Company Profile - Buru Energy Limited (Buru) is engaged in oil and gas exploration and production in the Canning Superbasin, in the northwest of Western Australia. The Company’s Yulleroo 3 well is located in Exploration Permit EP 391 some 80 kilometers to the east of Broome. The Asgard 1 well is located in Exploration Permit EP 371 some 180 kilometers to the southeast of Derby, and 30 kilometers northeast of Noonkanbah Station. The Ungani North 1 well is located in Exploration Permit EP 391 some 100 kilometers to the east of Broome, and lies some six kilometers north of the Ungani Production Facility. The Yulleroo 4 well is located in Exploration Permit EP 436.The Company’s subsidiaries include Terratek Drilling Tools Pty Limited, Royalty Holding Company Pty Limited, Buru Energy (Acacia) Pty Limited, Buru Operations Pty Limited and Yakka Munga Pastoral Company Pty Limited.

Analysis – In light of the progress made at Ungani over recent months and the upcoming Laurel tight gas pilot program we look at BRU. With Ungani – 2 flowing at 1000 bopd and the first oil shipment due to leave the wyndham port in late January, significant progress has been made regarding the phase 1 development plan. That said results from Ungani-3 and the full data set from the 3D seismic program in coming months will provide greater confidence in the ultimate resource size setting the scene for a final investment decision on a more material 5000bopd Phase 2 development as early as 1q14.

With BRU paying as much as A$30/bbl to truck oil to the Kwinana refinery and crude prices realised at a 10% discount to Brent, BRU continues to investigate a permanent export terminal solution. Indedd success here could see transportation costs fall to US$6-12/bbl and allows it to realisemarket prices for its sweet crude blend. Furthere more BRU could elect to take advantage of Mitsubishi’s shipping and marketing expertise to crystallise what we estimate to be a 10% premium to Brent. A permanent export solution will also provide scalability in the event of further exploration success.

Following a hiatus in activity last year, BRU plans to fracture stimulate four existing wells during the 2014 dry season. With the large resource potential across the Laurel Wet Gas Project now well understood, the next phase of testing is likely to provide greater confidence in the productive potential of the pplay. In the absence of further near term operational updates the ongoing WA parliamentary enquiry into the implications of hydraulic fraccing for unconventional gas could create some negative sentiment particularly the environmental approval for this program is yet to be granted.

In light of the scale of the unconventional gas resource seen across the Laurel tight gas formation and a long dated gas commercialisation path BRU has recognised the need to generate cash flow to fund its residual shawre of near tremgas appraisal. Consequently over the last 12 months it is clear that the eUngani oil trend has received greater attention from managemenrnt. While the core 5,000bopd development could generate net operating cash flow of A$50M, gross crude production could ultimately reach 16,000bopd by 2018 based on further exploration success.

Source – Company Reports

A re-commencement of Ungani production has been well received by the market, with the share price rising more than 50% from its early December 2013 low of about A$1.30per share. We believe that either greater Ungani exploration success or further progress surrounding the Laure tight gas play will have to be delivered this year to see further performance from here.

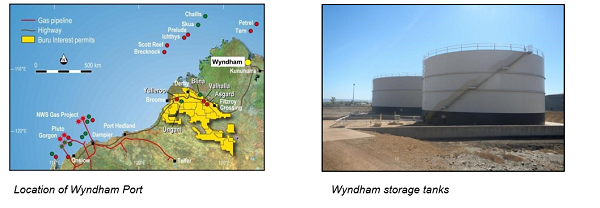

Following an agreement with traditional land owners in June , the announcement of a funding package in august, completion of the Ungani 3D seismic program in October, successful completion of work over at Ungani – 1&2 in early December and initial oil production at Ungani-2 substantial progress has already been made. Under phase-1 of the development, BRU worked over the existing Ungani – 1&2 wells which were expected to deliver production of 1000bopd in the coming months. Indeed Ungani-2 alone is already producing at this rate following work over and subsequently clean up. With Ungani – 1 clean up now commenced production could improve further. Management is already proposing to increase trucking capacity to cater for 1,500bopd of production. BRU has finalised a preliminary export location at the Wyndham Port, with the first 40kbbl lifting expected in late January. Phase 1 development costs are likely to be limited to A$20M gross with BRU’s A$10M refundable by Mitsubishi at final investment decision (FID) of full field development. Construction works have commenced for the export of Ungani oil through port of wyndham as part of Phase1 of the Ungani development. This work is being undertaken in co-operation with Cambridge Gulf Limited, the owner and operator of the Wyndham Port tank farm.

