Company Overview - carsales.com Limited is engaged in online classified and display advertising business and provides a range of software, data and other services to customers in the automotive industry. The Company operates in two business segments: Online Advertising Services, which offers classified advertising and display advertising services. Classified advertising encompasses both private sellers and dealer customers. Display advertising involves corporate customers, such as automotive manufacturers/importers, finance and insurance companies placing advertisements on its Website and Data and Research Services, where the Company’s divisions of Redbook, LiveMarket, DataMotive and DataMotive Business Intelligence provide various solutions to a range of customers, including manufacturers/importers, dealers, industries, finance and insurance companies offering products including software, analysis, research and reporting valuation services, website development and hosting and photography services.

Analysis - Carsales (CAR) reported 10% growth in consolidated net profit after tax to $48.6m for the 6 months to 31 December 2014 as opposed to $44.0m in 2013. There was a 15% rise in EBITDA for the half-year ended 31 December 2014, which was of the order of $72.9m as opposed to $63.5m of 2013; while the EBITDA margins were at 48.3% quite lower than 56.5% of 2013 given the lower margins witnessed at Stratton. 34% growth in revenue from ordinary activities to $150.9m as opposed to only $112.3m in 2013 for said period was another highlight. Particularly, organic growth resulted in 8% rise in online advertising revenue to $105.9m and 20% rise in data and research revenue to $15.2m. The international revenue also surged 8% to $1.4m. The Company reported finance and related services revenue of $28.4m based on the Stratton acquisition in 2014.

Financial Results (Source – Company Reports)

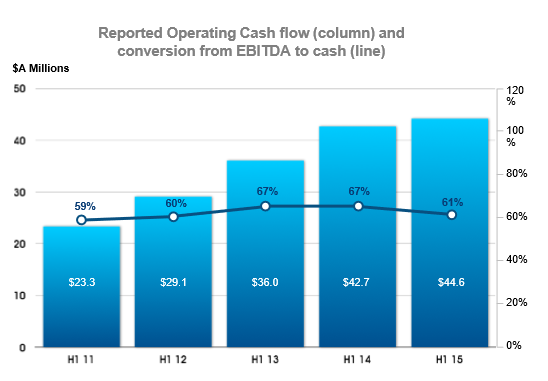

There has been an increase of about $52m in net debt from 30 June 2014 to reported net debt of about $201m as at 31 December 2014 in view of the investments made by the Company. The cash conversion of earnings has been robust with operating cash flow/rolling 12 month EBITDA at 61%. Cash payment by Stratton of pre-acquisition tax liabilities indicates the decrease from 1H 14.

Domestic Revenue Performance_Segment-wise (Source – Company Reports)

The Company declared a dividend of 16.2 cents fully franked to be paid in April 2015. This is 10% up on previous corresponding period (pcp). During the 12 months ending 31 December 2014, the Company paid dividends totaling $0.34 per share and there has been an increase in its dividend during each of the past 5 fiscal years. As per CAR, the Company aims to maintain its dividend reinvestment plan for the 2015 interim dividend while giving away an opportunity to acquire ordinary shares for the shareholders. Further, CAR reported earnings per share of 19.6 cents per share reflecting an increase of 1.1 cents (6%) on the prior half year. Steps have been also taken towards refinancing of existing debt by entering into a $325m 5-year syndicated debt facility. This will enable CAR to support its business growth.

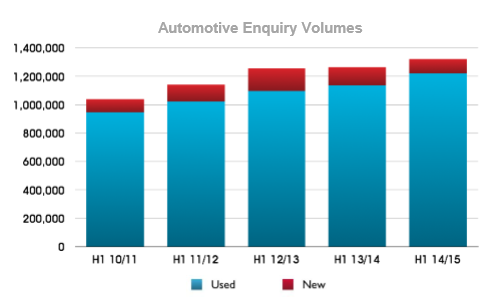

Automotive Enquiry Volumes (Source – Company Reports)

The 34% surge in gross revenues from continuing operations was steered by 8% rise in dealer revenue and 16% rise in private revenue under domestic performance. The rise in dealer revenue is attributed to acquisition of new customer subscriptions, rise in subscription price and growth in premium advertising products including but not limited to GTS and Top Deals; while tyresales, price rises and volume growth in niche verticals drove private revenue growth. There was a 7% surge in automotive dealer used car enquiry growth year on year. Revenue for dealer and data services illustrated continuous growth with 20% rise on pcp. 3% growth on pcp was noted for mediamotive performance.

