I. Sector Landscape and Outlook

At global level, fintech sector has revolutionised the online payment industry by allowing users to access money just by swiping on their cell phones/ other such devices. The technological innovation, demand for digital adoption and the need for easier financial access have been the pillars behind the rapid development of the sector. This sector has made easy, safe, and timely availability of credit compared to the traditional payment mechanisms. The revolutionary change with regards to consumer acceptance and demand scenario has allowed many fintech players to develop ground-breaking technology and tools, giving fierce competition to established banks and traditional financial providers.

Several Buy Now Pay Later (BNPL) companies have emerged in the last few years, which offer small, unsecured interest-free credit to help customers make their purchases. These companies are gaining worldwide acceptance and have made lives of consumers hassle-free as they become ubiquitous by the day.

Consumer Behaviour Amid COVID-19

COVID-19 pandemic has resulted in a shift in consumer behaviour that might change the dynamics of the consumption pattern that we have been used to for all these years. Consumers are actively climbing the digital ladder and making it an essential part of their daily schedule. With the comfort of online delivery of all essential and non-essential commodities, consumers are indulging in buying more and more online.

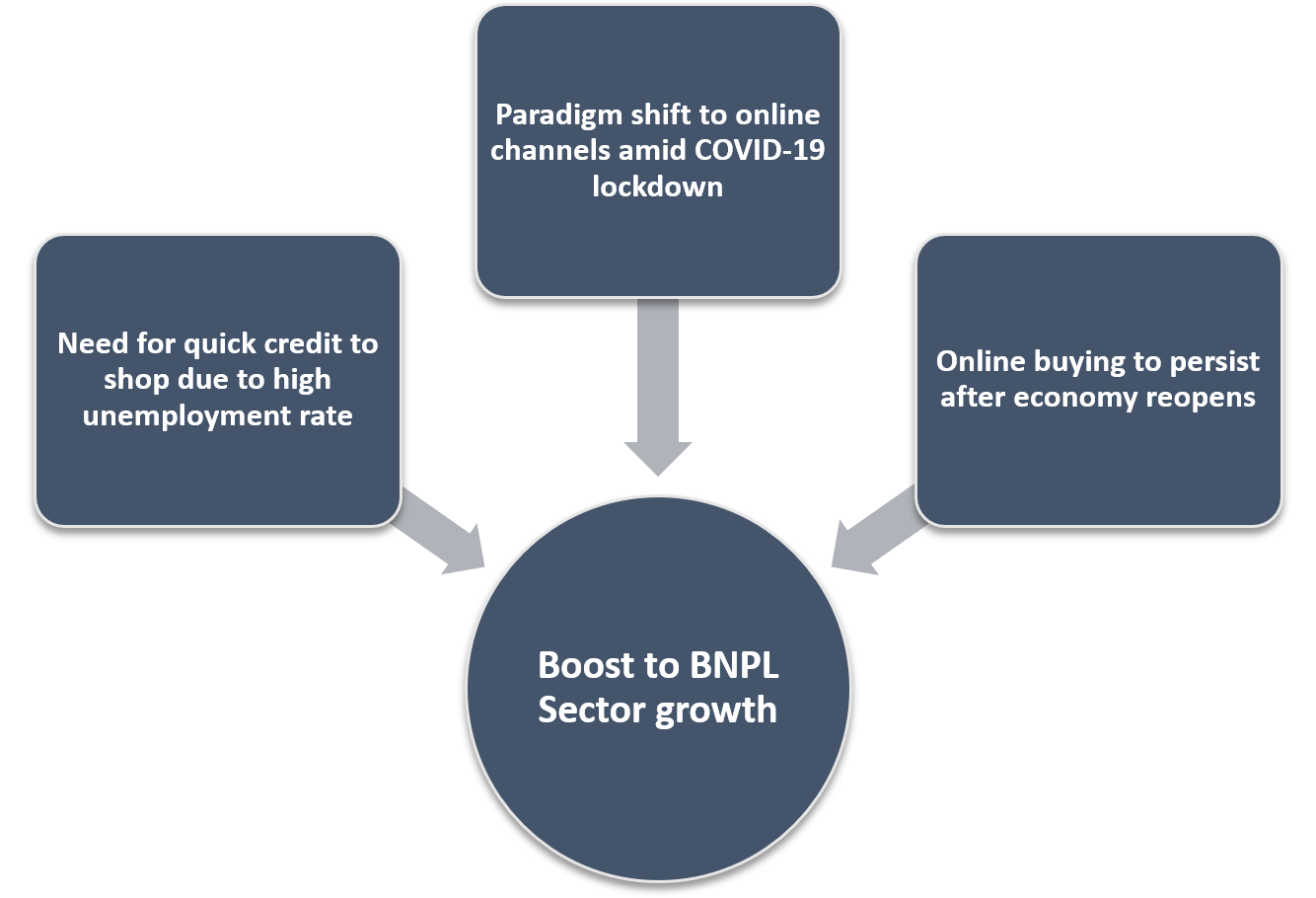

As people are doing away with paper money, coins and even plastic money, BNPL sector has gained more traction during COVID-19 when the need for being contactless has risen. BNPL industry has made it easy for consumers not even to pay before they get any goods and is rapidly evolving as a global payment choice.

Fig 1: Drivers of BNPL Sector

Source: Kalkine’s Secondary Research

BNPL platforms offer consumers a specified period (a week or a month) to make incremental payments. Paying through BNPL option lets them split their payment into many instalments at 0% interest.

More consumers are likely to stick to online buying even when they can return to their earlier spending behaviour and activity normalises. Further, the constant spiral in unemployment rate amid COVID-19 has pushed several Australians to go for quick credit options as they come under financial pressure giving a boost to the BNPL sector.

Technological products typically bank on getting the right customer base on board for long-term success. Let us understand the customer profile of the BNPL players.

