Kalkine has a fully transformed New Avatar.

Company Overview: Centrepoint Alliance Limited is a financial services company. The Company is a provider of a range of financial advice and licensee support services (including licensing, technology, business support, training, compliance and professional standards) to financial advisers and accountants across Australia. The Company operates through two segments: Licensee and Advice Services, and Funds Management and Administration. Licensee and Advice Services segment provides Australian Financial Services License related services to financial advisers and their clients and mortgage broking services. It’s Funds Management and Administration segment provides investor directed portfolio services and investment management services to financial advisers, accountants and their clients. It also provides lending mortgage aggregation services to mortgage brokers. Its subsidiaries include Centrepoint Alliance Lending Pty Ltd, Associated Advisory Practices Pty Ltd and Professional Investment Services Pty Ltd.

.png)

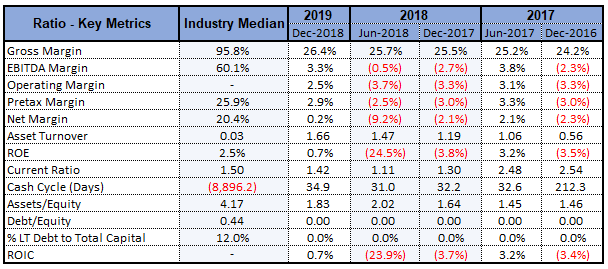

CAF Details, *ROE figure for 1HFY19

Turnaround Performance in 1HFY19: Centrepoint Alliance Limited (ASX: CAF) is an ASX-listed company whose principal activities revolve around Licensee and Advice Services as well as Funds Management and Administration. As on July 19, 2019, the market capitalisation of Centrepoint Alliance Limited stood at ~$17.87 million. The company released its results for 1H FY19 (or for the six months ended December 2018) in which it posted a net profit before tax of $1.7 million as compared to $1.9 million loss in the 1H FY18. Also, the company’s EBITDA in 1H FY19 stood at $2.2 million as compared to the loss of $1.4 million in 1H FY18. The company stated that, even though there were difficult trading conditions, the company’s gross profit remained flat on the prior periods. The company’s net profit after tax for 1H FY19 amounted to $0.1 million as compared to the loss of $1.3 million in 1H FY18. The company added that the improvement from the prior comparative period implies a 0.3% rise in revenue to $16.1 million. Also, the company’s operating expenses witnessed a fall of 20% to $14.4 million as the company witnessed substantially lower legacy client claims.

With the help of the renewed executive team as well as deployment towards robust operational capability, the business maintained stable revenue, attracted new advisers, and it is also absorbing the costs of executing Strategic Refresh program through re-deploying the resources and adding new digital and data capabilities financed with the help of productivity gains. Coming to the management’s viewpoints, CEO stated that there happens to be an unequivocal demand for the quality financial advice, and with structural disruption of the industry that is occurring CAF is uniquely placed to capitalise on unfolding changes. As at December 31, 2018, the company is having a closing cash position of $7.4 million, which can be considered at the decent levels. The company stated that it is focused on growth and relationships with around 469 financial planning firms. The business happens to be well progressed on the strategy of putting in place a new offer which would be positioning it as a leader in advice and business services operating in post Royal Commission environment.

.png)

1H FY 2019 Financial Results (Source: Company Reports)

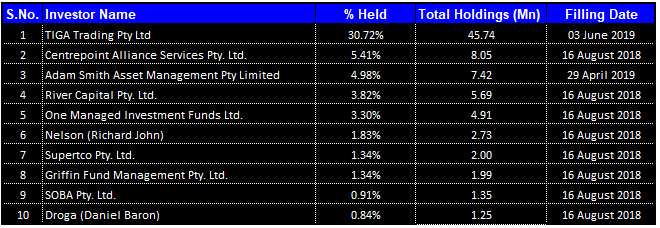

Top 10 Shareholders: The following table provides a broad overview of the top 10 shareholders in Centrepoint Alliance Limited:

Top 10 Shareholders (Source: Thomson Reuters)

Improvement in Key Margins Strengthens Confidence in Future Operations: The company witnessed an improvement on a YoY basis, which reflects that the company has respectable financials. The company’s net margin stood at 0.2% in 1H FY19, implying an improvement of 2.3% on a YoY basis, which indicates that the company’s capabilities to convert its top line into bottom line have improved. Additionally, its EBITDA margin stood at 3.3%, which reflects a rise of 6% on a YoY basis. Coming to the liquidity levels, the current ratio stood at 1.42x in 1H FY 2019, which is an improvement of 9.3% on a YoY basis. This indicates that the company is in a decent position to meet its short-term obligations. And, considering the decent liquidity levels, it looks like that the company in a position to make deployments in key strategic objectives and in areas which can help it in achieving long-term growth.

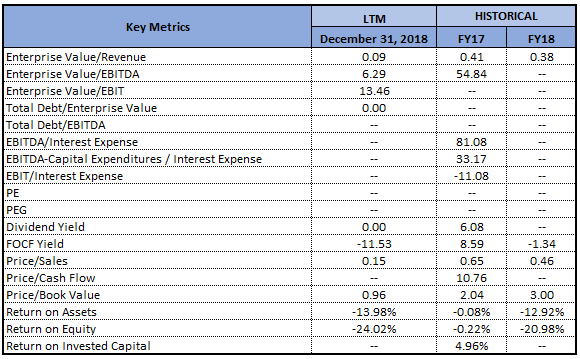

Key Metrics (Source: Thomson Reuters)

