Kalkine has a fully transformed New Avatar.

Company Overview: CIMIC Group Limited is an international contractor and contract miner. It provides construction, mining, mineral processing, engineering, concessions, and operation and maintenance services to the infrastructure, resources and property markets. Its segments include Construction, Mining & Mineral Processing, Services, HLG Contracting LLC (HLG), Public Private Partnerships (PPP), Engineering, Commercial & Residential, and Corporate. Construction operates through CPB Contractors Pty Limited. Mining & Mineral Processing operates through Thiess Pty Limited and Sedgman Limited. Services includes UGL Limited's operations. HLG is engaged in construction. PPP includes the Company's project finance division, Pacific Partnerships. Engineering includes its engineering and technical services business. Its projects include Lake Vermont, Mount Owen and Curragh North coal mines; rail and road activities; social infrastructure projects, and QGC Surat Basin project. It operates in over 20 countries.

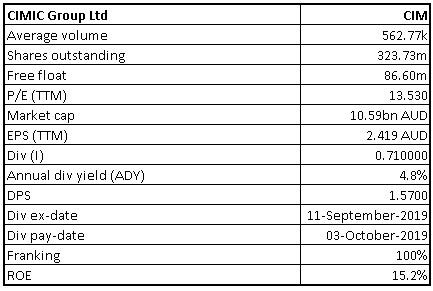

CIM Details

Decent Set of Numbers For 9 Months to September 2019: CIMIC Group Limited (ASX: CIM) carries out operations in infrastructure, resources and property markets. As on October 24, 2019, the market capitalisation of CIM stood at ~$10.59 billion. Recently, the company reported a decent set of numbers for nine months to September 2019, wherein its revenue stood at $10.7 billion and NPAT grew by 2% to $573 Mn. Its EBIT, PBT and NPAT margins were robust, and the figures were 8.2%, 7.3% and 5.3%, respectively. It was mainly driven by a prudent investment in infrastructure and favourable support from its core market. The company has a decent financial position with net cash of $826 million, and the company managed to return $294 million to its shareholders via dividends and share buyback event during the third quarter of 2019. The company’s key personnel stated that the company is on track at the third quarter-end. It was further stated that the positive outlook across the company’s core markets helps its full-year guidance. The company has secured numerous landmark projects during the third quarter of 2019. UGL and CPB contractors together reached contract award, which involves the consideration amounting to $900 million rail, integration and systems alliance package of Brisbane’s Cross River Rail, as well as Thiess, was awarded $1.3 Bn mining services extension at Curragh Mine in Queensland. The company has continued focus on delivering the shareholder returns, and it has announced interim 2019 ordinary dividend amounting to 71 cents per share ($230 million), a rise of 1.4% on a YoY basis, fully franked, which was paid on October 3, 2019. The company has a favourable outlook at the back of (1) strengthening of the mining market, (2) deployment towards infrastructure which has been driving construction and services, and (3) unique position in the growing Public Private and Partnership (PPP) market.

Moving forward, the company’s robust balance sheet, decent fundamentals and dividend-related parameters might help in gaining the interests of dividend-seeking investors. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., EV/Sales and P/E multiples and arrived at a target price of lower double-digit growth (in percentage term). At CMP of $32.580, the stock of the company is trading at P/E multiple 13.14x of CY19E EPS.

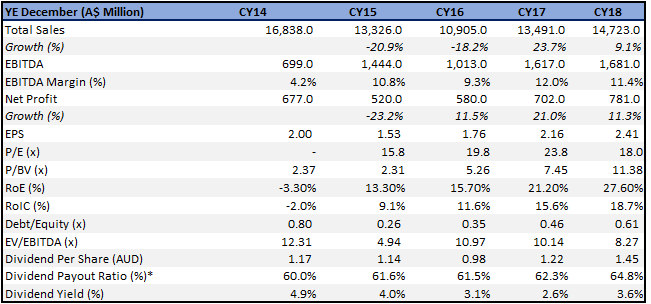

Key Financial Highlights (Source: Company Reports, Thomson Reuters), *estimated at the time the dividend is paid

