Kalkine has a fully transformed New Avatar.

Company Overview: Centrepoint Alliance Limited is a financial services company. The Company is a provider of a range of financial advice and licensee support services (including licensing, technology, business support, training, compliance and professional standards) to financial advisers and accountants across Australia. The Company operates through two segments: Licensee and Advice Services, and Funds Management and Administration. Licensee and Advice Services segment provides Australian Financial Services License related services to financial advisers and their clients and mortgage broking services. It’s Funds Management and Administration segment provides investor directed portfolio services and investment management services to financial advisers, accountants and their clients. It also provides lending mortgage aggregation services to mortgage brokers. Its subsidiaries include Centrepoint Alliance Lending Pty Ltd, Associated Advisory Practices Pty Ltd and Professional Investment Services Pty Ltd.

.png)

CAF Details

Decent Performance in FY19: Centrepoint Alliance Limited (ASX: CAF) and its controlled entities are engaged in the operation of financial services industry within Australia and it provides a range of financial advice and licensee support services (which includes licensing, systems, compliance, training and technical advice) as well as investment solutions to financial advisers, accountants and their clients throughout Australia, and lending mortgage aggregation services to the mortgage brokers. As on September 27, 2019, the market capitalisation of CAF stood at ~$17.12 million. The company has made an announcement about the financial results for the year ended June 30, 2019 (or FY19). The company reported profit before tax amounting to $1.2 million as compared to FY18 loss figure of $3.4 million while its EBITDA amounted to $2.4 million in FY19. The company’s Chief Executive Officer named Angus Benbow stated optimistic views with regards to FY19 results which validated new business model announced with strategic refresh program in the month of August 2018. It was further added that the initiatives have been showing early signs of the success in repositioning the business for growth. The company is well-positioned to capitalise on changing financial services landscape, offering advisers the tools as well as services that they require in order to drive their businesses forward. The company has welcomed additional advice businesses to the network, and it continues to witness that financial advisers are proactively looking for the quality business services partner. The company has cash and cash equivalents of $7.9 million as June 30, 2019, as compared to FY18 cash balance of $9.5 million. It was added that cash provided by continuing operations stood at $3.2 million from which $4.5 million was paid out in the claims, $1.3 million for the acquisition of software. However, $1.2 million was received for Neos divestment and loan repayment.

The company added that the industry dislocation gives an opportunity to grow the market share and CAF is deploying towards technology and data in order to enable greater scale, better insights and the superior service. Additionally, there are expectations that respectable capabilities to generate revenues can act as a primary tailwind.

.png)

Financial Performance (Source: Company Reports)

Top 10 Shareholders: The following table provides a broader overview of the top 10 shareholders in Centrepoint Alliance Limited:

.png)

Top 10 Shareholders (Source: Thomson Reuters)

YoY Improvement in Key Margins: Centrepoint Alliance Limited has witnessed improvement in its key margins in FY19 on a YoY basis and, thus, it can be said that the company is possessing a decent fundamental base. In FY19, the company’s EBITDA and operating margin stood at 2% and 1.3%, respectively. The company’s current ratio stood at 1.49x in FY19, which is higher than the FY18 figure of 1.11x and, thus, it can be said that liquidity levels are decent, and it can meet its short-term obligations in an effective manner. Additionally, the company can make deployments towards strategic business activities which could help it in achieving long-term growth.

.png)

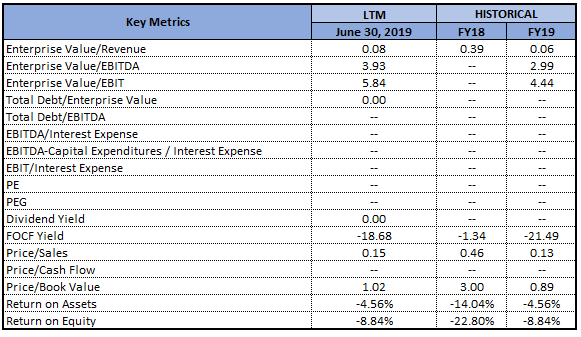

Key Metrics (Source: Thomson Reuters)

Progress on the Implementation of New Pricing: The Board of Directors has recently advised that the key milestone has been reached with respect to its strategic refresh program. The company has announced that 200 of its 226 licenced adviser firms contracted to transition to CAF’s new transparent pricing arrangements. The company launched a new licensee service offering in the month of March 2019 and transition has been completed successfully. It was further stated that the completion of transition was timely because fee-based revenue is required in order to offset accelerated decline in the Centrepoint’s rebate revenue. The new offer has been proving attractive to the new advisers, as well as existing network, resulting in a record number of new advisers joining CAF in June quarter of FY19.

