Kalkine has a fully transformed New Avatar.

Company Overview: Carter’s, Inc. is a marketer of apparel exclusively for babies and young children. The Company owns two brand names in the children's apparel industry, Carter's and OshKosh B'gosh (OshKosh). These brands are available in department stores, national chains, and specialty retailers domestically and internationally. The Company offers its products through over 1,000 Company-operated stores in the United States, Canada, and Mexico, and via its online sites www.carters.com, www.oshkosh.com, and www.cartersoshkosh.ca. The Company’s Child of Mine brand is available at Walmart, its Just One You brand is available at Target, and its Simple Joys brand is available on Amazon. The Company also owns Skip Hop, a global lifestyle brand for families with young children.

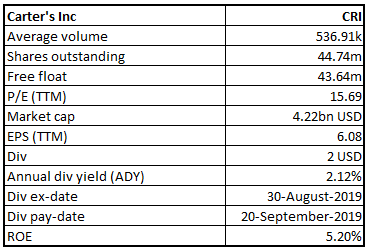

CRI Details

Prudent Marketing Strategy to Drive Overall Growth: Carter’s, Inc. (NASDAQ: CRI) is the largest branded marketer in North America of apparel exclusively for babies and young children. The company owns the largest market share of $21 billion in the U.S. and $1.5 billion in Canada for baby and young children’s apparel market. The most trusted brands of the company include Carter’s and OshKosh B’gosh with a history of more than 100 years. Brands such as Child of Mine, Just One You and Simple Joys are sold at Walmart, Target, and Amazon, respectively. Another brand Skip Hop is a fast-growing and innovative leader in the children’s durables product category. The company is the largest branded marketer of young children’s apparel in North America. The company’s top-line and bottom-line have grown, on average, by 9% and 14% in the last ten years. Taking cues from the company’s growth objectives, CRI’s multi-channel business model aids an average sales growth of approximately 3% per annum over the next five years. With the completion of this objective, top-line of the company is expected to touch the level of ~$4 billion by 2023.

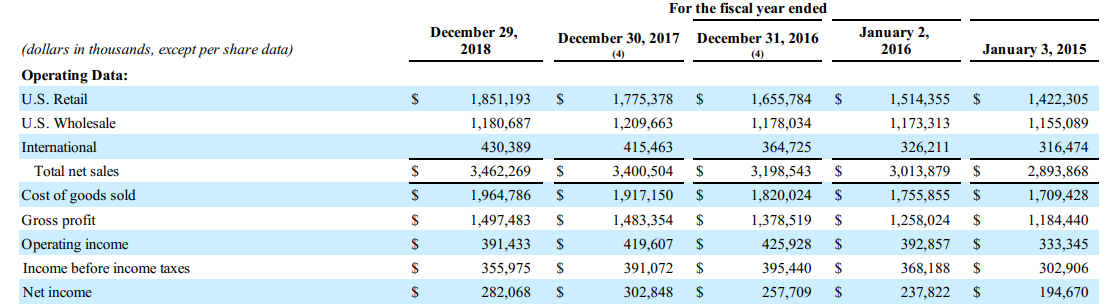

The company operates with a multi-channel global business model, that includes retail store, eCommerce, and wholesale sales channels, enabling it to reach a broad range of customers and generated net sales and net income of $3.46 billion and $282.1 million, respectively, in FY18, driven by sales growth in U.S. Retail and International segments, partially offset by a decline in U.S. Wholesale segment. In FY18 (for the period ended on December 2018), total revenue stood at $3,462.26 million, posting a rise of 1.82% as compared to $3,400.50 million during FY17. Net profit for the company was recorded at $282.068 million, declined 6.86% on y-o-y. Looking at the performance over FY14-FY18, CRI delivered a CAGR growth of ~4.59% in revenue, while net profit posted a CAGR growth of 9.71% during the same period.

Going forward, the Company will extend the reach of the brands by improving the convenience of shopping for the products, through omni-channel experience, followed by the expansion of international operations. The Company will be focusing on improving profitability by strengthening logistics and direct-sourcing capabilities, as well as inventory management disciplines.

Operating Performance During FY14-FY18 (Source: Company Reports)

Global Expansion to Support Top-line Growth: The company has footprints in 85 countries through eCommerce capabilities and relationships with retailers throughout the world. In the last five years, the company has invested in consumer-facing and revenue-driving capabilities in the U.S. To enable better collaboration between the U.S. operations and Canada & Mexico, the company, recently restructured international organization. With leveraging such investments and efforts to strengthen the global structure, the company intends to support the growth in the long run.

Segment Wise Performance: The company evaluates its performance with three reporting segments - U.S. Retail, U.S. Wholesale, and International. U.S. Retail segment consists of revenue primarily from sales of products in the United States through retail and online stores. Similarly, U.S. Wholesale segment consists of revenue primarily from sales in the United States of products to the wholesale partners. Finally, International segment consists of revenue primarily from sales of products outside the United States, largely through the company’s retail stores in Canada and Mexico, eCommerce sites in Canada and China, and sales to international wholesale accounts and licensees.