BNPL Customer Profiling

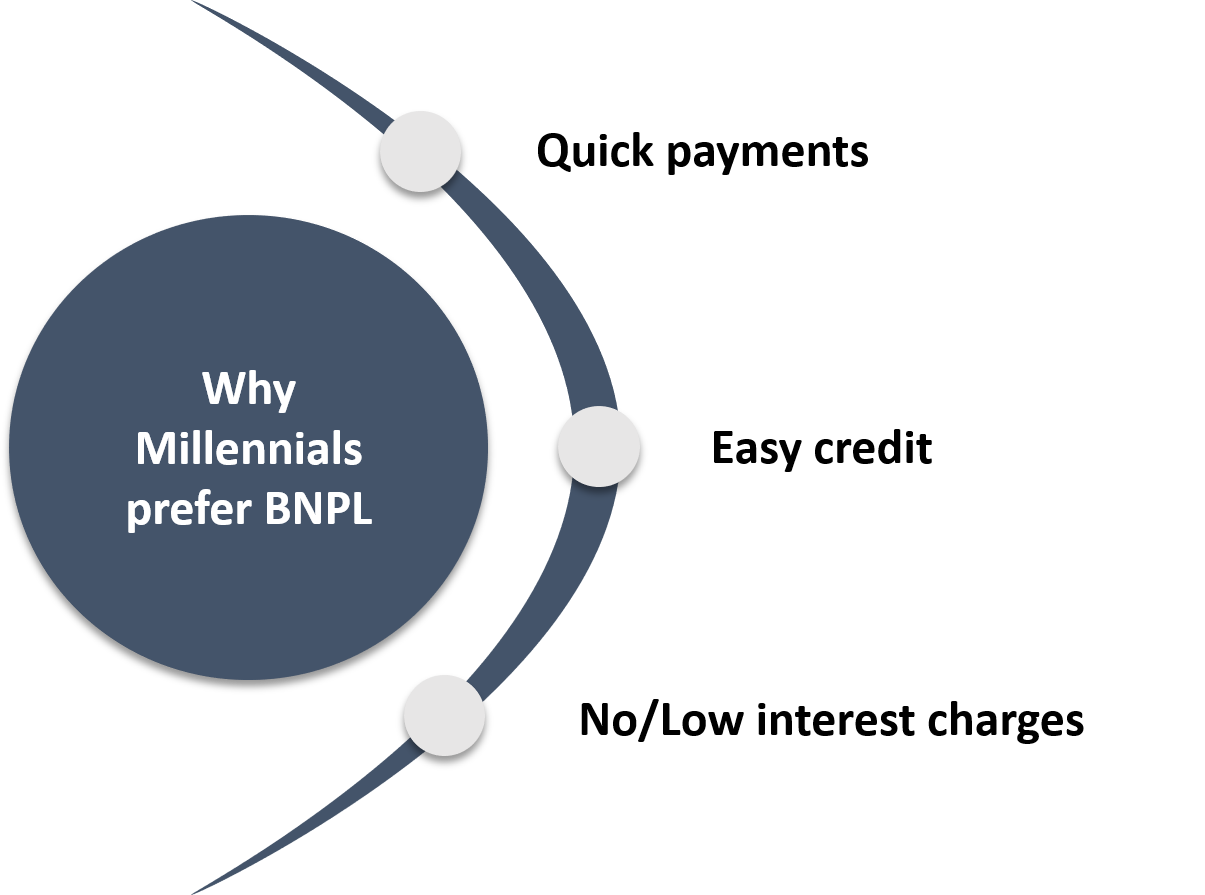

Millennials and Gen Z form the largest demographic group of BNPL sector and are doing away with traditional forms of credit. The global median age of active customers is 33 years as of 1 April 2020. BNPL is becoming popular among people who want to strike a balance between handling budget and the necessity to buy products vital to their daily lives. BNPL is particularly preferable among millennials because they typically provide advantages such as no or low interest charges, delayed payment option and easy budgeting.

Fig 2: Why Millennials Prefer BNPL

Source: Kalkine’s Secondary Research

Other customers of BNPL are merchants. Merchants have been increasingly offering BNPL options as consumers are going for late payments due to financial stress amid COVID-19. Merchants that support only credit or debit payments are at an increased risk of losing customers to relatively new players that offers more convenient payment solutions like BNPL. Some principal Merchants in Australia who went live or contracted with BNPL services during Q3FY20 include eBay, Samsung, Lancome AU, YSL Beauty, Kiehius, Kookai, Georgio Armani Beauty, Horseland Online, Pet Food Australia, Salt & Pepper.

Let us now flick through the various modes of payment that consumers indulge in and their trends.

Payments Through Various Mechanisms- BNPL Gaining Traction

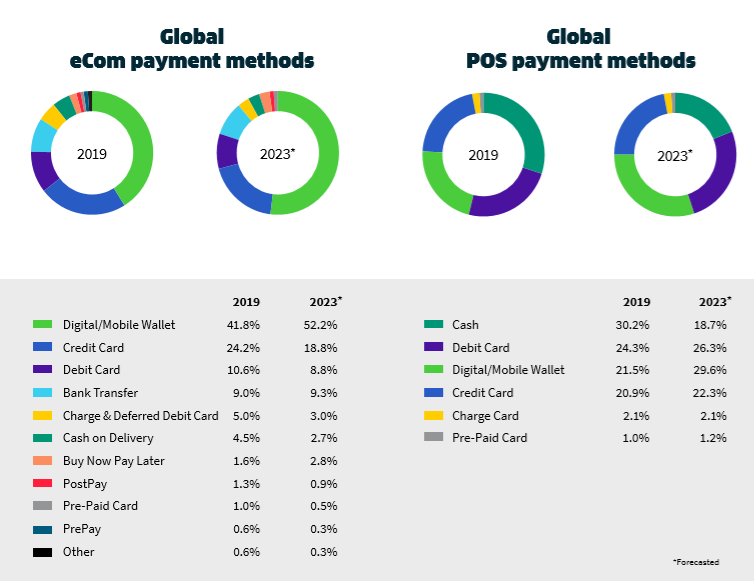

Referring to the Worldpay report 2019, it has been stated that cash remains the most preferred method of payments followed by debit card and digital wallets in 2019, amongst global point-of-sale methods. However, amongst global e-com payment options, digital wallet payments topped at 42% followed by credit card (24.2%) and debit card (10.6%) payment methods. By 2023, expert analysis (as per the report) suggests that credit card and debit card usage might drop to 18.8% and 8.8% respectively by 2023; and Digital wallets, bank transfer and BNPL payment options will be the preferred e-com payment methods by 2023.

Fig 3: Global Payment Methods

Source: WorldPay Report, January 2020

According to RBA data on credit and charge cards, the number of credit and charge card accounts have fallen by 8.4% while the number of credit cards issued dropped by 7.4% year-on-year during March 2020 compared to March 2019. The total number of credit and charge card accounts in Australia stood at 14.4 million in March 2020.

