Kalkine has a fully transformed New Avatar.

Company Overview: Challenger Limited is an Australia-based investment management company. The Company operates through two segments: Life and Funds Management (FM). The Life segment includes Challenger Life Company (CLC), which provides annuities and guaranteed retirement income products, and Accurium Pty Limited, which provides self-managed superannuation fund actuarial certificates. It distributes products under the Life segment through independent financial advisors and financial advisors that are part of hubs. The FM includes Fidante Partners and Challenger Investment Partners (CIP). Fidante Partners encompasses a range of associate investments in boutique investment managers. Fidante Partners provides administration and distribution services to the boutiques and shares in the profits of these businesses. CIP develops and manages assets under the Company's brand for CLC and third-party institutional investors. The investments managed by CIP include in fixed income and commercial property.

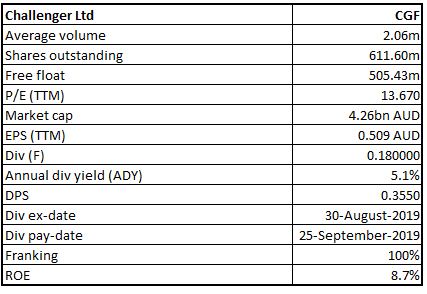

CGF Details

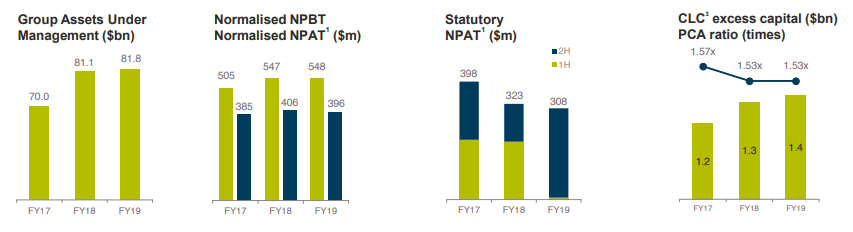

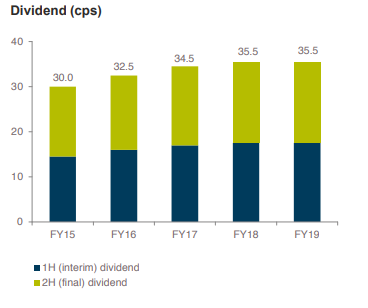

Group’s AUM Rose 1% And Pay-out Ratio Is Above Guidance Range: Challenger Limited (ASX: CGF) is a mid-cap investment management company with the market capitalisation of ~$4.26 Bn as of 09 September 2019. It has two operating segments, i.e., Life and Funds Management. Recently, the company released its results for FY19 in which group's assets under management (AUM) were recorded at $81.8 billion, exhibiting a rise of 1% on a YoY basis. The company has continued to attract robust retail inflows in Funds Management and Life, even though the retail flows throughout the sector were hitting record lows last year. Additionally, the company’s capital position remains strong with its Prescribed Capital Amount (PCA) ratio of 1.53x, which is towards the top-end of the target range of 1.3x to 1.6x. The results reflect resilience of the business in the face of challenges in the operating environment this year caused by a significant disruption in the advice industry. With respect to the business outlook, the company’s key personnel has reflected favourable views and stated that CGF is well-positioned to capture the opportunities for the growth in its Life and Funds Management businesses and there are expectations that the superannuation industry assets might get double over the next 10 years. The company is responding to the current environment with the range of initiatives in order to address adviser disruption the company faces, and it continues to implement its strategy for long-term growth. The company has maintained a strong capital position with $1.5 billion of excess regulatory capital and Group cash, reflecting a rise of $0.1 billion due to higher retained earnings and lower capital intensity. Based on the FY19 performance, the Board of Directors declared a fully-franked final dividend of 18.0 cps, bringing the full year dividend to 35.5 cps (fully-franked) which is in-line from the prior year. The company’s FY 2019 dividend payout ratio stood at 54.2% and was above the guidance range of between 45% and 50% of normalised profit after tax. This reflects confidence in future growth and strength of the capital position. The final dividend will be paid on 25 September 2019. The growth in Australia’s superannuation system is supported by the mandatory contributions, which are scheduled to increase from 9.5% of the gross salaries to 12.0% by 2025. The growth in superannuation system is supported by the changing demographics as well as the government enhancing the retirement phase of the superannuation. It was mentioned that Life and Funds Management might benefit from the growth in Australia's superannuation system.