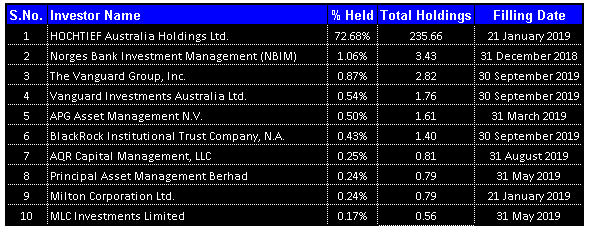

Top 10 Shareholders: The following table provides a brief overview of the top 10 shareholders in CIMIC Group Limited:

Top 10 Shareholders (Source: Thomson Reuters)

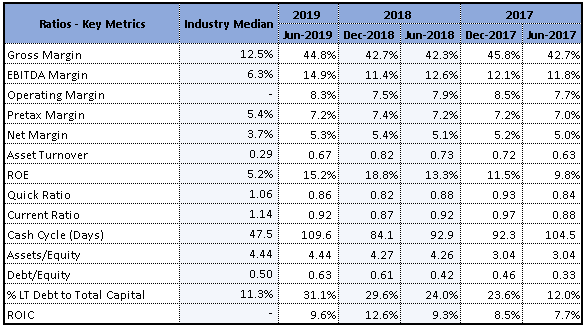

Improvement in Key Ratios Reflects Decent Fundamentals: The company’s net margin stood at 5.3% at the end of June 2019, which reflects a rise from the industry median of 3.7% and, therefore, it can be said that CIM is possessing better capabilities to convert its top-line into the bottom-line as compared to the broader industry. The company’s EBITDA margin stood at 14.9% at the end of June 2019, which is comfortably higher than the industry median of 6.3%. The company’s RoE stood at 15.2% as compared to the industry median of 5.2% and, therefore, it can be said that CIM has delivered better returns to its shareholders than the broader industry. It can be said that the decent fundamentals base and higher returns delivered to the shareholders (as compared to the broader industry) might attract the attention of market players.

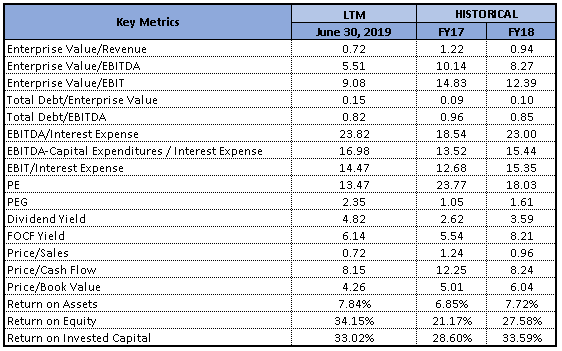

Key Metrics (Source: Thomson Reuters)

Recent Updates: CIMIC Group company, and the wholly-owned subsidiary of CPB Contractors, Broad Construction, was selected by Queensland Government to deliver stages 1 and 2 of new Inner City South State Secondary College in Dutton Park, Brisbane. The release stated that the project would be generating revenue of around $110 million to CIMIC Group. The top management of the company stated that they are optimistic on bringing the group’s leading building capability to deliver the important education facility, which would be serving the student as well as community needs now and for future generations. CIMIC Group company named CPB Contractors, as a part of the rail infrastructure alliance, was selected by the Victorian Government in order to deliver the next stage of works on Sunbury Line Upgrade in Victoria. The works would be providing upgrades to the rail network’s power system, generating revenue amounting to around $158 million to CPB Contractors. This happens to be the second package of Sunbury Line upgrade works, which has been awarded to Alliance.

Announcement About Refinancing Syndicated Bank Facility: CIMIC Group Limited recently made an announcement that it has refinanced the core working capital cash facility, as part of a long-term financing strategy. The press release also stated that the new syndicated bank facility is for $1.9 Bn, which has been split equally across the 2 tranches of four as well as five years. The company stated that it replaces the existing tranche in the company’s current facility, that matures in the month of September 2020, and some maturing US dollar debt. The company key personnel stated that the successful refinancing implies credit strength, leading market position as well as a strong partnership with the relationship banks.