2QFY19 Key Highlights:

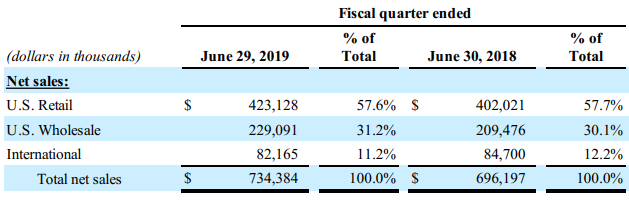

Decent Revenue Growth in Q2FY19: The Company derived 57.6% of the total revenue from U.S. Retail at $423.12 million as compared to $402.02 million in the prior corresponding period, driven by 7.7% growth in the number of units shipped and a 1.6% addition in the average price per unit. The U.S. Wholesale registered a revenue of $229.09 million as compared to $209.476 million in Q2FY18, depicting a 31.2% of the total revenue. The Company reported a 11.2% contribution from international segment at $82.16 million during the quarter. Compared to the second quarter of fiscal 2018, Canadian comparable retail sales increased by 0.9% in the second quarter of fiscal 2019.

Q2FY19 Revenue Bifurcation as Per Operating Segments (Source: Company Reports)

Gross Margin and Gross Profit: During Q2FY19, the business reported a reduction in gross margin from 44.5% in Q2FY18 to 44%. Gross profit of the business came in at $323.0 million in the second quarter of FY19, registering a growth of ~4.2% on pcp. The Management highlighted that a decrease in gross margin was mainly due to the changes in customer and channel mix, increased shipping expenses across the eCommerce segment, followed by higher product costs, which was partially offset by lower provisions for inventory.

Selling, General and Administrative Expense: During the quarter, the Company reported selling general, and administrative (SG&A) at $268.2 million, up 1.8% from the prior corresponding period. In percentage of net sales, SG&A expenses declined from 37.8% in Q2FY18 to 36.5% in Q2FY19. The Management highlighted that the Company witnessed a $3.6 million increase in U.S. retail expenses, $2.0 million increase in distribution costs, followed by $1.5 million increase in performance-based compensation and $1.8 million increase due to the receipt of insurance recoveries that occurred in the second quarter of fiscal 2018. While due to the China business model, the Company witnessed $2.8 million decrease in expenses and $2.2 million lower in marketing expenses.

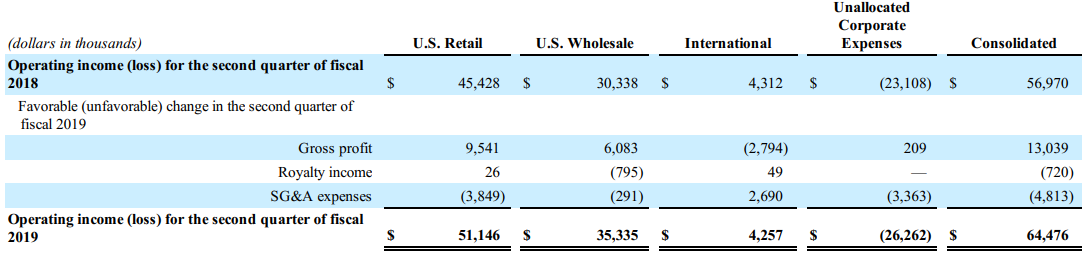

Operating Income and Operating Margin: The Company reported an operating income at $64.5 million, as compared to $57 million in the second quarter of FY18. Consolidated operating margin increased from 8.2% in the second quarter of FY18 to 8.8% in the second quarter of FY19. U.S. Retail reported operating income at $51.14 million while U.S. Wholesale came in at $35.33 million, whereas the business reported an operating income of $42.57 million from International segment. The Company reported unallocated corporate expense of $26.26 million during the second quarter of FY19. Wholesale segment's operating margin increased 90 bps from 14.5% during Q2FY18 to 15.4% in Q2FY19, primarily due to the lower provisions for inventory, partially offset by changes in customer mix and due to the transition of a licensee to a wholesale model, which was partially offset by increased licensee sales.

Interest Expense: The interest expense of CRI during Q2FY19 came in at $9.1 million as compared to $7.9 million in Q2FY18. Weighted-average borrowings of the Company during the second quarter of fiscal 2019 stood at ~$608.8 million with an effective interest rate of 5.78% as compared to weighted-average borrowings for the second quarter of fiscal 2018 of $616.9 million with an effective interest rate of 5.04%. The decrease in weighted-average borrowings during the second quarter of fiscal 2019 was attributable to lower borrowings under the secured revolving credit facility.

FY19 Operating Income (Source: Company Reports)

.png)

FY19 Operating Margin (Source: Company Reports)

Net Income: CRI’s net income on a consolidated basis for the second quarter of FY19 came in at $43.9 million as compared to $37.3 million during the second quarter of FY18.

