumulation. In the past few years, the company has shown positive trends across all its business segments and is in a strong financial position. The continued investment in Footprint 2025 Strategy resulted in the collection of more recyclables which further resulted in producing higher quality commodity streams. Considering the returns on stock, trading levels, decent financial performance, improving margins and modest outlook, we have valued the stock using EV/EBITDA based relative valuation approach and have arrived at a target upside of lower double-digit (in percentage terms); while we look forward to the earnings results which are expected to be released on 19th February 2020. Hence, we recommend a “Buy” rating on the stock at the current market price of $1.980, up by 1.279% on 10 February 2020.

CWY Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...