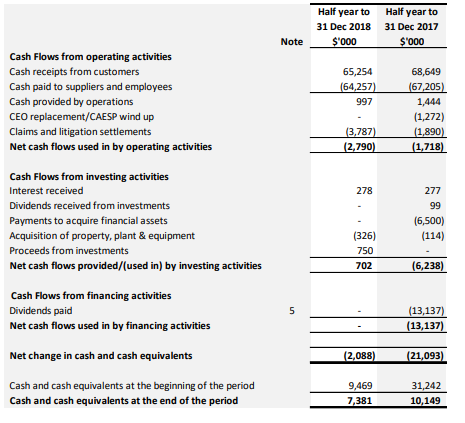

Understanding CAF’s Cash Flow Position: Centrepoint Alliance Limited is having a closing cash position of $7.4 million at the end of 1H FY19, and the following picture provides a brief information about the same:

Condensed Consolidated Statement of Cash Flows (Source: Company Reports)

The company’s net cash flows used in by operating activities stood at $2.790 million in the half-year to December 2018 and, during the same period, the company’s cash receipts from customers amounted to $65.25 million. In FY14, the company’s cash used in operating activities stood at $1.28 million while in FY18 it was $0.42 million.

Announcement Related to Progress on Implementation of New Pricing: The Board of Directors of CAF advised that key milestone has been reached with respect to its Strategic Refresh program. The company made an announcement that 200 of its 226 licenced adviser firms have contracted to transition to the company’s new transparent pricing arrangements. CAF launched its new licensee service offering in the month of March 2019 and transition has been wrapped up. Additionally, the company stated that completion of transition is timely, because fee-based revenue is needed in order to offset an accelerated decline in the company’s rebate revenue. The company's key personnel stated that, over the second half of FY19, they witnessed a significant acceleration in the reduction of grandfathered rebates, which further validates the refresh strategy to move to a contemporary as well as transparent offering. The new offer is proving to be attractive to the new advisers, as well as the existing network, resulting in a record number of new advisers joining Centrepoint in the quarter ended June 2019. It was stated that the company's new offer is also resonating with the external market and proving its competitiveness.

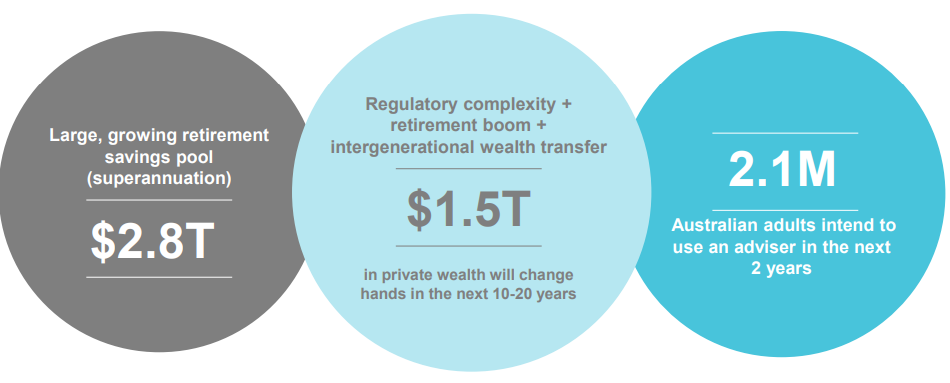

Key Takeaways From 1H FY19 Presentation: Centrepoint Alliance Limited stated that the underlying demand for financial advice happens to be attractive and the following picture could help in providing a broad overview regarding the same:

Underlying Demand (Source: Company Reports)

Additionally, the company added that quality as well as scale validates that the company would increasingly be attractive in the disrupted and increasingly scrutinised market. As stated in the presentation, the financial advice market offers significant opportunities for the quality scale providers and the structural demand for advice happens to be strong in the Australian community. It is important for the market players to know that CAF is uniquely positioned as a quality licence operator and service provider to the self-licenced firms.

What To Expect From CAF Moving Forward: As mentioned in 1H FY19 results presentation, in 2H FY19, Centrepoint Alliance Limited might introduce new governance and standards framework and harness the internal data for the efficiency gains. The key drivers of Licensee and Advice Services business include the number of advice firms, operating costs, fee income, funds under distribution agreements, lending volumes as well as lending margins. With respect to the same business, the company stated that it continues to focus towards being a client-centric, which involves improving the quality of advice and wealth solutions given to Australians.

Coming to the Funds Management and Administration business, the company stated that key drivers include funds under administration, funds under management, margins as well as operating costs.Additionally, the company happens to be debt-free with $7.4 million of cash as well as $7.9 million in the interest-bearing receivables. The debt-free status of CAF might prove to be beneficial moving forward, and it can be said that the company has a stable balance sheet. In 1H FY 2019 presentation, the company stated that industry as well as CAF are going through the transition that would see vastly re-shaped industry in the span of 3-5 years, with significant opportunities for the quality scale providers.

Key Valuation Metrics (Source: Thomson Reuters)

Stock Recommendation: In the span of FY16- FY18, Centrepoint Alliance Limited witnessed a CAGR growth of 3.19% which can be considered at respectable levels and it can be said that the company is possessing decent capabilities to generate revenues. The Chairman of the company stated that CAF has undergone significant change since the arrival of Angus. Considering that the new look of the executive team is in place, the company has made solid progress in 1H FY19 when it comes to delivering the Strategic Refresh, which happens to be consistent with recent recommendations from Royal Commission.

The company’s stock has delivered the return of -68.42% in the span of previous one year, while in the time frame of past six months, the stock’s return was 22.45%, which reflects that the stock has been improving its performance, which might help the company in gaining traction among market participants. Currently, the stock is trading slightly below the average of 52 week high and low prices of around $0.230, indicating a decent opportunity for accumulation. Hence, in the view of aforesaid parameters coupled with decent outlook and current trading level, we give a “Speculative Buy” recommendation on the stock at the current market price of A$0.135 per share (up 12.5% on 19 July 2019).

CAF Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...