New Mobile Site (Source – Company Reports)

We note lower total new vehicle enquiry volumes on pcp given stock reductions based on advertising policy changes brought-in by manufacturers. Growth in generic new car enquiry still continued. The automotive inventory count has been lower than pcp at around 202,000 cars as at 31 December 2014. Particularly, slip in dealer used vehicle inventory by ~4% on pcp and lower new car inventory of 35,000 cars along with 12% dip in private inventory to around 73,000 cars were the key points. Private seller sales volumes in December and January, respectively, rose 13% and 21% on pcp.

CAR also reported that investments in Webmotors SA (Brazil) and SK ENCARSALES (South Korea) led to rise in underlying revenue by 23.7% and 38%, respectively, indicating quite encouraging results. For SK ENCARSALES, EBITDA margins rose from 51% in June to 56.1% and strong collaboration resulted in a range of new initiatives. RedBook illustrated strong performances across Asian countries while New Zealand pcp performance was maintained. Webmotors witnessed strong double digit growth in dealer, private and display. Growth in Brazil is supported with combined (MeuCarango, CompreAuto and WebMotors) inventory getting doubled the closest competitor. However, the reported earnings for Webmotors were affected by one off amortisation charge (Meurcarango) and write off of fixtures and fittings along with investment in further headcount and marketing. The closure of acquisition of Vmotors by the WebMotors in December, is expected to better the offerings to dealers, although without having any significant impact on business.

International Portfolio (Source – Company Reports)

A lot is expected from the new products and initiatives for the remaining 2015 given the release and performance by the ones in 1H. Based on the revenue growth, 7% increase in consolidated net profit after tax and non-controlling interests of $46.7m was noted compared to that of 2013. As per CAR, the pcp interest expense growth and iCar negative earnings affected the NPAT (post non-controlling interests) growth of 7%. 64% rise in total operating expenses of $84.7m as opposed to $51.6m of 2013 emanated from the acquisition of Stratton along with amplified costs related to marketing efforts and personnel.

The Company expects to have strong revenue and EBITDA throughout 2H FY15 with modest rise in NPAT, in consideration of stability of its on-going performance and market conditions. Development of opportunities in Brazil and South Korea seem to be progressing well for future earnings growth.

Cash Flow (Source – Company Reports)

Overall, what is seen is rise in revenue despite the softness in new car listings and re-launch of Carsguide. Dealer used enquiries have been up indicating a solid growth for the segment. The total new vehicle enquiry volumes have been down but the Brand New Car Available (BNCA) product contributes to growth from a smaller base. Thus, growth is expected to continue in 2H as well. Display advertising has moved up only 3% on growth ladder given cyclical advertisement market and other challenges, thus appearing to be a little drag when other segments witnessed strong growth. Particularly, effect of some manufacturers withdrawing new car listings played a little havoc. Only a meagre growth is expected in display advertising in 2H15 which may improve gradually with increase in audience base and auto display advertising undergoing structural transformation from print to online. The plan to roll-out a new Autogate product to dealers at no extra cost may prove beneficial. Thus, great play still exists given CAR’s market-leading position in online automotive classifieds based on audience and inventory. The outlook with regards to private yields given advertisement price increases at CAR’s disposal look appealing. There also exists a positive sentiment around the revenue growth in dealer and data services. Benefits also may emanate from domestic growth opportunities in products like Live Market and opportunities in international markets.

Carsales Daily Chart (Source - Thomson Reuters)

Aspects such as loss of market share to new entrants or increase of market share by competitors, reduction in automotive website inventory, reduction in traffic to CAR’s websites, and change in consumers’ likings or new technology can affect the projected performance. It is to be understood that Stratton and tyresales.com.au operate in competitive and mature industries than CAR’s core business but do have an impact on group earnings. Effects from regulatory changes such as removal of $12k special tariff on importation of used cars, abolition of the Luxury Car Tax, and establishment of the Free-Trade-Agreement with Japan and South Korea need to be seen. Market believes that a neutral effect on car industry structure and a positive effect on CAR may be seen with the increase in cars being sold under the circumstances. Of course, the real scenario is difficult to be clearly construed.

Nonetheless, we also note that CAR has come out with an indication about its market position wherein it appears to dominate over competitors in Carsguide and Gumtree. For instance, CAR stated that 86% of its audience doesn’t visit the site of its nearest competitor and cumulatively it captures more than 25x the total session minutes than its nearest competitor. As part of CAR’s other strategies and to boost the Australian automotive financing market, CAR together with Stratton will invest about $10 million in Sydney-based RateSetter Australia while having a combined 20% equity stake.

We thus put a BUY recommendation for this stock at the current price of $9.70.

.png)

.png)

.png)

Please wait processing your request...

Please wait processing your request...