FY 2019 Outcomes (Source: Company Reports)

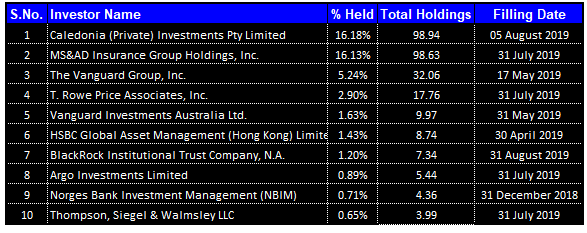

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Challenger Limited:

Top 10 Shareholders (Source: Thomson Reuters)

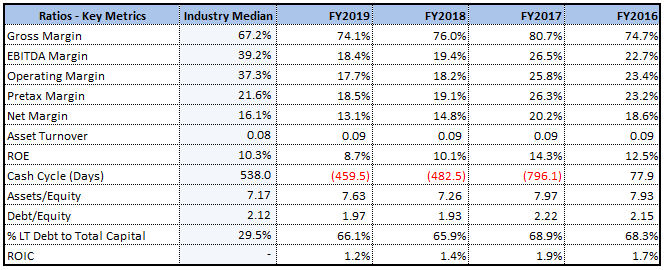

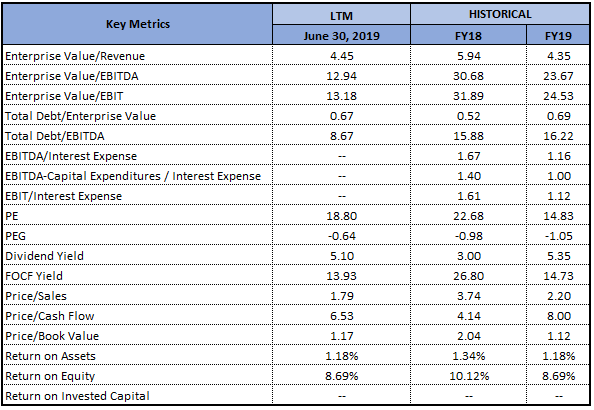

Decent Key Margins: The company’s key margins can be considered at decent levels in FY19 as its net margin stood at 13.1% while its EBITDA margin stood at 18.4%. Challenger’s gross margin stood at 74.1% in FY19, which is higher than the industry median of 67.2%. In FY19, the company’s Debt/Equity ratio stood at 1.97x, which is lower than the industry median of 2.12x and, therefore, it looks like that the company’s balance sheet is comparatively deleveraged as compared to the broader industry. Generally, a less leveraged balance sheet reflects stability and can help a particular company in delivering long-term growth objectives. Also, lower debt on the balance sheet reduces the company’s commitments and, as a result, the company could focus on its growth plans. RoE stood at 8.7% in FY19.

Key Metrics (Source: Thomson Reuters)

Appointment of MS&AD Representative to The Board: CGF’s Chairman named Peter Polson has recently made an announcement about the appointment of Mr Masahiko Kobayashi as Non-Executive Director of Challenger Limited. The appointment follows an expanded strategic relationship with MS&AD Insurance Group Holdings Inc. (or MS&AD) which was announced in the month of March 2019. As part of a strategic relationship, MS&AD has increased the Challenger shareholding to more than 15% of the issued capital and Challenger commenced reinsurance of the US dollar denominated annuities issued by the Mitsui Sumitomo Primary Life Insurance Company Limited (MS Primary), which is a subsidiary of MS&AD, on July 1, 2019. Mr Kobayashi would be joining Challenger Limited Board.

In the release, it was also mentioned that Mr Kobayashi would also be joining the Challenger’s Nomination Committee. In accordance with the constitution, Mr Kobayashi would be standing for the re-election at Challenger’s 2019 AGM which has been scheduled for October 31, 2019.

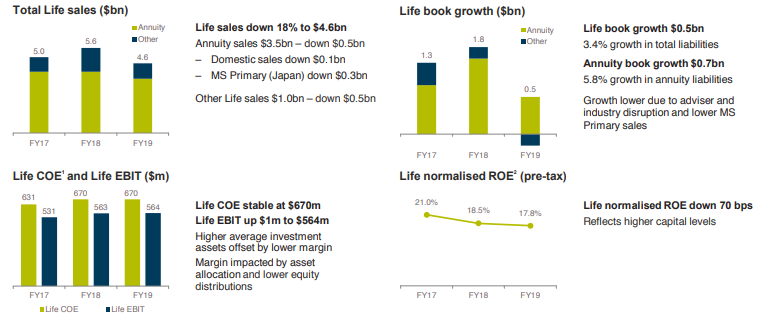

Understanding Performance of Challenger Life: Challenger Life earnings were steady for the year, and the book growth was offset by lower margin. The normalised earnings before interest and tax (or EBIT) witnessed a rise of $1 million and stood at $564 million which reflects stable normalised cash operating earnings (or COE) of $670 million and stable expenses. In the release, it was mentioned that total life sales stood at $4.6 billion, which reflects a fall of 18% on FY18. It included lower annuity sales, which was down $0.5 billion and stood at $3.5 billion, and lower Other Life sales, which was also down $0.5 billion to $1 billion. The biggest driver with respect to the decline in the annuity sales was MS Primary sales in Japan, which fell 54% because of higher US interest rates relative to Australia.

