Kalkine has a fully transformed New Avatar.

Company Overview: Challenger Limited is an Australia-based investment management company. The Company operates through two segments: Life and Funds Management (FM). The Life segment includes Challenger Life Company (CLC), which provides annuities and guaranteed retirement income products, and Accurium Pty Limited, which provides self-managed superannuation fund actuarial certificates. It distributes products under the Life segment through independent financial advisors and financial advisors that are part of hubs. The FM includes Fidante Partners and Challenger Investment Partners (CIP). Fidante Partners encompasses a range of associate investments in boutique investment managers. Fidante Partners provides administration and distribution services to the boutiques and shares in the profits of these businesses. CIP develops and manages assets under the Company's brand for CLC and third-party institutional investors. The investments managed by CIP include in fixed income and commercial property.

.png)

CGF Details

Rebound in Investment Markets Reinforced Total AUM Growth: Challenger Limited (ASX: CGF) happens to be a leading investment manager and annuity provider whose principal activities revolve around Life and Funds Management. As on June 3, 2019, the market capitalisation of CGF stood at A$4.94 billion. It had recently released its results for Q3 FY 2019 in which its total assets under management (or AUM) witnessed a rise of 4% and stood at $81 billion because of the rebound witnessed in the investment markets. The company had made progress with respect to implementing the strategies to build further resilience through an expanded relationship with MS&AD in Japan and new domestic distribution relationships. The company’s top management stated that annuity sales have been impacted by the lower Japanese sales and general disruption in the financial advice market in Australia. However, even though the annuity sales via major hubs were down, the company is witnessing resilience in other sectors of the advice industry with robust growth in sales by the independent financial advisers (or IFAs).

The growth in IFA sales implies the evolution of advice industry over the past twelve months and helps the company’s strategy to expand the distribution reach via IFAs. There are expectations that Challenger annuities would be rolled out on independent platforms, i.e., Hub24 and Netwealth before the financial year-end. Total Life net flows for the quarter ended March 2019 were an outflow amounting to $170 million, which represents annuity net inflows of $66 million offset by the net institutional outflows of $236 million. The annuity sales by the major advice hubs amounted to $352 million in Q3, which reflects a reduction of 24% on pcp. The results got partially offset by the robust growth in the IFA sales of $255 million, reflecting a rise of 33% on pcp basis.

Moving forward, strong capital position, decent dividend payout ratio, expansion of strategic partnership with MS&AD, growing retirement income market, expansion of distribution reach, strong brand and reputation, new product and distribution initiatives are expected to act as tailwinds for Challenger. Additionally, favourable FY 2018 leverage ratios might support the long-term growth prospects of the company.

.png)

Life Asset Allocation (Source: Company Reports)

Top 10 Shareholders: The following table provides a broad picture of top 10 shareholders in Challenger Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

Analysing CGF’s Margins’ Position: In 1H FY 2019, the company’s gross margin stood at 87.6% which is higher than the industry median of 74.1% which implies stronger revenue-generation capabilities as compared to the broader industry. During the same period, its Asset/Equity ratio and Debt/Equity ratio stood at 7.81x and 2.10x, respectively. Similarly, amidst certain macroeconomics challenges, the company generated positive returns for its shareholders than its peers with an ROE of 0.2% in 1HFY19. EBITDA margin and net margin stood at 13.0% and 0.7%, respectively in 1HFY19.

.png)

Key Metrics (Source: Thomson Reuters)

Understanding Life’s Results for Q3 FY 2019: The total annuity sales amounted to $662 million, which reflects a fall of $99 million (or 13%) on prior corresponding period, because of lesser contribution from MS Primary (Japanese) sales and lower Australian annuity sales. MS Primary sales amounted to $55 million, which got reduced by 49% on pcp because of increased US interest rates relative to Australia which led to the reduction in the demand for Australian dollar denominated products in Japan. The Australian annuity sales got impacted by the disruption witnessed in retail financial advice market following the Royal Commission which had led to the reduction in the new client acquisitions and increased adviser churn. Life’s investment assets as at March 31, 2019 amounted to $18.6 billion and were unchanged for March quarter. The company continued to reduce the exposure towards property during March 2019 quarter with several properties anticipated to settle during Q4 FY 2019. Challenger’s allocation towards property is anticipated to reduce to mid-teens percentage by FY 2019 end.

