Company Overview: Cann Group Limited is an Australia-based company, which is engaged in the cultivation of cannabis for human medicinal and research purposes. The Company has facilities to cultivate medicinal cannabis. It also focuses on manufacturing medicinal cannabis products. It focuses on developing and supplying cannabis, cannabis resin and medicinal cannabis products into the Australian market. It also focuses on supplying to overseas markets. The Company has a cannabis research license and cannabis cultivation license. The cannabis cultivation license allows the Company to produce Australian grown material that can be prescribed for patient use. It has research and development, and cultivation facilities in Australia. It focuses on plant genetics; breeding; cultivation; extraction; analysis and production techniques to facilitate the supply of medicinal cannabis for a range of diseases and medical conditions.

.png)

CAN Details

Significant Developments Made in March 2019 Quarter: Cann Group (ASX: CAN) is building a world-class business which is focused towards breeding, cultivating and manufacturing the medicinal cannabis for sale and use within Australia. As on April 30, 2019, the market capitalisation of Cann Group stood at ~$332.5 million. It recently released activities report for the quarter ended March 2019 wherein it disclosed that the company entered into non-binding Heads of Agreement to purchase a site which is situated within Mildura region, in North West Victoria. On this site, the company has plans to construct a state-of-the-art greenhouse for the large-scale cultivation and production of medicinal cannabis so that domestic and export markets can be serviced. Cann Group made an announcement that a five-year agreement with Aurora Cannabis Inc had been entered for offtake of medicinal cannabis produced by Cann at existing and planned expansion facilities until 2024. There is significant opportunity in Australia and for exports which can act as a tailwind for the company. Cann Group has been maintaining a focus towards the commercial strategy.

.png)

Net Cash used in Operating Activities (Source: Company Reports)

During March 2019 quarter, CAN’s net cash used in operating activities amounted to $2.77 million and it incurred staff costs of $1.33 million. Cann Group wrapped up $250,000 investment in independent medicinal cannabis clinic group named Emerald Clinics. This investment was part of $2.5 million of capital raising wrapped up by Emerald in order to help national roll-out program of its clinics. There are expectations that Emerald would be continuing expanding the network to other major cities and regional centres throughout 2019 in order to ensure that Australians which are looking for a regulated supply of medicinal cannabis have access to the highly-informed healthcare practitioners.

The primary growth drivers for the company includes offtake agreement with Aurora Cannabis, manufacturing partnership, investment in Pure Cann and strong liquidity position. Additionally, the patient access pathways and global opportunity are also the key factors which might help the company to grow further.

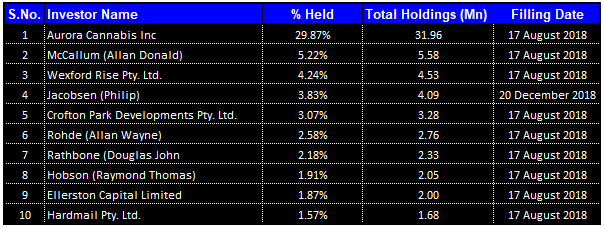

Top 10 Shareholders: The top shareholders account for 56.33% of the total shareholding pattern with Aurora Cannabis making it to the top of the list as shown in the table below:

Top 10 Shareholders (Source: Thomson Reuters)

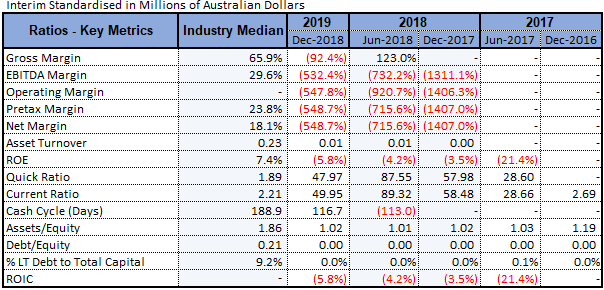

Improvement in Margins Builds Confidence in Fundamentals: The key margins of Cann Group had witnessed significant improvement in 1H FY 2019 on the YoY basis which reflects that the company is possessing decent position to achieve respectable growth levels moving forward. Moreover, the company enjoys a virtual debt-free status with a current ratio of 49.95x as on 31 December 2018. This current ratio is significantly higher than the industry median of 2.21x demonstrating that the company has a sound liquidity position in order to address its short-term obligations which might arise during the course of business. We expect that an improvement in the margins can attract the attention of market players and sound liquidity position can support its investment activities and could improve its standing to cater the long-term growth.

