Kalkine has a fully transformed New Avatar.

Company Overview - ChimpChange Limited (ChimpChange) is an Australia-based company, which is principally engaged in providing mobile banking services through the ChimpChange mobile application. The Company operates in the United States banking and financial services market. The Company's application allows mobile payments and transactional banking. The Company's application also allows its customer to get linked with ChimpChange prepaid MasterCard that can be used to make in-store/online purchases, pay bills and withdraw cash everywhere debit MasterCard is accepted. The Company also intends to provide its customers with digital banking. The Company's subsidiaries include Chimpchange LLC and Change Labs NZ Pty Ltd.

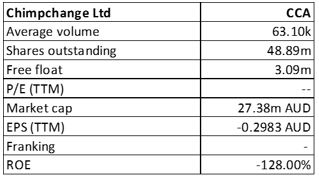

CCA Details

Double-digit month-on-month growth and acquisition of the customers on track as per target: ChimpChange Ltd (ASX: CCA) expanded their customer base by 15,500 customer during the September quarter of 2016 which is in line with the targeted acquisition cost of $25. CCA has a target to acquire 25,000 new customers by the end of December 2016 and is on track to deliver this growth. Moreover, CCA is focusing on acquiring higher quality customers and increasing the activity of its customer base. The higher quality customers regularly deposit and transact on the platform which would drive their business momentum. CCA had a positive momentum in the September quarter and expected this trend to continue even in the month of October. The group thus recently reported for addition of 7,000 new customers in October. The group is witnessing double-digit month-on-month growth across its transactional metrics.

Strengthening portfolio: CCA business continues to strengthen their portfolio and accordingly the group released the new features like mobile cheque load feature. The group had successfully executed their marketing programs and expects a better transaction spending given their growing customer base in the September quarter. CCA has several new features in the pipeline which could drive their growth in the coming periods. CCA’s business is growing positive in terms of the customer activation rate, active adoption rate, activity per user, and swipe size. Additionally, CCA in the second half of FY 16 had raised A$15 million (before costs) and got listed on the ASX. Further CCA had re-negotiated the transaction costs to significantly reduce the cost of goods sold and give a positive gross margin. These efforts make them well positioned for future while the group expects a better gross margin as well aims to generate a further value to the shareholder. Moreover, in the September quarter CCA’s net operating cash showed an outflow of US$1.76 million (A$2.3 million) and the cash was US$8.97 million (A$11.8 million).

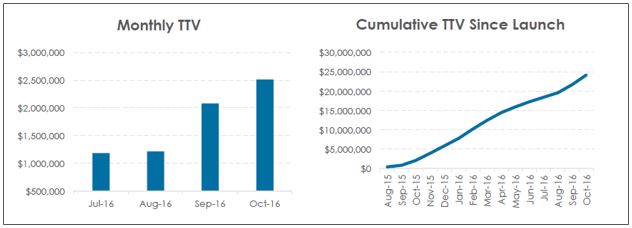

Strong Growth of the Total Transactional Volume (TTV) and customer deposits: CCA’s Total Transaction Volume has grown by 71% month-on-month in September 2016 reaching US$4.4 million (A$5.9 million) for the quarter of which the September month represented 46%. At the end of the September quarter, CCA had processed over US$20 (A$26 million) in total transactions. With regards to the customer deposits, CCA has seen positive growth in the September quarter of 2016 driven by solid performance in September month. The first two months of the quarter have seen the deposits growth. But during the September month, the deposits reported an outstanding growth of 73% on a month on month basis representing a new high since re-launch. This indicates growing attraction of higher value customers to the group’s products which has the capability to offer customers with new avenues to deposit funds. Additionally, CCA has grown its average deposit size by more than 250% since launch. The deposits are on track to deliver strong growth in the December quarter. In October, the TTV grew by 21% month-on-month while the total funds grew by 17% on month-on-month basis.

CCA’s Total Transaction Volume (Source: Company Reports)

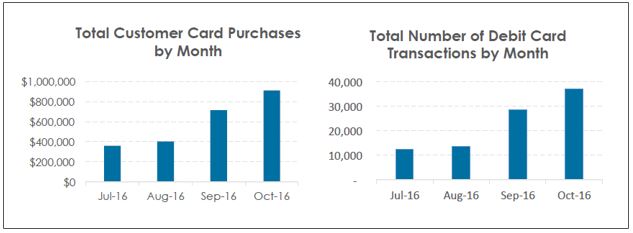

Growth in the Customer Card Purchases is more than industry average: CCA has reported 18% quarter on quarter growth in the Customer Card Purchases, driven by the deposit growth of the customers who are improving their proportion of funds to make purchases by debit card, rather than ATM withdrawals. There is an increase in the average purchase size, which resulted in a higher margin per transaction during the quarter by CCA. Additionally, CCA for debit card purchases in the first two months of the quarter has an average purchase size of approximately $29 and in September it was approximately $25 (which remains higher than what CCA got pre-IPO). These average purchase sizes are greater than the industry average for debit card purchases of approximately $24. As a result, the purchases over approximately $5 lead to positive gross margin to CCA. In October, the total customer purchases surged by 26% on a month-on-month basis. The debit card purchases are expected to deliver strong growth in the December quarter.