Life Investment Assets (Source: Company Reports)

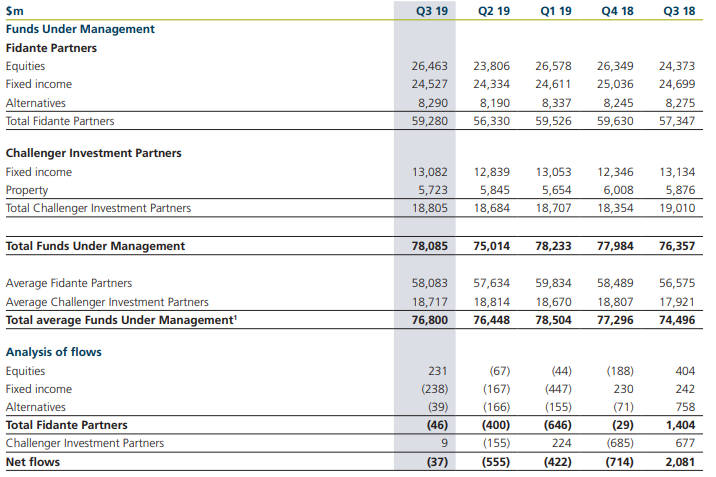

Funds Management FUM Rose 4% in Q3FY19: The FUM (or Funds under Management) of Funds Management at quarter end amounted to $78.1 billion, which implies a rise of $3.1 billion or 4% for the quarter. FUM was helped by positive investment markets which were partially offset by the net outflows amounting to $37 million for the quarter. Fidante Partners’ FUM stood at $59.3 billion, which implies a rise of 5% for the quarter. Challenger Investment Partners’ FUM amounted to $18.8 billion, which implies a rise of 1% for the quarter.

Funds Management (Source: Company Reports)

Strategic Relationship With MS&AD: CGF had progressed the strategic relationship with MS&AD Insurance Group Holdings Inc. in order to support CGF’s strategy for the growth in Australia and Internationally. With respect to the new arrangement, CGF would be commencing a quota share reinsurance of US dollar denominated annuities issued in the Japanese market by Mitsui Sumitomo Primary Life Insurance Company Limited (MS Primary), which is a subsidiary of MS&AD, and is anticipated to commence from July 1, 2019. MS Primary would be providing Challenger Life an annual amount of reinsurance, across Australian and US dollar annuities, amounting to at least ¥50 billion (currently ~A$640 million) per year for a minimum of 5 years. This amount is based on the exchange rate of 0.012839 as at 25 March 2019.

MS&AD has intentions to increase Challenger shareholding to more than 15% of the issued capital and seek representation on Challenger Limited Board, subject to the required regulatory approvals and market conditions. The expanded relationship with MS&AD builds on CGF’s successful relationship with MS Primary and broaden access to Japanese markets while diversifying the exposure throughout the different currency products. The top management of Challenger had stated that the expanded alliance leverages the strength of both businesses to create opportunities for growth.

Key Takeaways from Macquarie Australia Conference 2019: The top management of Challenger Limited stated that expansion of the relationship with the MS&AD Group diversifies the access to Japanese annuities market and delivers certainty by underpinning and increasing sales of the annuities into Japan. Challenger also stated that increasing allocation towards secure and stable income happens to be fundamental to its vision. Challenger annuities are compelling when it comes to assisting retirees to manage the longevity risk, inflation risk, and sequencing risk, but they are also compelling with respect to delivering good value.