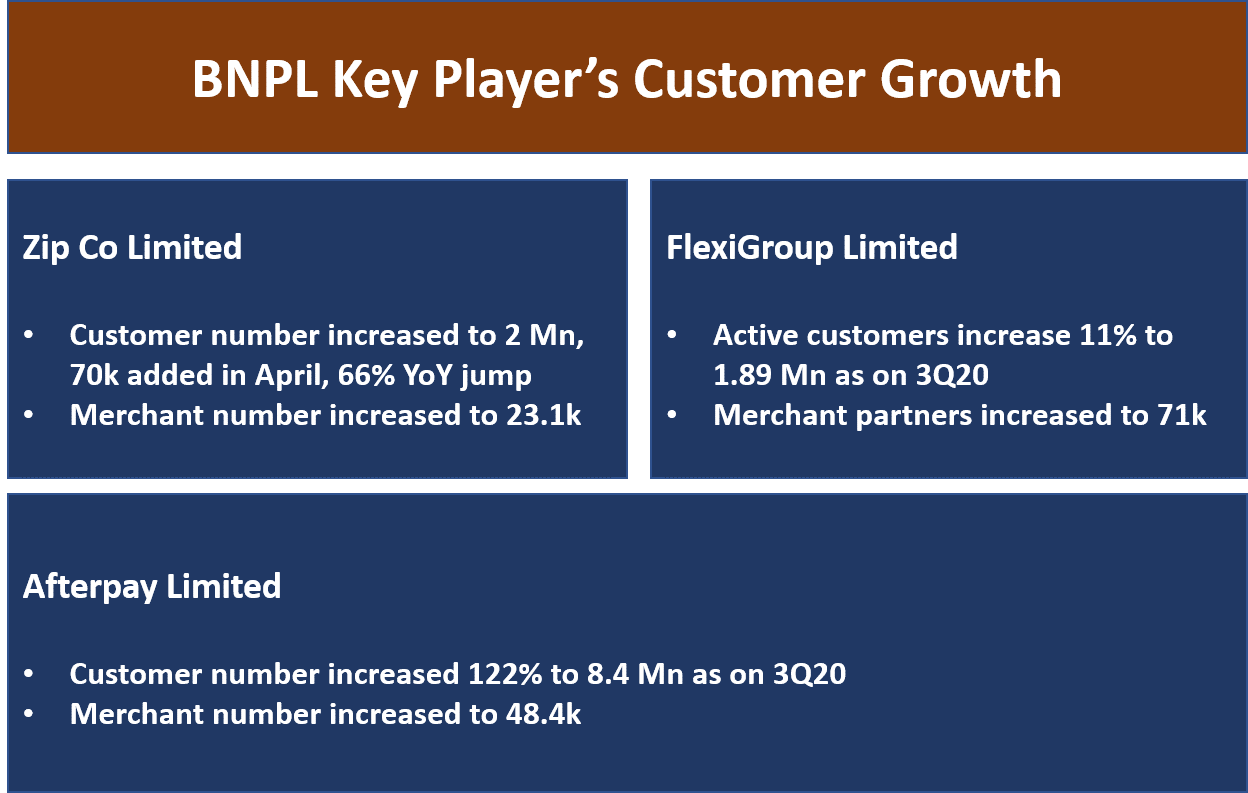

People are restricting their credit card usage and switching to the debit/prepaid transactions more during coronavirus due to job losses and pay cuts. Many BNPL players like ZIP, Afterpay and Sezzle have been reporting a rise in their customer base.

In view of the changing reliance in fintech space, Australia is emerging to be one of the leaders in the e-commerce industry, as noted over the last few years.

Fig: 4 Australian BNPL Players Attracting New Customers

Source: Company Reports

Any sector that undergoes rapid growth draws the attention of regulators and BNPL is no different. Let us look at the developments on the regulatory front.

Sector to Operate Under New Rules

The Australian Securities and Investment Commission (ASIC) is reviewing the rapid growth of BNPL sector to see if any intervention is needed. The ASIC accused the industry alleging that 1 in 6 providers bothers to check credit history and income of the consumers before offering them credit. ASIC has informed that about 44% of people who use BNPL services earn lower than $40,000 annually while about 40% of users are students or are the chunk of the part-time workforce.

Subsequently, major BNPL players like Afterpay, Zip Co, Latitude, Flexigroup etc. will follow a draft code of practice, written by Australian Financial Industry Association (AFIA) that covers measures to protect financially vulnerable from falling into debt and repulse any hard procedures from the regulator.

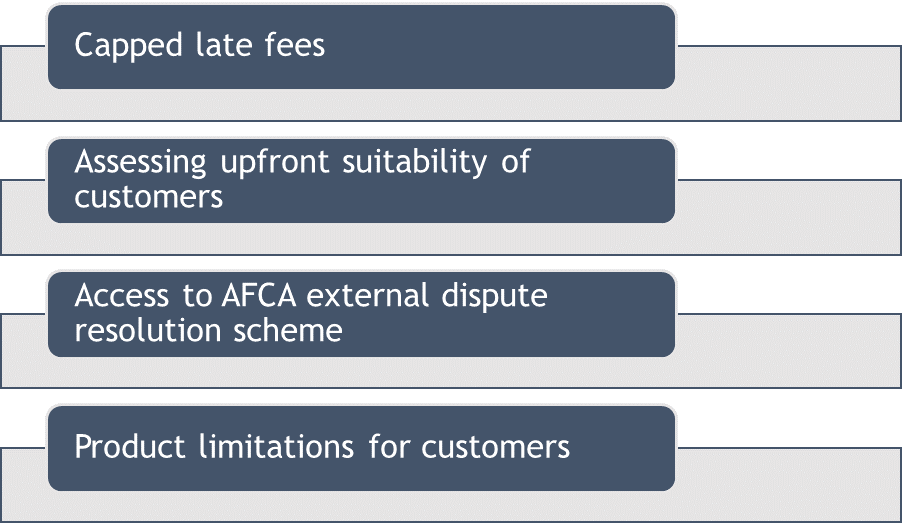

Fig 5: Pointers in the code that is expected to be introduced on 1 July

Source: ASIC

COVID-19 has turned out to be a big disaster for many businesses and consumers alike. How has this impacted consumer spending? Let us study the consumption trend amid the virus scare.

Australian Consumption Trends Under COVID-19

Coronavirus crisis has resulted in significant changes in the shopping and buying patterns of people. There has been a dramatic drop in footfall in supermarkets, shopping centres, cafes, hotels etc. as people practice social distancing to reduce the spread of the virus.