A Quick Look at Six-months Results: During the first six months, U.S. Retail segment reported net sales at $800.2 million, increased approximately 1.8% from $785.8 million on pcp. The U.S. Wholesale segment reported sales of $504.5 million as compared to $490.3 million in the first half of FY18. This increase reflected a 1.5% increase in the number of units shipped and a 1.3% increase in the average price per unit. Compared to the first two quarters of fiscal 2018, the Company’s Canadian comparable retail sales decreased 2.6% in the first two quarters of fiscal 2019. The Company’s consolidated gross margin witnessed a decline from 44.2% in the first six-months of FY18 to 43.3% in H1FY19. The consolidated gross profit decreased $3.6 million, or 0.6%, to $638.9 million during the first half of FY19 from $642.4 million on pcp. The consolidated net income for the H1FY19, witnessed 1.7% decrease at $78.4 million compared to $79.7 in H1FY18.

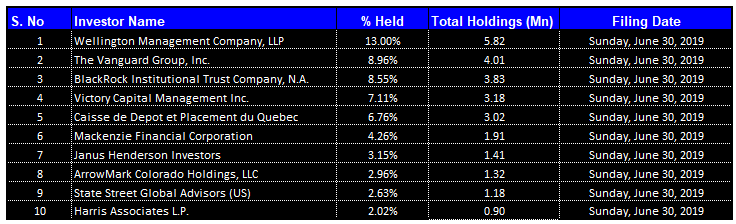

Top 10 Shareholders: The top 10 shareholders have been highlighted in the table, which together form around 59.4% of the total shareholding. Wellington Management Company, LLP and The Vanguard Group, Inc. hold the maximum interests in the company at 13% and 8.96%, respectively.

Top 10 Shareholders (Source: Thomson Reuters)

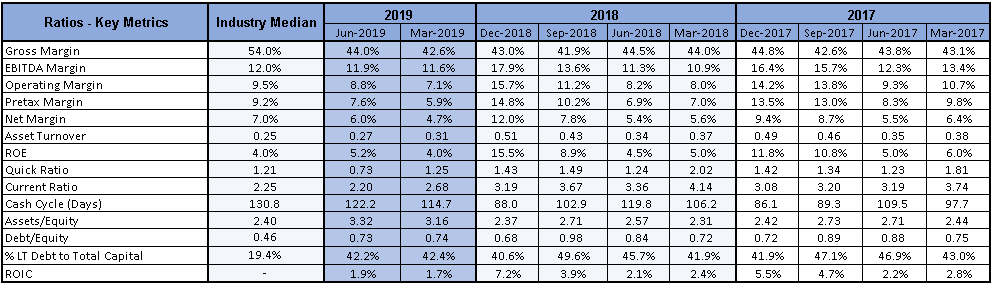

Key Metrics: The Company posted decent margins in the second quarter of FY2019. Gross margin for Q2FY19 stood at 44%, higher than Q1FY19. EBITDA and net margin for Q2FY19 came in at 11.9% and 6%, higher than Q2FY18 of 11.3% and 5.4%, respectively. Return on Equity (ROE) stood at 5.2% in Q2FY19, higher than the industry median of 4%.

Key Metrics (Source: Thomson Reuters)

Outlook: For Q3 FY19, the Management guided that U.S. retail segment is expected to grow by lower single-digit and expects lower growth in International and U.S. Wholesale segment. The Company is expecting Adjusted diluted EPS growth of ~3% to 4%. The Company is also expecting a higher interest expense due to refinancing of senior note.

For FY19 guidance, the Company is expecting ~1% to ~2% top-line growth and adjusted diluted EPS growth of ~4% to 6%. The company expects operating cash flow to remain within the range of ~$375 million to $400 million. The management also highlighted that FY20 CAPEX would be around ~$80 million.

Valuation Methodology- EV/EBITDA Multiple Approach:

.jpg)

EV/EBITDA Based Valuation (Source: Thomson Reuters)

Note: All forecasted figures and peers have been taken from Thomson Reuters, *NTM-Next Twelve Months

Stock Recommendation: At the current market price of $95.38, the stock is trading at a price to earnings multiple of 15.62x with a market capitalization of ~$4.22 billion. The Company provides the best value and experience across young children's apparel and accessories and is currently focusing on increasing its presence to more than 1,000 doors at the end of FY19. During the year, the Company has introduced a private label credit card, which is expected to strengthen the overall relationship with customers, drive incremental sales and margin, and reduce credit card fees. The Company is finding new avenues through the launch of OshKosh with the target in over 600 doors and online presence along with the expansion in the toddler clothing segment. Considering the aforesaid facts, we have valued the stock, using a relative valuation method, i.e., EV/EBITDA multiple, and arrived at a target price of lower double-digit growth (in % term). Hence, we recommend a “Buy” rating on the stock at the current market price of $95.38, up 0.43% on 16 October 2019.

CRI Daily Technical Price Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Please wait processing your request...

Please wait processing your request...