Life Result (Source: Company Reports)

There are expectations that the contribution from MS Primary might increase in FY20 following an agreement with Challenger to reinsure the US dollar annuities in Japan, which commenced on July 1, 2019. Additionally, it was stated that the minimum FY20 volumes will be around $660 million, and this agreement will continue for a minimum period of 5 years.

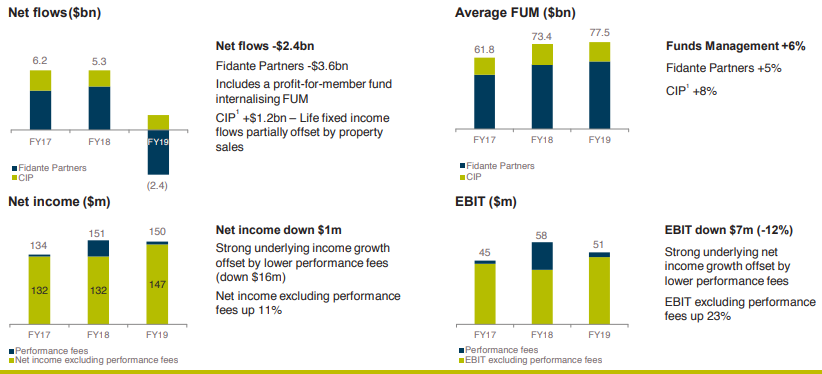

How Funds Management Performed in FY19: In the Funds Management business, robust underlying earnings got offset by the lower performance fees, which fell $16 million and stood at $3 million. As a result of this, the net income for the year encountered a fall of $1 million and stood at $150 million, but there was a rise of $14 million excluding the performance fees. It was also mentioned that the average FUM rose by 6% and stood at $77.5 billion, which includes Fidante Partners FUM which were up 5% and stood at $58.6 billion and Challenger Investment Partners (or CIP) which rose by 8% and stood at $18.9 billion.

Funds Management Result (Source: Company Reports)

What to Expect From CGF Moving Forward: The company stated that, while FY19 performance was impacted by the disruption throughout Australian wealth industry, the business happens to be in good shape to navigate current operating environment as well as it is well placed to capture the opportunities as they emerge. In FY20, the challenging operating conditions are anticipated to persist for the domestic sales and the company is targeting normalised net profit before tax in the ambit of $500 million and $550 million. It reflects $23 million in the earnings impact because of the lower equities normalised growth assumption and investment in the range of initiatives of up to $15 million in order to drive the future growth. There are expectations that the company’s dividend would be maintained at 35.5 cents per share in FY20, and the pay-out ratio is expected to be above 45%-50% range. However, it is subject to the market conditions and capital allocation priorities.

Dividend (cps) (Source: Company Reports)

The company’s priorities primarily include improving the adviser experience, leveraging MS&AD strategic relationship and maintaining the financial discipline and robust capital position.

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodologies:

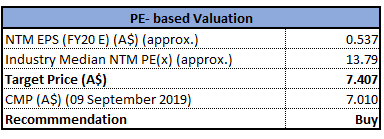

Method 1: PE- based Valuation

PE- based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

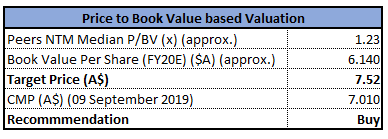

Method 2: Price to Book Value based Valuation

Price to Book Value based Valuation (Source: Thomson Reuters), *NTM: Next Twelve Months

(Note: All forecasted figures and peers have been taken from Thomson Reuters)

Stock Recommendation: The stock of Challenger Limited has fallen 17.14% in the span of previous six months, while in the time frame of the past three months, it witnessed a fall of 12.56%. Currently, the stock is trading towards its 52-week low levels of $6.22 with reasonable PE multiple of 13.67x, indicating a decent opportunity for accumulation. Moreover, the company is strongly capitalised, which might help it in gaining traction among the market participants moving forward. Commencing in FY20, the company’s normalised ROE (pre-tax) target was revised from 18%, which is to be based on the RBA cash rate plus a margin of 14%. The change in the ROE target reflects the structural change with respect to the interest rates, which are expected to be lower for longer. Using the ROE target based on Reserve Bank of Australia cash rate removes the interest rate impact from ROE target. Based on the foregoing, we have valued the stock using two relative valuation methods, i.e., Price to Earnings multiple and Price to Book Value multiple and have arrived at the target price upside of high single-digit growth (in percentage term). Hence, we give a “Buy” recommendation on the stock at the current market price of A$7.010 per share (up 0.718% on 9 September 2019).

CGF Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...