There has been an accelerated growth in online grocery shopping as people stocked up on food items and staples. The excessive urge for flexible, exclusive and accessible buying has been forcing retailers to come up with products that satisfy the same. However, many e-commerce platforms are crashing servers due to their inability to meet the current demand.

The retail sector witnessed the sharpest rise in food retailing. As per ABS, retail spending for March 2020 lifted to 8.5% due to unprecedented demand for food, household goods and other retailing. However, sales fell in cafes, restaurants, clothes and other discretionary spending.

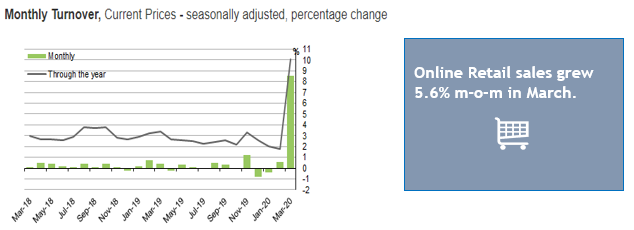

As per NAB, Online Retail Sales Index showed growth of 5.6% month-on-month while 21.8% year-on-year in March 2020. Albeit retail as a percentage of total sales for BNPL has remained lower, but it does open avenue to tap into going forward.

Fig 6: Monthly Turnover (Online Retail Sales)

Source: ABS, NAB Online Retail Sales Index

Source: ABS, NAB Online Retail Sales IndexSpending anticipated to pick up: Prime Minister Scott Morrison drafted a 3-step plan last week to re-open the Australian economy which has started from 11 May and will be implemented as per the discretion of state and territory. This will act as a welcome step for Australians to begin spending and businesses to get back up.

The Australian Government has undertaken $320 billion worth of stimulus measures translating to about 16.4% of the annual GDP. Furthermore, the Government has taken various fiscal actions to help businesses, households and workers including $130 billion JobKeeper payment to help Australian workers financially amid coronavirus crisis. Recently, it announced fortnightly $550 coronavirus supplement welfare payment as additional income support is anticipated to boost spending in months ahead. As restrictions lift, Australians are expected to limit their spending to buying food items, office supplies, alcohol and furniture. However, expenditure on taxis, gyms, cafes and entertainment is still likely to remain low for some time.

As per the latest credit and debit card spending analysis from Commonwealth Bank, spending momentum has picked up in grocery and supermarket, alcohol and household furnishings during the last two weeks ending 1 May 2020. However, total spending (credit and debit card) was down 10% compared to the previous year. There has been a sharp rise in online retail sales, showing positive movement before restrictions ease.

II. Investment Theme and Stocks under Discussion (Z1P, FXL, TYR and APT)

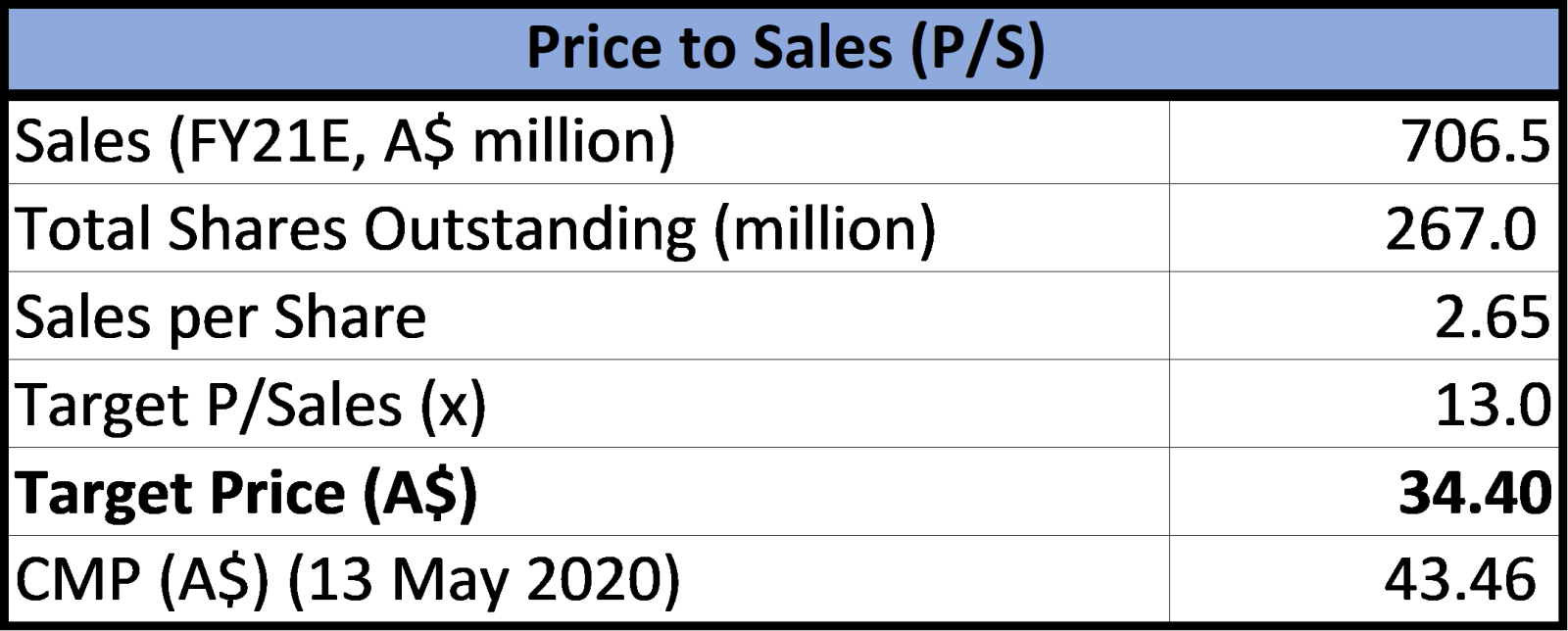

With Australia successfully taming the COVID-19 spread, many states have started to ease lockdown restrictions. Further, Prime Minister Scott Morrison unveiled a three-step plan that would be implemented by July 2020 to reboot the economy. The situation is beginning to look better for the economy at large and BNPL sector in particular. Let us deep dive into four BNPL related players and understand how to position them in one’s portfolio. To assess the potential, stocks have been valued using ‘Price/Sales’ methodology.

