Company Overview - Buru Energy Limited (Buru) is engaged in oil and gas exploration and production in the Canning Superbasin, in the northwest of Western Australia. The Company’s Yulleroo 3 well is located in Exploration Permit EP 391 some 80 kilometers to the east of Broome. The Asgard 1 well is located in Exploration Permit EP 371 some 180 kilometers to the southeast of Derby, and 30 kilometers northeast of Noonkanbah Station. The Ungani North 1 well is located in Exploration Permit EP 391 some 100 kilometers to the east of Broome, and lies some six kilometers north of the Ungani Production Facility. The Yulleroo 4 well is located in Exploration Permit EP 436.The Company’s subsidiaries include Terratek Drilling Tools Pty Limited, Royalty Holding Company Pty Limited, Buru Energy (Acacia) Pty Limited, Buru Operations Pty Limited and Yakka Munga Pastoral Company Pty Limited.

Analysis - In this report, we bring our focus back to Buru Energy (BRU) in view of the latest updates released by the Company. As per BRU’s quarterly report ending 30 September 2014, the year-to-date production was 230,256 bbls of oil. Further, six shipments totaling 215,163 bbls were sold resulting in the Joint Venture year to date sales revenue of $21.8 million. BRU’s key partners include Mitsubishi and Apache, which add to the Company’s benefit.

For capital raising, a share placement and share purchase plan at an issue price of $0.75 raised $31.1M before costs. The Company is now fully funded through the end of 2015 and about to start an exciting exploration and appraisal program.

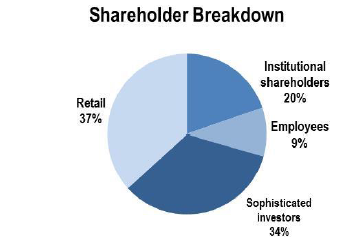

Shareholder Breakdown (Source – Company Reports)

Shareholder Breakdown (Source – Company Reports)

The cash flow statement for the quarter ended 30 September 2014 entails exploration expenditure of $3.9M, Ungani development expenditure of $1.3M, and Ungani production operating expenditure of $2.2M, for the quarter. The net cash inflow of $24.3M has been reported for the quarter with net cash reserves of $61.9M at the end of the quarter.

The Company’s shares on issue are 298 million and market cap is $253 million. Further, cash on hand is about $37.6 million as at 30 June 2014. Net Acreage is about 53,188 sq km, i.e., ~13.2 million acres. BRU’s regional acreage position entails continuous basin wide coverage gross 93,007 sq kms (22.9 million acres) - 640km by 250km (~450 miles by ~150 miles). BRU’s unique portfolio which entails oil development, gas appraisal, and quality exploration coupled with multiple play types with high potential indicate a good potential.

.png) Three Major Petroleum Systems (Source – Company Reports)

Three Major Petroleum Systems (Source – Company Reports)

Key investment drivers for the Company include extensive basin wide acreage spread in the onshore Australian basin, immense oil and gas potential in conventional reservoirs with current oil production from Ungani field, multi TCF tight gas resource with high liquids content, high equities and operatorship, and State Agreement that provides long term tenure over core acreage.

The significant highlights reflected that first phase of the workover of Ungani 1ST1 was successfully completed and second phase which was earlier underway has also been completed on 31 October 2014. The production tests have been quite encouraging and the water cut has decreased from ~30% to ~2%. With regards to BRU’s appraisal and exploration program, acquisition of 988kms of 2D seismic was completed, and acquisition of Jackaroo 3D seismic has commenced and is progressing well (35% complete as per November 2014 updates). The seismic data is aimed at maturing oil drilling targets for 2015 and to meet permit commitments. The exploration drilling program and Phase 1 TGS activity is to be commenced in the upcoming quarter.

First Gas from Yulleroo 2 (Source – Company Reports)

First Gas from Yulleroo 2 (Source – Company Reports)

With regards to the conventional gas and oil segment, the Company specified about good potential for conventional gas resources including the Yulleroo. This is further associated with low cost development with short term cash flow generation.

The Company has been able to identify an enormous potential in Laurel formation with regards to tight gas. Test stimulation (frac) program has been planned for early 2015. BRU asserts that this will provide a long term value for all stakeholders. The Company has been successful in attaining state agreement with a long term tenure (25 years). With regards to the three major petroleum systems, Ungani oil trend has demonstrated high quality conventional reservoirs with prolific oil source rocks and well defined prospects; Laurel Formation showcased potential giant gas accumulation with basin centred tight wet gas accumulation and conventional reservoirs presenting potential high deliverability; and Goldwyer/Acacia demonstrated large scale conventional oil potential in the Acacia Sandstone and Nita Formation with Apache providing low cost evaluation.

For Ungani discovery, substantial oil column (+50m) in very high quality conventional dolomite reservoir has been confirmed by two wells. The production testing shows excellent reservoir performance indicated by strong production of total 320,785 bbls to end August. Next steps in development plan entail commercialization wherein EPT has confirmed resource base to support incremental development plan. The simple and relatively cheap production system is another point in development.