Key Ratios (Source: Thomson Reuters)

Strategic Investment In Pure Cann New Zealand Limited: – Cann Group wrapped up a strategic investment in Pure Cann NZ Limited. There are expectations that Pure Cann would be able to establish a leading position in the anticipation of regulatory changes that would be permitting cultivation and broader supply of the medicinal cannabis in New Zealand. The New Zealand Government is expected to bring new regulations, licensing requirements and quality standards governing medicinal cannabis usage by the calendar year end.

CAN’s strategic investment amounting to NZ$6 million in Pure Cann secured a 20% ownership stake which is to be made over stages. The initial 10% is expected to be wrapped up on or before August 30, 2019 and further 10% upon earlier of new NZ regulations coming into force and Pure Cann’s Board approving construction of the commercial cultivation facility. CAN is having an option to increase its position to 30%. There are expectations that this investment would be allowing two companies to work together in order to capitalise on increasing domestic demand with respect to medicinal cannabis in NZ as well as to explore the export opportunities as Pure Cann develops its own proposed cultivation and production facilities.

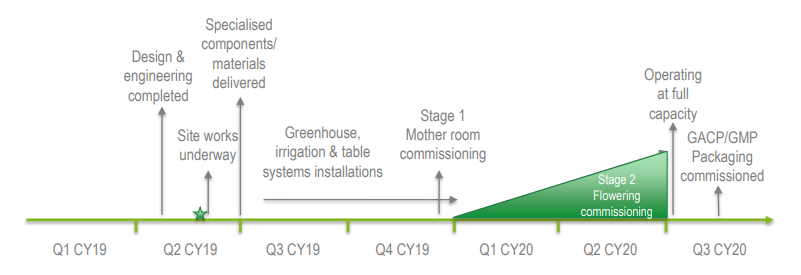

Offtake Agreement and Revised Expansion Plans Might Support Growth Prospects: CAN entered Heads of Agreement (HOA) to purchase a site situated within Mildura Rural City Council, in North West Victoria. The new greenhouse facility is anticipated to have a production capacity of up to 50,000 kilograms of dry flower per annum which will generate revenues of approximately $160-200 million at the current wholesale price of cannabis dry flower. It is expected that the site would be fully commissioned in 3Q of the calendar year 2020 with an estimated construction cost of around $130 million. The financing of this project involves a mix of debt and existing cash reserves.

Mildura facility provides a clear pathway to sustained profitability (Source: Company Reports)

The offtake agreement has been entered with Aurora Cannabis. As a result, CAN would be supplying GMP processed dry flower, extracted resin and manufactured medicinal cannabis products to Aurora until 2024, covering CAN’s full production capacity beyond that produced for the domestic needs. There are expectations that the agreement would underpin investment risk and the value which is to be generated from CAN’s large-scale cultivation expansion program. Also, it might help Aurora in its plans to meet the growing global demand for GMP grade medicinal cannabis products.

CAN Entered Contract with Victorian DHHS: Cann Group Limited had entered a contract with Victorian DHHS with regards to the supply of cannabis plant extract (resin) for the utilisation in Victorian Government’s compassionate access scheme for the children with severe & intractable epilepsy. The agreement has a term from April 2019 to June 30, 2020. With respect to the revenue stream for CAN, the full commercial terms are confidential.