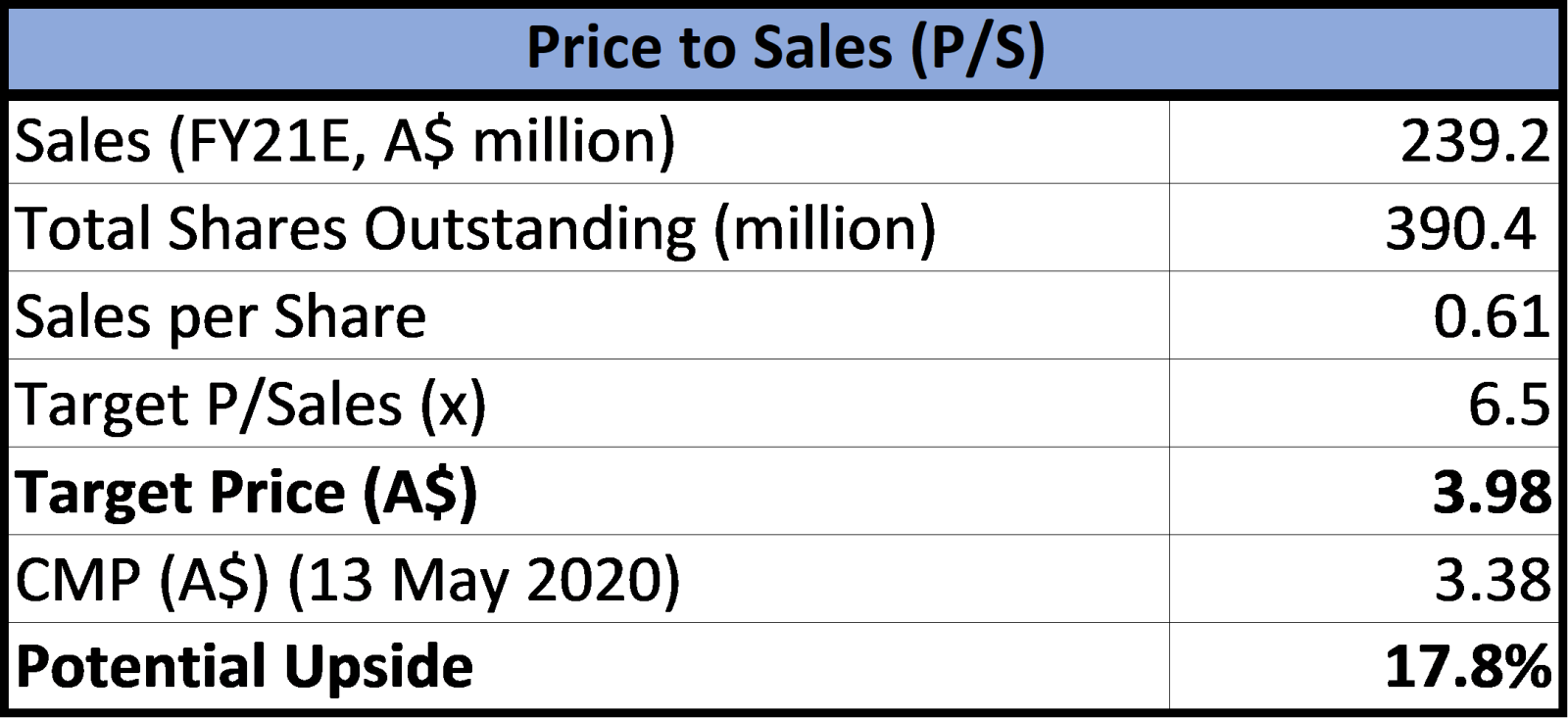

1. ASX: Z1P (ZIP CO LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap – A$ 1.34 Billion)

Zip Co Limited is one of the leading players in the payment industry and digital retail finance. It is involved in offering point-of-sale credit and digital payment services to consumers and merchants. The group offers an interest free buy now pay later solution to its customers with flexible repayments schedule.