The management of the company is optimistic about the long-term fundamentals of its business and strong systemic tailwinds that would be driving the business forward over the longer term. There are expectations that the retirement income market would be going to grow as the population ages and the system matures. However, the management believes that they are well positioned with regards to those changes.

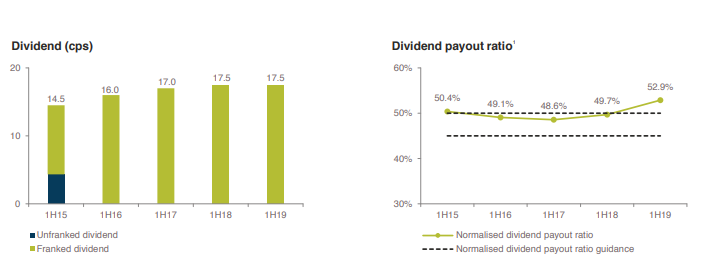

What to Expect from CGF Moving Forward: Challenger Limited happens to be well positioned as it possesses robust product offerings, expanding distribution networks as well as highly efficient operations which might help the company moving forward in terms of tackling the industry-wide challenges. Another favorable factor which the company possesses is dividends as it has managed to declare an interim dividend amounting to 17.5 cents in 1H FY 2019 which is in line as compared to 1H FY 2018 amidst certain challenges. This reflects decent fundamentals of Challenger Limited. The 1H FY 2019 interim dividend equates to the Normalised dividend pay-out ratio of 52.9% which can be considered at respectable levels. The Company’s Board has been targeting a dividend pay-out ratio of between 45%- 50% of the normalised profit after tax.

Dividend (Source: Company Reports)

Coming to the expectations for 2HFY19, the company has been focusing on building relationships, and innovate such as launching annuities products on various platform. It also has its focus on active management of Life’s investment portfolio. For 2019, the company had revised the expected earnings range from 8% to 12% growth on 2018 ($591.0 million to $613.0 million) and it now anticipates normalised net profit before tax in the range of $545 million- $565 million. The lower expectation reflects 1H normalised net profit before tax and flow on into 2H FY 2019 and changes to Life’s investment portfolio to reduce the capital intensity. The normalised cost-to-income ratio is anticipated to remain between 30%–34% over the medium term.

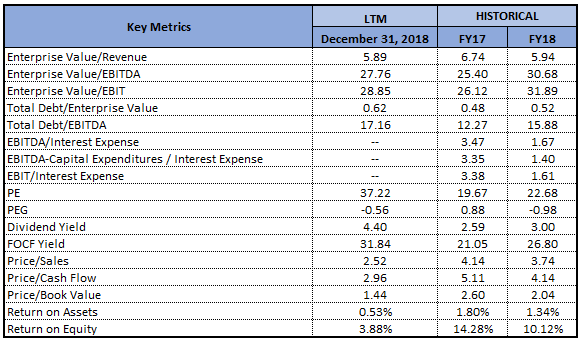

Key Valuation Metrics (Source: Thomson Reuters)

Valuation Methodology:

Method 1: PE- based Valuation

.png)

PE- Based Valuation (Source: Thomson Reuters), *NTM-Next Twelve Months

Stock Recommendation: The stock of Challenger Limited had witnessed the fall of 19.62% in the span of previous six months and, in the time frame of past three months, it had fallen 3.70% which reflects the negative factors, more or less, have been discounted at the current juncture. It looks like the stock has potential to witness further growth and robust capital position, appealing product offering, and expansion of distribution reach are expected to drive CGF’s performance moving forward.

Challenger Limited happens to be strongly capitalised and there are expectations that the capital intensity would be reducing further which might attract the attention of market participants. Hence, considering a decent capital position and dividend pay-outs ratio, we have valued the stock using Relative valuation method, P/E and arrived at the target price upside in single digit (%). Hence, considering aforesaid parameters and current trading level, we are affirmative on the stock, and recommend a “Buy” rating on the stock at the current market price of A$7.890 per share (down 2.23% on 3 June 2019).

CGF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...