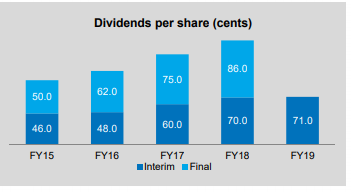

Growth Trajectory in Interim Dividend Continues: The company has declared interim 2019 ordinary dividend amounting to 71 cents per share (or $230 million), reflecting a rise of 1.4% on a YoY basis, fully-franked, that has been paid on October 3, 2019. It has also declared a final ordinary dividend for the 2018 year, which amounted to 86 cents per share (or $279 million), reflecting a rise of 15% on a YoY basis, fully-franked, which was paid on July 4, 2019. During the nine months ended September 2019, the company has repurchased 527,341 shares, which involve an average price amounting to $31.67. For six months ended June 30, 2019, the company’s payout ratio stood at 62.8%.

Dividends Per Share Trend (Source: Company Reports)

Announcement About Changes To CIMIC’s Board: CIMIC Group has recently advised that Trevor Gerber would be resigning as an Independent Director and the resignation would become effective on December 31, 2019. The release stated that Mr Gerber has cited the appointment as the Chairman of Vicinity Centres, which would be effective from November 2019, as a reason for decision made.

Key Valuation Metrics (Source: Thomson Reuters)

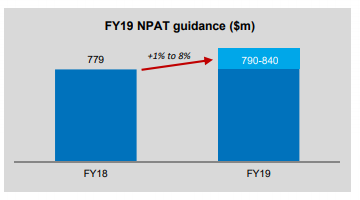

What To Expect From CIM Moving Forward: The company has confirmed its guidance for 2019, and there are expectations that its NPAT would be in the range of $790 million -$840 million, however, it is subject to the market conditions. CIM stated that positive outlook throughout the group’s core markets supports the guidance and mining market has been strengthening, and the opportunities in Construction and Services are being boosted by the robust PPP pipeline. The image relates to the FY 2019 NPAT guidance:

FY 2019 NPAT guidance ($ million)

The company is possessing a robust balance sheet, and this continues to give flexibility to the company to pursue the strategic growth initiatives as well as capital allocation opportunities, and to deliver the shareholder returns. There happens to be a $20 billion pipeline of the construction, mining and services opportunities for the rest of 2019, extending to $475 Bn for 2020 and beyond. It was further added that this pipeline includes approximately $130 billion of the PPP opportunities which have been identified for the remainder of 2019 and beyond. The company continues to make progress on the objectives, and it is in a robust financial position, which might help the overall company in achieving long-term growth objectives.

Valuation Methodologies:

Method 1: EV/Sales Valuation Multiple

(6).png)

EV/Sales Valuation Multiple (Source: Thomson Reuters)

Method 2: Price to Earnings based Valuation

(3).png)

Price to Earnings based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM: Next Twelve Months

(16).png)

Historical PE Band (Source: Thomson Reuters)

Stock Recommendation: The stock of CIM has witnessed a fall of 5.76% in the span of previous three months while, in the time frame of previous six months, the company’s stock has witnessed a decline of 33.93%. As per ASX, the stock price is trading lower to the 52-week low high average and, therefore, it can be said that it is offering a decent opportunity to make an entry. The company is having a diversified order book and has an extensive pipeline which could help it moving forward. In the presentation for nine months to September 2019, the company stated that its work in hand amounted to $37.2 billion, which reflects a rise of 6% on a YoY basis, and this gives good visibility. In LTM, the company generated operating cashflow amounting to $1.7 billion as well as free operating cash flow amounting to $803 million. The company has been maintaining a strict focus towards managing the working capital as well as generating sustainable cash-backed profit, which could help the company is gaining traction among the market participants. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., EV/Sales and P/E multiples and arrived at a target price of lower double-digit growth (in percentage term). Hence, we give a “Buy” rating on the stock at the current market price of A$32.580 per share (down 0.428% on 24 October 2019).

CIM Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...