Growth in the Customer Card Purchases and Debit Card Transactions (Source: Company Reports)

Launch of innovative photo cheque load feature: CCA had launched the innovative photo cheque load feature in the first quarter of fiscal year of 2017. The cheques are regarded as antiquated Australia but over in the United States, the cheques are very much part of the system and represent 13% of all non-cash payments in North America based on the World Payment Report. This US market offers a huge potential opportunity to the group as the group is offering affordable banking experience. CCA had surveyed their customers and found that CCA’s cheque load tool would be hugely valuable and drive them to use CCA as their primary transactional account. Accordingly, their customer’s growth would also continue in the coming years. In addition, the new feature will assist in driving the total transaction volume and revenue. Moreover, CCA had anticipated that 90% of customers would select the expedited option (to clear within minutes) and the September quarter has exceeded the initial targets. In the September quarter, more than 97.6% of users chose to clear cheques within minutes. Additionally, CCA had posted that the deposits made through the photo cheque load feature represented 5.69% of total deposit volume at the end of end of September. It is expected the adoption of this would continue to grow and for deposit volume from the photo cheque load feature to exceed 7% over the coming months.

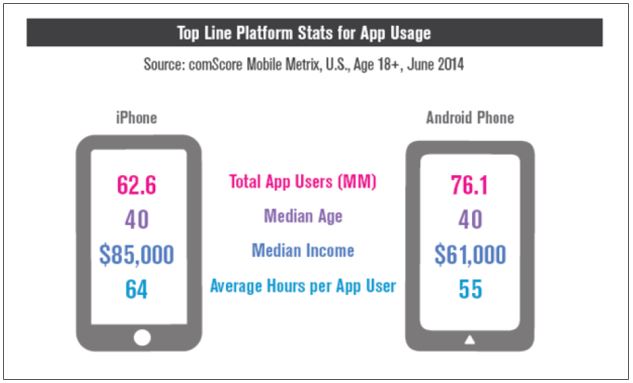

Top line platform stats for App Usage as of September Report (Source: Company Reports)

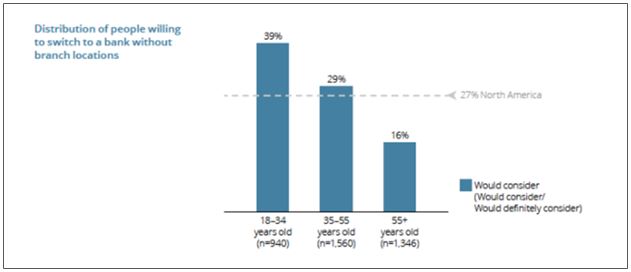

Positive outlook: FY 16 was a transformational year for the company as CCA platform started to earn fees from November 2015 and only minimal revenue was received. The fees earned was related to interchange fees, out-of-network ATM fees and other platform fees. The group’s first quarter of 2017 performance was also good. Even though the Australia technology company’s performance is considered volatile, management believes that consumer’s demand for the group’s digital banking products would continue in the coming periods while we believe US markets would play a major role in this growth. A survey-based analysis has shown that more than one in four customers preferred branchless digital bank if they were to switch from their current bank. Younger customers opted this preference more as they are less interested in convenient branch locations and more interested in accessing digital services at their preferred time and place. It has been estimated that mobile-only users make up about 15% of a typical financial institution’s mobile banking user base. Moreover, the survey reported that over 70% of Millennials preferred to bank with a company that they currently do business with but do not currently offer banking services, with examples being trusted digital brands. On the other side, while analyzing the group’s potential opportunity, management quoted few examples of their international comparables. Number26, a European based digital bank had raised US$40 million privately in June 2016 and added 200,000 customers since its launch in 2015. Given the current scenario, the group expects rapid growth especially in their deposits and debit card purchases, and is on track to generate a solid growth during the December quarter. As a result, management is focusing on marketing efficiency and daily acquisition rates to achieve their goals. The group invested over US$1.1 million for the September quarter on customer acquisition and on their new upcoming product features.

Survey results (Source: Company Reports)

Stock Performance: The shares of CCA stock fell over 1.6% in the last three months (as of November 07, 2016) due to softening Australian technology industry coupled with uncertain conditions in the US ahead of election results but rose 24% in the last one month. On the other hand, we believe CCA is a long-term growth driven investment and investors can leverage the opportunity to enter the stock. The group has a long list of planned product launches to boost its top line in the future. All the key metrics, especially deposits and debit card purchases, are on track to deliver strong growth in the December quarter. US digital banking offers solid potential opportunity for CCA while targeting Millennials could drive their performance further. The group will hold its AGM on November 28, 2016. We give a “Buy” recommendation on the stock at the current price of – $ 0.60

CCA Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...