Valuation

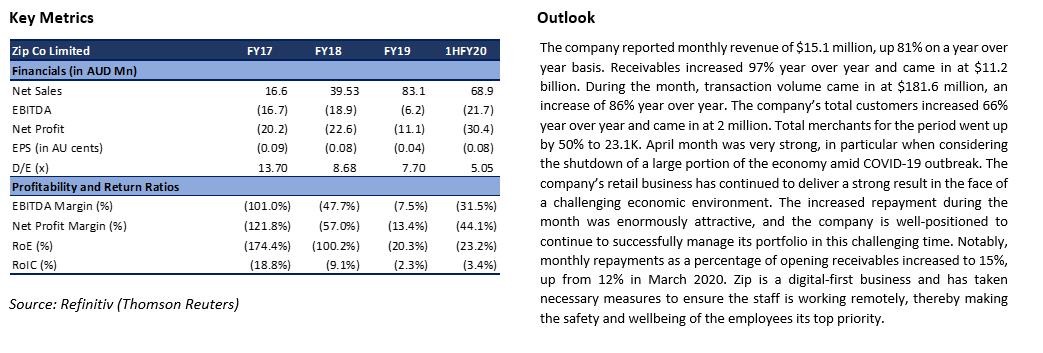

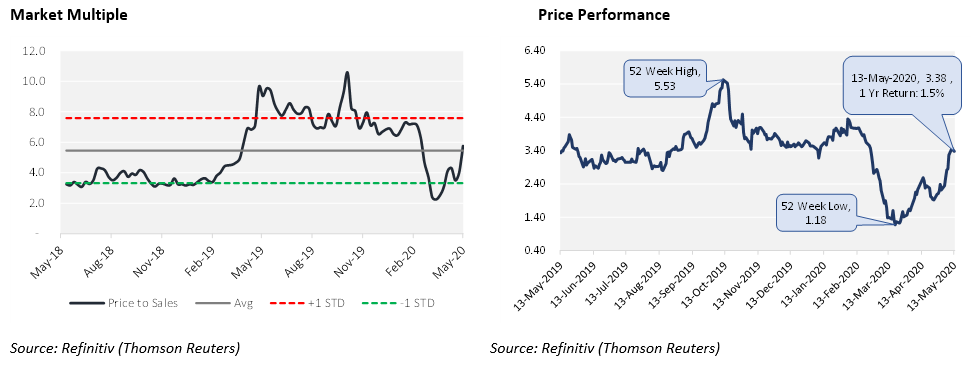

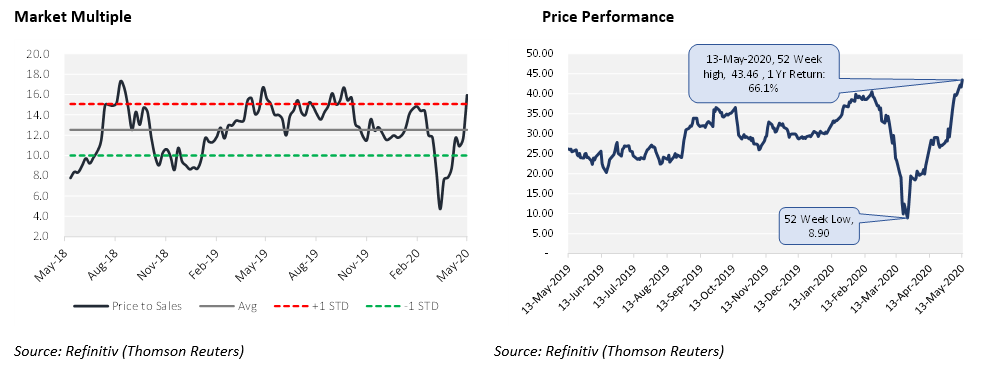

The company has not witnessed any material impact from COVID-19 across its business and continues to perform strongly, with healthy customer growth, transaction volume and a strong pipeline of enterprise partners. Going forward, the company expects robust demand for online purchases, bill payments, everyday spend and health and expects to increase its penetration in the same space. Despite recent market volatility, the company opines that in the coming years it will see the rapid adoption of alternative payments, including BNPL. The company is targeting 2.5 million customers by the end of FY20. The stock has corrected ~4.5% YTD and significantly outperformed the benchmark by ~17.8% during the same time. We have considered Credit Corp Group Ltd, Xero Ltd, Afterpay Ltd etc. as a peer group for comparison purpose. Our illustrative valuation model suggests that the stock has a potential upside of ~18% on 13 May 2020 closing price.

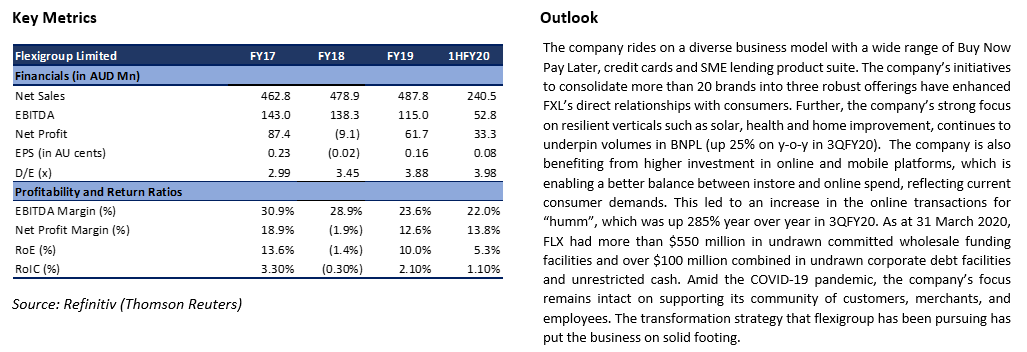

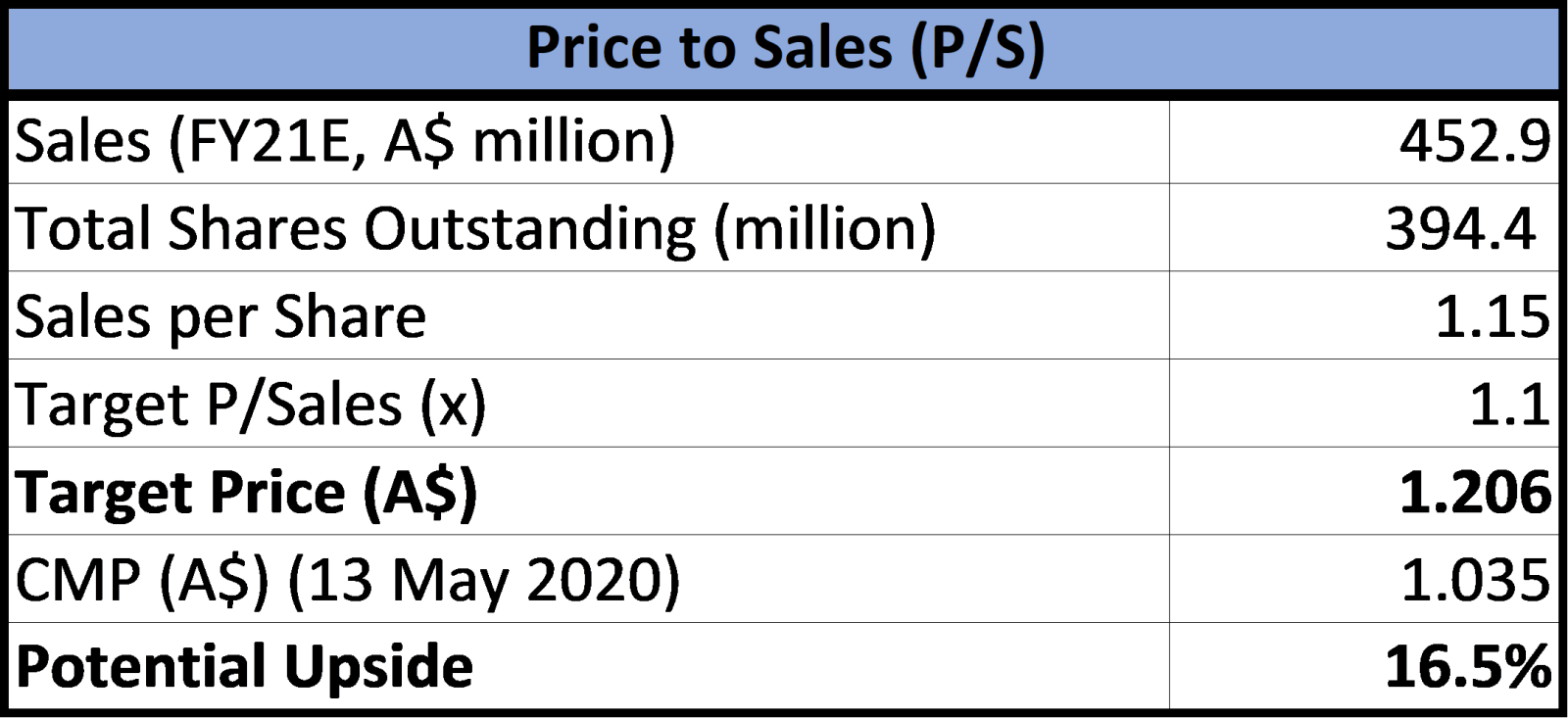

2. ASX: FXL (FLEXIGROUP LIMITED)

(Recommendation: Speculative Buy, Potential Upside: Low Double Digit, Mcap – A$ 416.8 Million)

Flexigroup Limited is a diversified financial services group which offers no interest ever payment products, leasing, vendor finance programs, interest-free finance, credit cards and other finance solutions to consumers and businesses. The group relaunched its buy now pay later offerings in April 2019 by consolidating two legacy products into one new brand ‘humm’.