.png) Ship loading at Wyndham (Source – Company Reports)

Ship loading at Wyndham (Source – Company Reports)

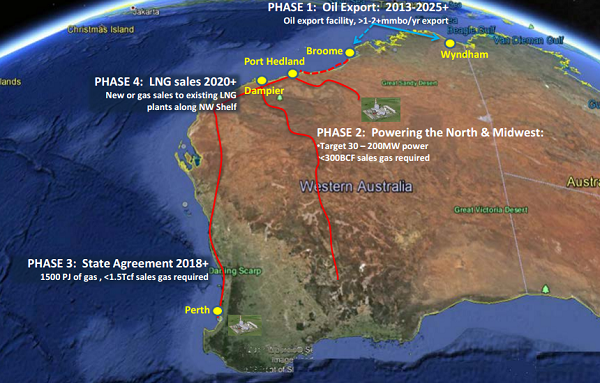

A detailed review of the Ungani EPT reveals that U2 well is producing very strongly with the rate constrained as planned to up to 1,000 bopd aligned with current trucking capacity. U1ST1 workover first stage has been successful. The second phase included placement of a cement plug to allow production of dry oil. U3 workover has been planned for production test/injectivity potential. UN Production test has also been planned. The Company has also upgraded its production facilities to better operability. With regards to the oil trucking, the Company reported for 900km to existing tank farm at Wyndham Local contractor with excellent reliability. Trucking system has also been sized to port storage and ship capacity. With regards to the Port Facility, Wyndham Port is led to use the existing Cambridge Gulf Limited facility. BRU has completed the required modifications to the tank farm. The Company believes to have potential to increase storage to streamline ship schedules. Lastly, crude shipping is being set from Wyndham to regional refineries. Shipping and sales is by Petro Diamond Company Limited (Mitsubishi subsidiary in Singapore).

BRU further aims to optimizing shipping export route and minimizing wet weather downtime. The Company also stated the need of additional wells with produced water handling system.

The Company is renegotiating the Mitsubishi facility post Ungani 3 results and analysis. Even, NAB facility structure is also being reviewed prior to reserves certification process. Moreover, negotiations for production agreements with Native Title Parties are continuing. BRU is in negotiations for access to the Port of Broome for export of oil. Even negotiations with Nyikina Mangala and Yawuru for the production license agreement for Ungani are progressing along with negotiations with Yawuru for the 2015 TGS. Under the TGS program, Phase 1 activity has commenced with on-track progress. Works at Asgard and Valhalla North sites are also completed.

Buru Energy Vision (Source - Company Reports)

Buru Energy Vision (Source - Company Reports)

BRU with consensus from Apache also entered into fixed price drilling contract with DDH1 Drilling for the use of DDH1 Rig #31 (UDR5000 highly mobile mineral rig). After completion of Commodore 1, the rig will be used for drilling the second coastal well, Olympic 1. The Company is also exploring high value oil targets and other innovative high plays in regions such as Fitzroy Trough. Under Ungani program also, Senagi prospect in EP 458 which is a shallow structural target, is being explored. Drilling programs may be initiated in early second quarter of the next year, i.e., after the wet season.

.png) DDH1 Rig 31 (Source – Company Reports)

DDH1 Rig 31 (Source – Company Reports)

Recently, BRU got the tender for the Yakka Munga pastoral lease which includes the areas of the Ungani facility. With financing and lease management arrangements in place, the net impact of transaction is estimated to be of the order of about $3.5M with regards to BRU’s cash position.

The Company forecasts a net cash outflow of about $10.9M in the December 2014. This will include costs associated with exploration, development, production and adminsitration and corporate.

BURU Energy Chart (Source - Thomson Reuters)

BURU Energy Chart (Source - Thomson Reuters)

The recent changes such as restructuring of the board emphasized on operational aspects. Further, the Company has now built a strong skill set in terms having proven oil and gas finders and developers with strong technical experience; talent for world scale projects and budgets with strong focus on the bottom line; people with expertise from major corporate environments; and better stakeholder relations in view of strong Government connections and community engagements.

In view of the above positive updates and a potential play set by BRU, we put a

BUY recommendation for this stock at the current price of $0.63.

Disclaimer

The advice given by Kalkine Pty Ltd and provided on this website is general information only and it does not take into account your investment objectives, financial situation or needs. You should therefore consider whether the advice is appropriate to your investment objectives, financial situation and needs before acting upon it. You should seek advice from a financial adviser, stockbroker or other professional (including taxation and legal advice) as necessary before acting on any advice. Not all investments are appropriate for all people.Kalkine.com.au and associated pages are published by Kalkine Pty Ltd ABN 34 154 808 312 (Australian Financial Services License Number 425376).The information on this website has been prepared from a wide variety of sources, which Kalkine Pty Ltd, to the best of its knowledge and belief, considers accurate. You should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation.Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. To the extent permitted by law, Kalkine Pty Ltd excludes all liability for any loss or damage arising from the use of this website and any information published (including any indirect or consequential loss, any data loss or data corruption). If the law prohibits this exclusion, Kalkine Pty Ltd hereby limits its liability, to the extent permitted by law to the resupply of services. There may be a product disclosure statement or other offer document for the securities and financial products we write about in Kalkine Reports. You should obtain a copy of the product disclosure statement or offer document before making any decision about whether to acquire the security or product.The link to our Terms & Conditions has been provided please go through them and also have a read of the Financial Services Guide. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...