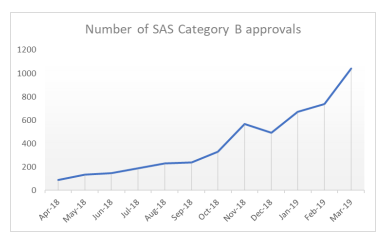

Growing global market, Australian and Export Opportunity Might Help CAN: Cann Group had stated that global legal market has been estimated at US$20 billion and over 50 countries have legalised medicinal cannabis and there are expectations that this momentum might continue. There are expectations that approximately 10 more countries might also legalise this year. The recreational use in the markets like Canada is placing pressure on the medicinal cannabis supply. There is significant Australian opportunity and the state hurdles have been removed. The Special Access Scheme is allowing patient prescription and the patient approval rates have been witnessing strong growth as there were 1,042 approvals in March 2019.

Australian Opportunity (Source: Company Reports)

Cann Group had stated that there is a potential for $1 billion per annum in the local industry and 1.2% of the population happens to use cannabis for medicinal purposes. We expect this opportunity will provide sufficient headroom to the business in years to come.. With respect to export opportunity, 342,103 registered patients coupled with the recreational use in Canada has led to the shortage thus, creating significant export opportunity. Additionally, the European markets are also opening up. The cannabis is authorised medicine in over 25 European countries. Germany has also legalised and is reimbursing the patients (almost 50,000 patients have been registered).

What Might Drive Growth for Cann Group: The Board and Management of Cann Group expects the number of key news items during the present quarter and beyond. CAN is progressing with the debt funding plans for Mildura expansion facility and the negotiations are going on with the prospective lenders. Also, the company is progressing with the preparations for the construction of the new facility, with the shipping date set for first construction materials currently being fabricated in The Netherlands. The company started the production of resin for Victoria’s Department of Health as of April 2019 and it anticipates that there would be regular orders under the agreement.

Cann Group is also focusing on building the strong platform which would help in generating sustainable profits as well as shareholder value over the long term. There are expectations that significant export and Australian opportunity coupled with the rapidly growing global market are expected to act as tailwinds for the company moving forward. Additionally, the company’s key partnerships complement the in-house skills & capabilities which might also help in getting the traction of market players.

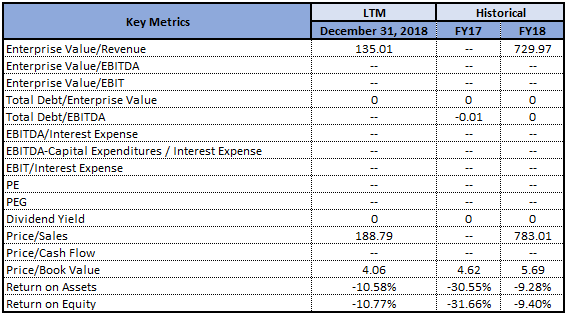

Key Metrics (Source: Thomson Reuters)

Stock Recommendation: On the YTD basis, Cann Group had delivered a return of 19%, while in the span of the previous three months, the company’s stock had posted the return of 12.80%. Currently, the stock is trading below the average of 52 week high and low prices of around $2.70.The company had stated that its existing facilities add to the critical long-term value. There are expectations that the offtake agreement with Aurora Cannabis can support its future growth plans. Fundamentally, the company is in a strong position to tap the market opportunity on the back of synergistic partnerships and agreements with key players, government support to the cannabis sector, and improving financials. Further, the company stated that Mildura facility is providing a pathway to the sustained profitability and it is expected to produce up to 50,000 kg per annum at the full capacity which would help in generating the revenues amounting to around $160-200 million at a current wholesale price of cannabis dry flower. Also, the company is expected to be aided by a manufacturing partnership which has been entered with IDT Australia and a supply agreement with Victorian DHHS. Given the backdrop of aforesaid parameters, we expect the stock price to witness an upside based on an improved EPS in the next 12-24 months. Hence, we give a “Speculative Buy” recommendation on the stock at the current market price of A$2.420 per share (up 1.681% on 30 April 2019), considering current trading level.

.png)

CAN Daily Chart (Source: Thomson Reuters)

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...