Valuation

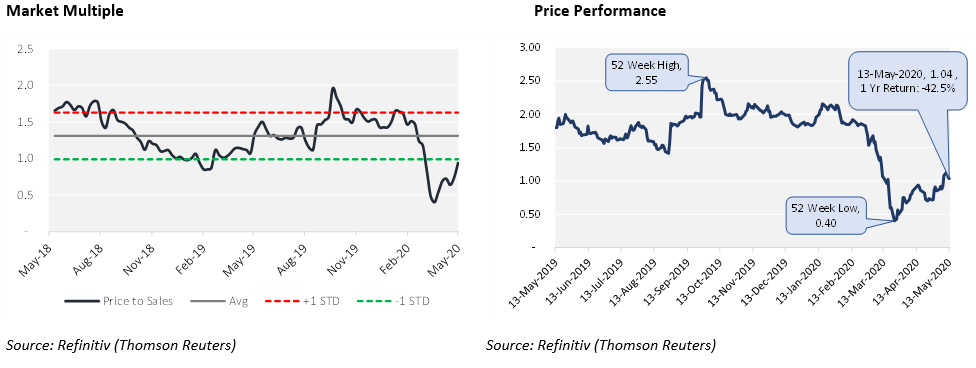

The company is taking initiatives to curb the cost in the context of the current economic environment and targets to reduce FY21 annualised operating expenses by more than 15%. Consequently, the company is likely to surpass its aim of $7 million in cost savings in FY20. In addition to the above cost initiative, Flexigroup has also undertaken several near-term actions including the suspension of marketing activity; renegotiations with suppliers; and the reduction of Board and Executive pay for three months. For FY20, the group expects its transaction volume to increase in the range of 10% to 15%, on the heels of new product launches. Going forward, FXL also predicts to balance margin with growth along with double-digit return on equity. The stock has corrected ~42% YTD but seen a strong pull back and rose ~22% in last one month and outperformed the benchmark index by ~200% in last one month. We believe the price correction provides a decent entry point. We have considered Eclipx Group, Money3Corp Ltd and Collection House Limited etc., as a peer group for comparison purpose. Our illustrative valuation model suggests that the stock has a potential upside of ~17% on 13 May 2020 closing price.

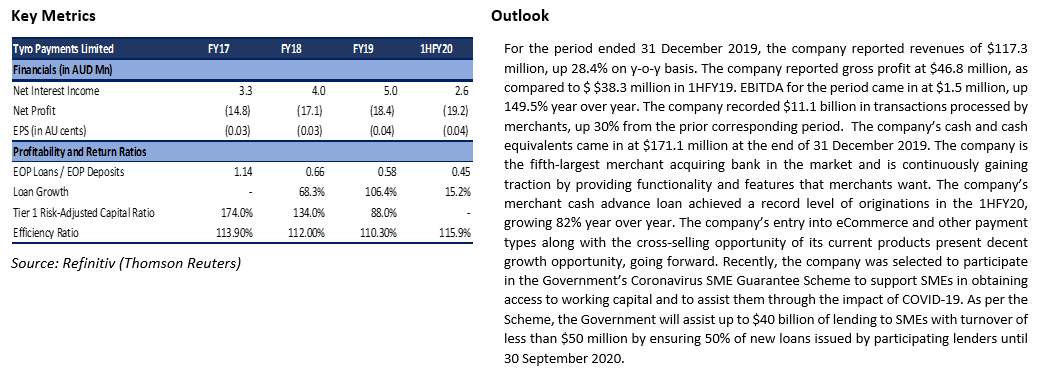

3. ASX: TYR (TYRO PAYMENTS LIMITED)

(Recommendation: Buy, Potential Upside: Low Double Digit, Mcap – A$ 1.73 Billion)

Tyro Payments Limited is betrothed in providing credit, debit and EFTPOS card acquiring, private health fund claiming services to Australian companies. Although the group is not extensively into buy now pay later space, it had tied up well with BNPL businesses such as Afterpay and ZIP in the past.