Source – Company Reports

Source – Thomson Reuters

An expected 5,000bopd production rate from Ungani clearly justifies a standalone export terminal. Based on the differences in transportation costs between Kwinana and the highest cost export option, we believe there is a saving of A$160M over the life of the development. BRU is planning to construct a flow line to connect Ungani to Great Northern Highway. The 8000bopd, 6 inch, 70km Growler to Lycium flowline and 15000 bopd, 8 inch, 74km flowline connecting Lycium to Moomba cost A$40M in total.

We understand that the current permanent export terminal locations being investigated are at Broome, Port Hedland and Dampier. All of these locations have existing petroleum handling ports and storage. Initially a temporary export facility has been located at Wyndham to support the phase-1 development; however Broome appears the logical location for an export facility given its proximity to Ungani. BRU does not expect that it will fund an export terminalon its balance sheet rateher we expect a third party owner/operator to be engaged.

Following interpretation of 2D seismic and initial results at Ungani 1&2, BRU estimates for gross recoverable resources ranged between 5 to 20mmbbls. However subsequent interpretation of pressure data from the extended production tested confirmed a minimum resource estimate of 8 mmbbls in October 2012. Data from the recently completed 3D seismic program will likely provide greater certainty regarding field closure and volumetrics.

Following the successful Ungani discovery and a regional review undertaken in FY12, BRU has identified a further 20 leads and prospects across the 1 million acre Ungani Trend. The prospects exhibit the same seismic signature. Of the dolomite limestone reservoir and shale seal and are mapped on existing 2D seismic. While the focus remains on successful commissioning of the core Ungani development, further exploration success this year could take advantage of installed infrastructure and potentially see production reach as high as 16000bopd by 2018.

BRU will have to deliver progress surrounding the gas portfolio to deliver further performance. Following two consecutive years of drilling in Canning basin, 2013 was instead spent on optimisation of the acreage position, securing the WA state agreement and finalising funding. None the less activity is expected to accelerate this year, with BRU planning to fracture stimulate four wells over the April to November dry season at a budgeted cost of A$54Million gross. With 47tcf of prospective gas resource independently estimated across the Laurel Wet Gas Project, the large resource potential appears well understood. However the next phase of testing is likely to provide greater confidence in the productive potential of the Laurel tight gas play.

Last August BRU announced A$110 – 130Million of new funding to support the ongoing development t of Ungani Oil field, further conventional oil exploration across the Ungani trend and the next phase of testing regarding the Laurel Wet Gas Project. Consequently we continue to see BRU fully funded for the 2014 program with A60 Million of surplus funding, supported by a ramp up in Ungani production. We will be putting a buy on the stock at the current price.

Disclaimer

Kalkine provides general advice on securities. Kalkine does not provide advice that takes into account your, or anybody else’s investment objectives, financial situation or needs. We strongly suggest that you should make your own enquiries about any investments and we strongly suggest you seek advice before acting upon any recommendation. Kalkine Pty Ltd has made every effort to ensure the reliability of information contained in its newsletters and websites. All information represents our views at the date of publication and may change without notice. Employees and/or associates of Kalkine Pty Ltd may hold one or more of the stocks reviewed on this website. On the date of publishing this report (mentioned on the website), employees and/or associates of Kalkine Pty Ltd currently hold positions in: BHP, BKY, KCN, PDN, and RIO. These stocks can change any time and readers of the reports should not consider these stocks as advice or recommendations.

Copyright

Copyright © 2014 Kalkine Pty Ltd ABN 34 154 808 312. No part of this website, or its content, may be reproduced in any form without the prior consent of Kalkine Pty Ltd.

Kalkine is a trading name of Kalkine Pty Ltd ABN 34 154 808 312, which holds Australian Financial Services Licence No. 425376.

Past performance is not a reliable indicator of future performance.

Please wait processing your request...

Please wait processing your request...