Understanding Group’s Balance Sheet Position: The company has managed to maintain the robust balance sheet through transition, and there has been a significant reduction in the legacy claims resulting in the reduced provision. The following picture provides an idea of the company’s balance sheet:

.png)

Balance Sheet (Source: Company Reports)

The loans receivable includes $5.8 million from Neos, of which $2.5 million has been scheduled to be repaid by June 2020.

Overview of 1H FY19 Results: Centrepoint Alliance Limited has earlier announced the financial results for the half year ended December 31, 2018 (or 1H FY19) in which its net profit before tax amounted to $1.7 million. It was stated that even though there were difficult trading conditions, the gross profit has remained flat on the prior periods. Over the half, the company has witnessed a net increase in the licenced as well as self-licenced advisers. The following picture provides an idea of the funds under management and administration:

.png)

Funds Under Management And Administration (Source: Company Reports)

The company’s net profit after tax for 1H FY19 amounted to $0.1 million as compared to 1H FY18 loss of $1.3 million. The improvement from the prior comparative period implies a 0.3% rise in the revenue to $16.1 million. The operating expenses witnessed a fall of 20%, and the figure stood at $14.4 million as the company witnessed substantially lower legacy client claims. In 1H FY19 results presentation, the company stated that the financial advice market offers substantial opportunities for the quality scale providers. The structural demand for advice happens to be strong in the Australian community. The company is uniquely positioned as the quality licence operator and service provider to self-licenced firms. CAF’s FUMA rose 1% (vs 1H18) and fell 4% (vs 2H18), impacted by the market movements and outflows. However, quality and scale validate that CAF would be increasingly attractive in disrupted and increasingly scrutinised market.

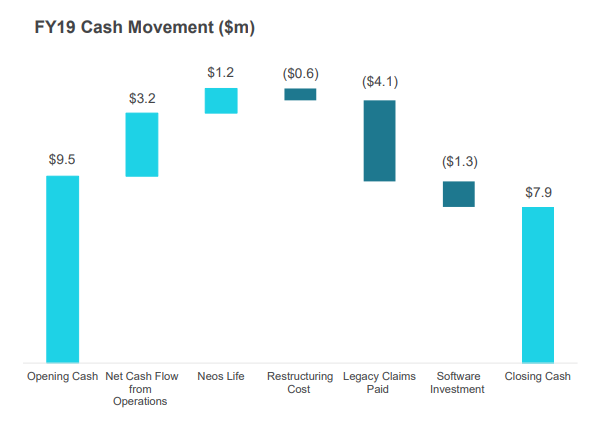

Software Investment Might Support CAF: At the end of FY19, the company had a closing cash position of $7.9 million, and the following image provides a broader overview of the cash movement:

FY19 Cash Movement ($ million) (Source: Company Reports)

The company’s net cash flow from operations stood at $3.2 million, and there was a software investment amounting to $1.3 million in order to improve the scale and service experience for advisers.

What To Expect From CAF Moving Forward: As mentioned in the half-yearly report, the key drivers of Licensee and Advice Services revolve around a number of the advice firms, fee income, operating costs, funds under distribution agreements, lending volumes as well as lending margins. For Funds Management and Administration, the key drivers include funds under administration, funds under management, margins as well as operating costs.

In the annual financial report, the company stated that it is well-positioned to take advantage of disruption in the wealth management industry. The transformation has been progressing well, and it is focussed towards assessing the partnerships, acquisition opportunities and enhancing the shareholder value. The areas of focus for FY20 of the company includes launching fee-based offer for the self-licensed advisers and drive growth in the licensed network. Additionally, the focus also revolves around further deploying towards technology and data in order to enable the greater scale and superior service.

In 1H FY19 results presentation, the company stated that the strategy would ensure that CAF is the lead provider of the advice and business services to the financial adviser community. It was also mentioned that the financial advisers are seeking a quality partner in order to help manage their businesses efficiently and confidently in the changing landscape.

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: The stock of CAF has delivered a return of 27.78% in the span of previous three months while, in the time frame of past six months, the stock has gained 4.55%. The company’s key personnel stated that 86% of the adviser firms within Centrepoint authorised representative network transitioned to new recurring pricing model as revenue from rebates reduced sooner than was expected. Between the time span of FY13- FY19, the company’s total revenue has witnessed a CAGR growth of 15.08%, which can be considered at decent levels and might attract the attention of the market participants. There are expectations that decent capabilities to generate revenues might help the company in achieving growth over the long-term. Currently, the stock is trading slightly below the average of 52 weeks' high and low levels of $0.175 and $0.081, respectively. Hence, considering the above-stated facts and current trading levels, we give a “Speculative Buy” recommendation on the stock at the current market price of $0.120 per share (up 4.348% on 27 September 2019).

CAF Daily Technical Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...