Valuation

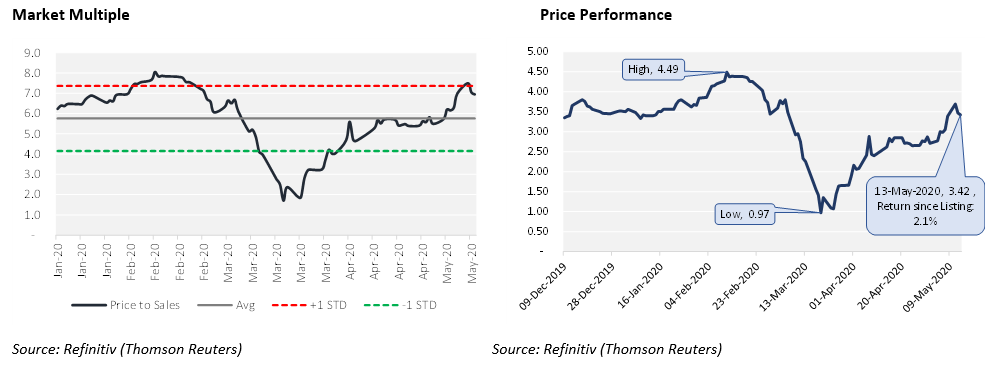

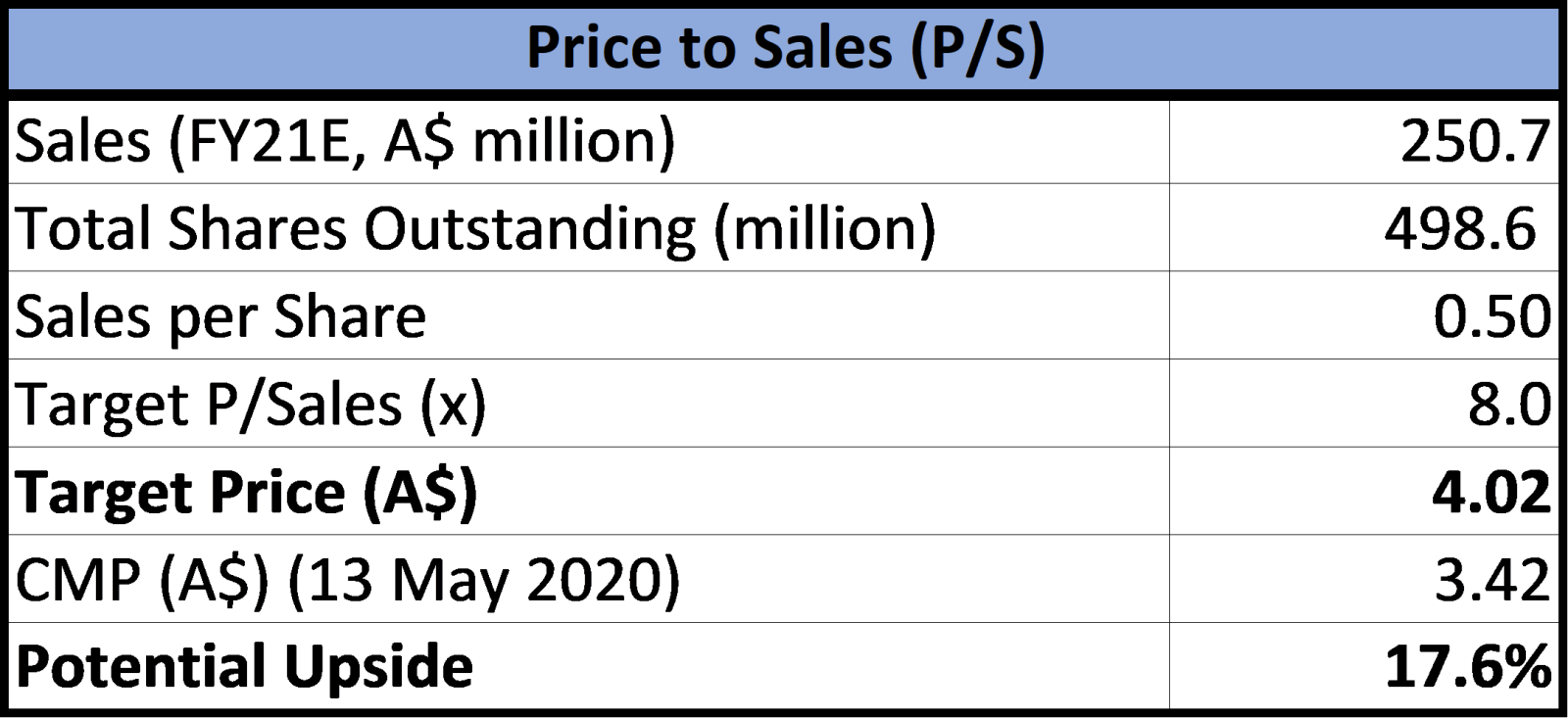

TYR announced that its transaction value in April FY20 (year-to-date basis) soared 20% year over and came in at $17.190 billion. Notably, in 1HFY20, the company managed a transaction value of more than $11.1 billion for more than 32,000 Australian merchants. Although the company has withdrawn its FY20 outlook, its key priorities and plans are aimed at sustained growth in its payments along with banking businesses. The stock has corrected ~2.8% YTD amid the global market free fall and outperformed the benchmark index by~20%. We have considered EML Payments Ltd, Afterpay Ltd and Pushpay Holdings Ltd etc., as a peer group for comparison purpose. Our illustrative valuation model suggests that the stock has a potential upside of ~18% on 13 May 2020 closing price.

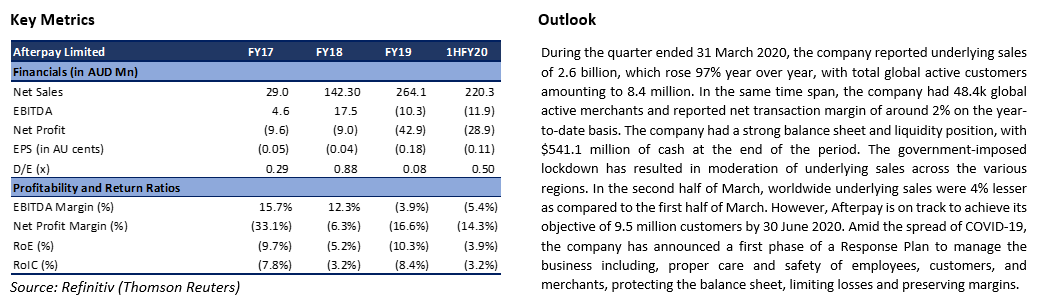

4. ASX: APT (AFTERPAY LIMITED)

(Recommendation: Expensive, Potential Downside Expected, Mcap – A$ 11.13 Billion)

Afterpay Limited is betrothed in offering technology-based payments solutions for businesses & consumers via its Afterpay and Pay Now services. The group offers instalment payment services that enables consumers to buy product on a ‘buy now, receive now and pay later’ basis.

Valuation

The unprecedented circumstances from the breakout of COVID-19 are causing significant concerns in financial markets, and APT has not been immune to these market concerns. However, it is managing its losses in real-time by identifying leading indicators early. The stock of APT gave a return of 43.58% in the past six months and a return of 48.49% in the last one month. The company is set to fight the current challenges with a strong capital position and an excellent business model that will help it survive and thrive in the long run. We have considered Xero Ltd, Perpetual Ltd and Challenge Ltd etc., as a peer group for comparison purpose. Our illustrative valuation model suggests that the stock has a potential downside. Considering the uncertain environment while the stock has witnessed a significant run-up in view of the high returns in the past six months, we believe that the stock is ‘Expensive’ at the current price.

Note: All the recommendations and the calculations are based on the closing price of 13 May 2020. The financial information has been retrieved from the respective company’s website and Refinitiv (Thomson Reuters). All the recommendations are valid on 14 May 2020 price as well.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people. Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376). The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product. The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd do not hold positions in any of the stocks covered on the website. These stocks can change any time and readers of the reports should not consider these stocks as personalised advice.

Past performance is not a reliable indicator of future performance.

AU

AU

Please wait processing your request...

Please wait processing your request...